Executive Summary

This empirical study on business rescue would provide insight on how the Companies Act no.71 of 2008 would contribute the leading South African companies to overcome the recessional impact. The paper has organised the case study of ARM, a leading South African company, which seriously evidenced the recessional impact in 2009 caused from the global financial crisis of 2008. The paper has prearranged with six major chapters that integrated problem statement on the topic area, conducted the research with both primary and secondary data, integrated theoretical framework with finding and discussion to come into conclusion. This study has identified that the business rescue under Companies Act no.71 of 2008 of South Africa is an advanced and landscape legislation, which is a powerful tool to mitigate recessional impact of 2009. This milestone legislation is more advanced contributor than the US and the UK bankruptcy code, and the US and the UK policymakers have too many scope to learn from this Act. The outcome of this dissertation would contribute to gain further momentum as well as awareness from the academicians, companies, and financial institutions to handle with business rescue.

Problem Statement

Introduction

This dissertation would examine the Business Rescue concept of Companies Act No.71 of 2008 with the aim to explore and investigate how this legislation possibly will contribute the South African Companies to overcome the impact of recessional economy of 2009 and it would also investigate the position of African Rainbow Minerals Limited as a case study in this regards. This study would be organised in six major chapters those have demonstrated as below-

Problem Statement

The Problem Statement or introduction is the foremost opening chapter of this dissertation, which would deliberate with the overview of entire study with the background and rationale of the research. In addition, this part will raise research questions to support the topic area, enlighten the scopes and drawbacks of the research along with research objectives.

Literature Review

The Literature Review is the second chapter that would deliberate with the appropriate theoretical arguments on business rescue concept supported by the most recent authors and remarkable researchers recognised by the global legislative institutes. This literature review would attempt to argue and to answer the research questions with theoretical framework first, then it would also fit the literature on the business rescue concept under section six of the Companies Act No.71 of 2008 with the aim to assess the reality of business rescue concept application for African Rainbow Minerals Limited. This chapter would start on coherence with the introduction to business rescue concept, its background to bring into legislation, influential factors, competitive analysis of legal nature of the Companies Act 2008 & 1973. This chapter also enlighten on rescue path of financially distressed companies, its positive impact, safeguard creditors to bypass bankruptcy code, financing distressed companies, and concerned role to mitigate the impact of Global financial crisis. This chapter also addresses the theoretical framework of being rescued and sustained evidence of African Rainbow Minerals Limited through the way of measuring the effectiveness of business rescue concept, and then empirical evidence of business rescue concept would be presented from the performance of other large SA companies.

Methodology

Methodology is the third phase of this dissertation that makes it available the justification on how the current research on the business rescue concept under Companies Act No.71 of 2008 would take place and the paper would argue for qualitative research and some extent quantitative research. Malhotra (2009) has demonstrated that the difference between quantitative and qualitative research to collect data and analysis them in different way; for example, qualitative research methods possibly will directly involve on focus group interviews and sometime indirect. Therefore, this dissertation will explain the data collection processes such as direct interviews with the business leaders, policymakers, legislators and social elites of South Africa on their experiencing outcome with the Companies Act No.71 of 2008 with significance the primary and secondary sources. Besides the data collection, limitation on data collection, reliability, and validity of the interviews will also be illustrated in this chapter.

Key Findings and Results

It is the most significant among other chapters, as this part would be based on the practical data and evaluation to bring the suitable solutions for measuring the effectiveness of their business rescue concept to mitigate the impact of global recession of 2009. The tools of statistical analysis will briefly explain by using the several models and the collected data to measure the market risk factors, opportunities, and external environmental influences in order to assess the contribution of business rescue concept under the Companies Act No.71 of 2008.

Discussion

The basic differences between the company Act 2008 and the company Act 1973 is the business rescue provision, which affect to the South African companies to mitigate the recessional impact and provide tremendous opportunities to sustain, but it also increases the number of distressed companies that would be discussed to compare legislative provisions. African Rainbow Minerals Limited would like to expand its business more graciously in export market and contribute to develop the business rescue practice to overcome the impact of global financial crisis started from credit crash in Western countries in 2008 and prolonged recession in 2009.

Recommendation and Conclusions

Finally, the chapter six of this dissertation will scrutinise all the discussion of previous chapter to draw significant conclusion and to point out the key recommendations that will contribute South African legislation to more refine and encourage the business communities for better practice.

Background of the problem

SBP (2010) added that the Companies Act No.71 of 2008 of South Africa is going to be enacted in the third quarter of 2010, by this time an ongoing process to correcting errors, omissions, and rectification is under execution with the view to remove technical dilemmas and weakness identified by the stakeholders through a regulatory impact assessment (RIA). The draft regulations has published at the end of 2009 and opened for public consultation until March 2010, but the public awareness, tremendous responds have deliberated the reality that it would require to pre-release for regulatory impact assessment due to unclean compliance guidance, and possibilities to implementation in 2010 would be delayed.

CACIL (2004) pointed out that the Companies Act, No.71 of 2008 of South Africa has been generated with the creditable objectives to remove red tape influence, upgrading the elevated standards of corporate governance, intensifying rights of shareholder, reassuring the entrepreneurship and keeping full attention to the overall stakeholders. This is a sky scraping legislation of South Africa, which has integrated milestone provision of business rescue while it raised debates with various controversial aspects and to overcome such concerned, and strong criticism, it is essential to take time to incorporate pubic options.

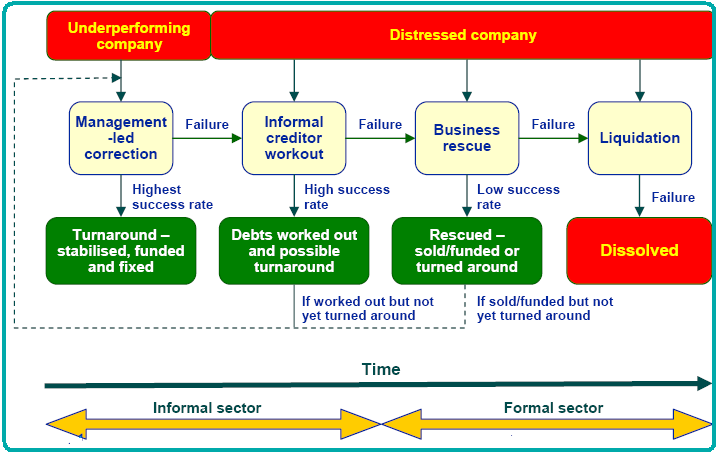

Burdette et al. (2002) argued that the Business Rescue concept under chapter six of the new Companies Act has drafted with very simple language to avoid linguistic complexity and the aim to provide better flexibility to the companies than ever to meet their exact needs; however, there are still enough gaps in the detailed provisions. It also reconstructed the road to business substantially by introducing several new regulatory agencies, turning incorporation procedure easy, and administration of companies, modernizing dogmatic process and way out to rescue any business entry rather than liquidation which traditionally safeguarded by complex legislation.

Khaole (2010) mentioned that the business rescue is an official progression, which the board of directors of an organisation can instigate while stakeholders, trade union, and even employees have the option to activate this preference by the order of court at some stage of liquidation trial setting the organisation under control to start business rescue against any security. Such practice has evidenced under the Companies Act 1973 of South Africa where the route of judicial management was mandatory, but the new business rescue concept under Companies Act No.71 of 2008 facilitated the opportunity to conduct business rescue without any court verdict.

SARW (2009) pointed out that the financial crisis and its recessional impact is diverging to turn back the long struggled achievements of socio economic progress of South Africa by triggering rapid decrease of exchange rate and key turn down in stock exchange for foreign investment concerned securities as well as equities large shares of the big holdings. Though SA has lesser incorporation with the international financial system in relation to other counties, it was predicted to have less impact of global financial crisis, but the reality has resulted in decreasing external demands, worse commodity prices, reduced private capital flows, decreased export revenue and large-scale liquidity trap.

African Rainbow Minerals Limited is one of the largest business entities incorporated in 1994 in South Africa as a miner and exporter of mineral resources such as base metal and expensive metals including coal with tremendous growth and huge contribution to the national economy with eco-friendly technology (ARM, 2006). DEEP SA (2009) added that though the ARM has evidenced to generate highest value for stakeholders including an enhancement of market capitalisation up to 160% but it was difficult for the company to rescue itself from the shocks of global financial crisis and its concerned recession during 2009.

Rationale for the Research

The business communities already presented their clear viewpoints and strongly argued that, there are many missing guidance regarding the compliance requirements and huge contradictory issues those should raise future dilemmas in the implementation process while the business communities always urged for better regulatory practices to generate new policies or legislation that would ensure suitable environment to trade and investment. Moreover, within the Companies Act, No.71 of 2008 there is no provision of RIA1 to ensure better directives to gaining policy objectives of the government with extremely significant tool that can reduce cost, time, and risk for effectual public consultation.

The new Companies Act 2008 is a gradual development of long practice of South African business communities and government where the concept of business rescue provision under section six is a landmark contribution for the business concerns within the shocks of global financial crisis. The academia and theoreticians pointed out that in standard practice business rescue is a creditable perception while any company become financially troubled; it is provision of board of directors to deem rescue solutions rather than liquidation.

There is enough evidence that many small business entries are becoming insolvent in regular practice and liquidating without employing any rescue solution. Under the global financial crisis and recent recessional economy, business rescue concept would principally significant for the emerging economy as route to recovery by avoiding job cuts and allied liquidation. The new legislation of business rescue has flourished new dreams for the South African business communities that it will contribute with proper assistance, but surge of new business failures within the first two years of operation may generate new challenge.

There are huge studies on business rescue concept, but there is enough gap in the area of which variables of business rescue concept would explain the differences in performance with elevated scale of operations, how business rescue concept have substantially with better use of rescuing, sustaining, and enable the companies to achieve extended economics of scale to mitigate recessional impact. To address and identify these gaps, it is rational to have an elevated study on this topic area.

Research Aim and Objectives

The main objective of this study is to examine the performance of the business rescue concept in respect of ARM and to understand how this legislation would contribute to the SA Companies to mitigate recessional impact on the existing entities. Another aim of this research effort is to identifying how the business rescue concept under Companies Act No.71 of 2008 would ensure to flourish new companies safeguarding from financial distresses. To do so, the business rescue concept under the Companies Act No.71 of 2008 has generated huge scope to act as a strong resource of security for the SA companies as an alternative to make business communities free from going to the judicial management to apply business rescue under the existing Company Act of 1973. On the other hand, it is essential to maintain the standard of a legislation conforming with international trends in similar aspects while the new business rescue concept has not only limited its effort on just handling the company, but also providing sound trading status which needed further study. The remarkable area of this provision has regarded as a system for the interim period to shield the company together with any claim of creditor; under such condition the company would be sold with overriding value than a running company in order to deliver the creditors an improved dividend return, which is quite substantial than liquidation. At the same time, another objective of this study is to investigate the scope of financing the distressed companies and the concerned role of financing companies.

This dissertation has aimed to explore the effectiveness of business rescue concept by considering strategic tools and parameters and to assess how the companies like ARM are mitigating the socks of recession 2009 and gaining their emerging position in the market. To do so, this dissertation also deals with few imperative questions, for instance, what the business rescue concept is, or what are its policies for public option, whether it would keep positive impact of Business Rescue provision or not, how business communities planning to argue for amendment and to what extent it would contribute economic growth.

Research Questions

This dissertation has intended to response the following research questions to support the topic area with proper evidence from the South African companies such as African Rainbow Minerals Limited. The main objective of this research is to analyse the implication and effectiveness of business rescue concept under the Companies Act No.71 of 2008 to diminish the financial distress rooted by the recession of 2009 and to do so this paper would raise five research questions and these are –

- What are the factors those influenced the South African legislation to integrate Business Rescue provision for the financially distraught companies under Companies Act No.71 of 2008?

- To what extent Business Rescue provision would keep positive impact to the SA business communities and how does this legal framework would encourage malpractice by the flustered business organisations;

- How Business Rescue provision would safeguard the creditors and bypass bankruptcy code?

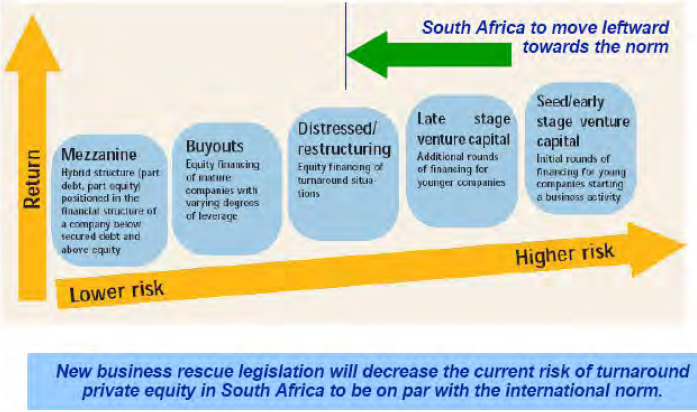

- What are the most significant risk and return measures for the financial institutes to invest on the distressed companies under Business Rescue?

- What were the impact global financial crises on South African companies, and how Business Rescue provision contributed to mitigate the influence global financial crisis by the companies like African Rainbow Minerals Limited?

The raised research questions are very important to examine the business rescue concept under Companies Act No.71 of 2008, and the answers to these questions would ultimately assist to draw the conclusion of the dissertation.

Scope and Limitations of the Study

Projected scopes are

- The topic of this dissertation is unique as it scrutinised that there are no previous research on investigating the effectiveness of business rescue provision to mitigate recessional impact on South Africa. However, many researchers and scholars attempt to research on Global financial crisis and the new Company Act individually with different companies, but none of them has investigated incorporating both issues or considering the African Rainbow Minerals Limited.

- Discussion on business rescue provision for South African companies is also prospective to judging the core problems of the region along with some fruitful solutions;

- The study has the opportunity to acknowledge the business environment by considering social, political, economical, legal and technological factors of South Africa in context of African Rainbow Minerals Limited;

- Most significantly, this dissertation would address the provision of business rescue implication by South Africa in context of African Rainbow, which is a major South African Holdings with a number of subsidiaries. The company is concerned with mining and export of both base and precious metal, there are enough data and reports available in the internet, which facilitated the researcher to achieve goals.

Projected limitations are

The researcher of this study has experienced with various problems in order to complete this dissertation, for instance –

- It was problematic issue for the researcher to organize the dissertation considering both primary and secondary data due to lack of sufficient time;

- Field survey or interviewing process was one of the most difficult tasks for this study due to non-cooperation of the staff and management of African Rainbow Minerals Limited. ARM staff and management have completely denied to take part in the interview and to provide data. ARM behaved in such a way that they have no responsibility to the academia, just profit making is only their motto. As a result, this researcher has to change the respondent group for primary data and also has to depend on secondary sources for ARM data.

- In addition, lack of reliable secondary data sources related with the dissertation topic was another research limitation because chapter 6 of South African Companies Act No.71 of 2008 is the most common area, but what is the impact of this law to mitigate the financial distress caused by 2009 recession is the subject of ongoing agenda.

- On the other hand, it was difficult to access all the site of internet without password, and there are few famous sites for journal articles, which ask additional payment to access previous papers or journal articles;

- As the researcher intended to use both qualitative and quantitative data, it should require huge fund to complete the research, but the budget was not sufficient to afford for this purpose.

Literature Review

Introduction to Business Rescue in South African

Theoretical Framework of Business Rescue

The literature of business rescue has been rooted to the Business failure and success model presented by Altman (1964) though the financial management and academia have long waited to develop an effective tool to forecasting the grounds of economic failure that termed as bankruptcy or insolvency since the 1930s. Altman (1964) demonstrated the reasons of business collapse with five factors, which are the major ratios of working capital, retained earning, profitability, and sales revenues corresponding to the proportion of total assets while the market value of assets presented as a ratio of debt. Business failure and success model also identified that internal ratios of the above factors have facilitated to organise a particular variable that will present a warning to propensity to fail a business.

Argenti (1976) presented another model of corporate failure by identifying a number of non-financial indicators, which includes inefficient management structure, lack of accounting information systems, audit gaps, fraudulent financial statements, useless gearing, and hedging, as well as weak budgetary control including corporate fraud. Buttery and Shadur (1991) presented a more deliberate study on business failure and pointed out some other reasons of collapse, such as insufficient corporate governance, quality gaps, excessive dependency on single product, increasing number of competitors, reduced industrial relation, and failure to respond to the technical development.

Pratten (2004) investigated with the British companies and added more non-financial attributes, such as, unproductive merger and acquisition, failure to respond with the legislative changes, lack of innovation and product diversification, operational gap cause major reduction in customer base and gap of research and development have entrenched to the business failure urged to rescue. Any policy or legislation to rescue business from such failure needed to identify the cause and effect of the failure.

Wrzosek and Ziemba (2009) kept their effort to generate a rating based dynamic model of bankruptcy prediction gathering data from the US National Court Register on the bankrupted companies integrating with models of Altman (1964) and Argenti (1976) with the aim to explain the economy on which the US companies operate and argue to rescue plan. This rating based approach delivered a complete pattern of predictive variables as a coefficient of this model those classify ratings for the companies in accordance with the risk of bankruptcy concerned with individual company.

Scholes and Wright (2009) pointed out that rather than the internal factors of failure of business, in recent era, it has increased the overall business failure linked with regional or global financial crisis and the recession initiated facilities for buyouts to rescue as well as to turn around the failing companies. As the business collapse linked with financial crisis or recession, some operationally failed companies take the opportunity of governmental rescue package. During the global financial crisis of 2008-09, it has been evidenced that to availing governmental rescue packages have turned in to the corporate culture and a number of operationally failed companies sued for rescue package.

Historical background of Business Rescue

Boardman and Chipungu (2010) expressed that the commercial legislation of South Africa have long rooted with the English legal system while the Cape Joint Stock Act and Companies Limited Liability Act- 1861 had introduced by the British colonial rule. Even the existing Companies Act also organised with the principal of British legal system and the reformation of the Companies Act 1973, Britain has contributed with constructing three reviews in 1985, 1989 and 2006, which were reformed respectively. However, it was sole responsibility of Department of Trade and Industry (DTI) to construct Companies Act No.71 of 2008, and it has successfully produced this Act, which would exceed British regulation in some extent, as organising system is far better, resourceful and more effectual in various ways. The business rescue provision under chapter 6 of the Companies Act No.71 of 2008 has wider realistic resources to contribute the economically distorted companies than the UK Company Act 2006 and the US bankruptcy code.

Factors that influenced for Business Rescue

Gewer (2009) identified a number of factors those influenced for business rescue provision, which are the basic cause of business failures in South Africa and laid blame on the international propensity in the direction of rescues, local turnarounds along with workouts. Evidence demonstrated that the existing legislation has very limited option of successful rescues that urged for new legislation while judicial management procedure has failed to prove their efficiency to deliver fruitful rescue in time. Another motivation that worked as a driving force to introduce new business rescue provision is that it was expected while the new business rescue provision would be implemented; it will increase the returns for creditors along with stakeholders.

Khaole (2009) elaborately analysed issues that have seriously influenced the South African legislation and the recognized a number of factors that influenced for business rescue provision while the top concern has kept on macroeconomic environment of SA. Such factors included credit risk consideration, default risk monitoring, risk and return consideration, provision of turnaround finance, lack of debtor friendly bankruptcy code distressed investment scope including the discouraging role of judicial management. Other influential factors like capital provider’s perspectives, company level factors, and source of refinancing altogether are the influential factor behind the new business rescue provision.

Alberts (2004) identified the business rescue provision as a basic shift from the insolvency approach while influencing factors of such legislative changes are international pressure from developing partners like World Bank and UN Agencies arguing that it will keep interest of employees, workers, suppliers and customers and contribute to the steady economic growth. Rather than the interest of creditors and insolvents, it will preserve jobs and provide greater benefits for the creditors as well as to the rehabilitated company in long run.

Content of the Business Rescue Provision

South African legislation Chapter 6 of the Companies Act No.71 of 2008 has defined business rescue as a process of providing one more chance before liquidation to the business entries for a fresh start keeping creditors aside, which is a legislative imitative to rehabilitate the financially distressed companies. Through this legislative imitative, it would impose temporary supervision on management, operation, and property where the rights of the creditors temporarily postponed (Article 128 of the Act)

IDSA (2009) explained that within the direction of the act, the board of directors of the financially disturbed firms have to pursuit a declaration that it is going to start a proceeding for business rescue and would go under supervision of a practitioner appointed by the authority. In this connection, the board of directors would have logical justification to consider that the firm is surely financially bothered or collapsed while it is visible that there are enough realistic panoramas to rescuing the organisation (Government Gazette 2009).

The Act also efficiently integrated the concern of the affected person who has the scope to apply to a court asking an order to placing the concerned firm under supervision as well as starting a business rescue proceeding while the employees and union can avail this opportunity. The Act has kept the provision that at any stage of business rescue proceedings none can take any other legal action against the company without prior permission the practitioner or with a leave petition from the court. It also directed that the practitioner would not allocate any enforcement accomplishment to carry on along with those reasonable amounts of the broad-spectrum moratorium in the ongoing legal action aligned with the company.

Other most vital stipulation of the Act is under section 136, Article 2, it has mentioned that, for the duration of business rescue proceeding continuation, the practitioner possibly will abandon or postpone any proviso of any agreement fully or partially that the firm made for any commencement to any party during the business rescue episode. For any other previously made agreements, the concerned parties can pursue to assert any claim in opposition to the company for damages to the concerned authority or can negotiate informally while this section engaged to express effect of business rescue upon employees as well as contracts.

Chapter 6 of the Companies Act No.71 of 2008 has been headed with ‘Business Rescue and Compromise with Creditors’ and organised with five parts with section 128 to 155 while the first part deliberated with business rescue proceedings and the second part directed regarding the Practitioner’s functions and terms and condition of appointment them. The third part of the Chapter 6 explored with rights of affected people at some stage in business rescue proceedings, the fourth part leads to developing and approving business rescue plan while the fifth part argues to compromising with creditors (Government Gazette 2009).

The most vital provision under chapter 6 of the Act is it part “E” – headed as ‘Compromise with creditors’ where it has provided the landscape direction for the companies to present clear picture of asset and liability to the creditors irrespective of whether they are financially distressed or not. It has clearly mentioned that the board of the distressed company would present a proposal to all of the creditors, which must include- the entire list of all assets of the company with clear indication, which has already been mortgaged, the entire listing of creditors, indication of dividend that would be offered to the creditors while liquidated. It also argued to incorporate other information in the proposal such as entire list of issued securities and their holders, length of time for the projected debt moratorium; hints of debt conversion into equity, action taken for the ongoing operation including an assumed cash flow statement for three years (Government Gazette 2009).

Impact of Business Rescue in South African

IODSA (2009) identified that King III Report is a significant indication to identifying the positive impact and scope of malpractice of the business rescue provision and it is an emergence need of the amendment of the South African Companies Act No. 71 of 2008 where current amendments of the international governance trends as well as Business Rescue provisions have included. Relevance of the King III report in this part of the paper has illustrated both supportive role and the malpractice encouragements for the business community of South Africa as well. Since the King III Report has looked in front of the international business behaviour in order to highlight annual business report execution as well as transparent financial outline of a business organisation. Consequence of this, the Report has involved in following two aspects and in brief, the King III Report has symbolized as either apply or explain.

Firstly, through which manner a company’s economic life has affected by both of positive and negative circumstances during the operating year of amendment of the Business Rescue Provision. Secondly, to what extent a company can be able to take advantage of the positive influences to wipe out the malpractices during the year in advance.

Save the Lifecycle of Business & Provide Opportunity of Fresh Start

Due to liquidity crisis and insolvency, company has scope to winding up by employment of the Chapter 6 of the Companies Act 1973. Conversely, transitional agreements of the Business rescue provision has made scope for the financially distressed companies to start newly or continued their business operation without changing existing company name as well as the registration number. In consistent with the amendment of the Business Rescue provision of Section 16, financially distressed companies should make a notice of file within two years of Business Rescue and in addition, during general effective date of the Act. Alternatively, in the light of Section 21 along with Section 53 (b), a company has an opportunity to re-enter into market by filing their name and registration number within 20 business days after Business Rescue file has opened (Zurnamer, 2008).

Reduce the Red Tape of Judicial Management

South Africa is prominent as a creditor friendly region for the business holders. Before amendment of the Business Rescue mechanism of the Companies Act 71 of 2008, judicial management was tremendously time-consuming and costly as well. After amendment of this provision, involved parties have justified liquidation or the solvency potentiality of the financially distressed company first and afterwards decided whether the Business rescue provision would be suitable to apply. Since, the Business Rescue provision has also termed as compromise with creditors, the involved parties of an organisation has scope to get advantages from Section 129 (3) (b) either to claim rights from the company or to draw a business rescue plan for prompt liquidation to resolve the financial distressed. (Eversheds 2010)

Generate mobility & Trust for New Starters

During business rescue proceedings, new birth of a distressed company has scope to enjoy several advantages under the Section 76 of Chapter 6 (Braatvedt, 2010). This Section has defined about obligatory principles of the directors of the company. Therefore, new investors as well as the shareholders have always attached with every operation and function of the company. On the other hand, Section 75, 76 and 77 has kept some attributes to avoid statutory duties of the directors, but significance of these Sections have not provided any ease to relief from duties and accountability of the directors. (Mclaren & Modika, 2009)

Provide Sustainability for Business

Another demand of the Business Rescue provision has required an integrated sustainability report during renewal of the company’s business operation. Most significant result here has generated both transparency and accountability throughout effective communication with stakeholders2 in order to make strategic decisions to look forward into the company’s economic values and in addition, to attract potential shareholders/investors. Conversely, sustainability scope of the Business Rescue has able to also illustrate a comparable outline with the companies past performance. Financially distressed companies in South Africa can have enjoyed lots of auditing support during Business Rescue. For an effective Business Rescue result, companies should fabricate financial reports3 at the end of each year to highlight creditable sustainability in order to achieve consumer’s loyalty. Alternatively, sustainability is an effective tool of the Business Rescue to redefine company’s strategic vision as an essential ingredient of the Company’s DNA. (The Business Leaders 2009)

Creditor Debtor dilemma (Discharge of debts)

Amendment of the Business Rescue provision has not kept either any enforceability of the residency requirements for the debtors or distressed firms or any consent of the creditors for the debt discharge. Additionally, modernization of the debt relief administration has outlined in such way that an insolvent debtor has opportunity to replacing by just one of the Three Person Commission (Jones, 2010).

Effect of business rescue on employees and contracts

During Business Rescue proceedings consideration in favour of current employees as well as remaining contracts, amendment of the Act has discussed and outlined about directors liability in the Section 78 and Section 247 respectively. In proportion to the Section 247, Sub-section 1, non-executive directors of a company has option to exempt from insurance liability of an existing contract. Alternatively, amendment of the law has also attached the directors in order to exempt or void from any type of negligence, default cases, breach of duty, as well as breach of trust. On the other hand, Section 78 (5) & (6) have expressed limitation of the law that liabilities of the directors or any type of fraudulent conducts in relation to the company or their employees would have not enough protective in favour of the insurer and insured (Mclaren & Modika, 2010).

Rights of Affected People

Affected people during business rescue has classified into several terms such as employees, creditors and company securities or the shareholders. New amendment of the Business Rescue provision (Chapter 6) has kept several proceedings to compensate the affected parties of the firm. Employee’s trade union can resolute to claim their official allowances like medical allowances, pension schemes and the monthly salary payment under Business Rescue provision of the Section 152 (1) and Section 153. Additionally, affected creditors have also resolute in the light of Section 152 (1) and Section 153 to acquire their payable. Creditors may also resolute under the Section 151, Sub-section 4 (b) and 5 (b) within 15 business days. On the other hand, shareholders either may reject or approve the Business Rescue plan of the company and additionally, have authoritative power to claim their acquired shares or handsome value against those in the manner of Section 152 and 153 (Government Gazette l, 2009).

Directors Duties and Shareholder Remedies

Current amendment of the Business Rescue provision has kept significant the directors that appraisal right remedies of the shareholders should focus rights in favour of the minor shareholders and the point is a new concept of South African Companies Act 2008 as well as in the Business Rescue provisions. Consequence of this legal aid, shareholders would have taken several triggering actions. For instance, Section 112 has undertaken major part of the assets to dispose, Section 113 conducts merger or acquisition and the Section 114 has outlined instalment programs of due payments. Affected shareholders during business rescue have legal right to resolution and demand their fair value of shares within 20 business days. Alternatively, according to the Section 166 and Section 164, affected shareholders can be resolution to court for fair value, which should have accumulated handsome interest rate on payable money (Mclaren & Modika, 2010). On the other hand, in the light of Section 76, directors of a distressed company have assigned to do their functions and duties and in Section 75 have provided the treatment of financial concern4.

Lacking of Regulatory Impact Assessment

Though the new Companies Act 71 of 2008 (Chapter 6) has generated several prospects towards the affected companies as well as the affected parties, but there also have diverse limitation to re-enter into market and slower regulatory assessments. In brief, distressed companies under Business Rescue proceeding have currently passed through “hurry up and wait” state of affairs. In time of re-entry, companies are instructed to waiting for presidential assent to get starting to operate next step. Regulatory assessment has delayed here for two major aspects. First, the DTI5 has needed to conduct a Takeover Regulation Panel as a relating matter to functioning Business Rescue proceedings and additionally, the DTI has published these matters to justify public comments before finalised. Second, reform of the distressed firm should transform them and construct the CIPRO6 for addressing mandatory inconsistencies to modernise the course of conduct. Alternatively, roads of the new Act has committed to implementation of MOI7 in order to deviate difficulties of the MA and AA. Consequence of these regulatory assessments would not have effectively impact to recover company’s financial distresses, but have around two operating years go under water (Mclaren & Modika, 2009).

Lack of Guidance for Financing Institute

At the early stage of the Business rescue provisions under the Companies Act, business rescue has presented as discussing on trade-off among lenders (financial institutes) and borrower (distressed company). However, section 136(2) of this regulation has argued that business rescue practitioners have the authoritative power to suspend any provision of the agreement during business rescue proceedings with and without reasonable cause. On the other hand, inner-sense of the rescue provisions has claimed to utilize surety ships in order to safe corporate debt which should to grant by a third party to secure obligations of the lender. Additionally, credit transaction by the lender would have secured in the company restructuring levels with loan agreement including the third party selections in terms of guarantee and guarantor as well as loan agreement, rescue provisions has not yet outline any unambiguous direction in this regards. Considering this limitation, financial institutes cannot exercise any pre-defined loan agreement towards borrowers (Mclaren & Modika, 2010).

Controversially Linked with Business Rescue

After amendment of the South African Companies Act 2008 (Business Rescue provisions), South African Trade and Industry has officially declared that, the new Act has fluctuated from the fundamental flaw of the Business Rescue provisions. Groups of legal practitioners as well as the academics have wondered about major errors of the primary formal issues. Moreover, Section 218 (1) has represented modes to resolution; several deed provisions and terms of void any deed enforceable to declare by court. In brief, all of these amendments have quite inconsistent with principal Business Rescue provisions and hence can be termed as a legal nonsense (Mclaren & Modika, 2010).

Business Rescue & Debtor-Creditors Friendly Environment

Debtor Creditors Safeguard

Under Business Rescue Provision, creditors of an organisation are the affected parties in time of financial crisis. Creditors are of two types, according to the Business Rescue Provision, Section 144 (2) employees have regard as direct creditors, and directors and other practitioners have treated as indirect creditors by the Sub-section (2). After notification of court for Business Rescue proceedings, creditors as well as other affected parties have an opportunity resolution to court under Section 129 (Sub-section 1) in order to compensate. During liquidation after Business Rescue proceedings, affected creditors have right to be notified within five business days, which said in Sub-section 4 to 5, and Section 132 (2).

Though during continuation of Business Rescue proceedings, there have no scope to proceedings any legal prosecution against the company, but the direct creditors have right to continuing their employment scope attaining predefined terms and conditions. Moreover, in case of any type of employee retrenchment, employees could resolution to court in terms of Labour Relation Act 1995 (Act No. 66) which have inconsistent with the Business Rescue Plan (section 189 & 189A). Alternatively, Act No. 24 (Section 35A & 35B) of the Insolvency Act has argued that indirect practitioners of a distressed company could be denied or suspend any of the provisions of the Business Rescue either entirely, partially or conditionally, and the provision has also liable to benefit the direct creditors in terms of employment agreement. Both the parties’ direct and indirect creditors can be got a supplementary benefit to be compensated subject to the Sub-section–2.

On the other hand, if the Business Rescue proceedings have conducted as a conversion of liquidation, creditors should be treated as the liquidator of the corporate body who could have claim remuneration to work performed as well as compensation for the incurred expenses. Business rescue proceedings have the authority for the directors to be continued their functions according to the predefined authority of the practitioners. Under the circumstance, Section 75 of the business rescue provision has performed for the financial interests of the directors of distressed company. Section 76 has structured how directors could be relieved from duties where as Section 77 as well as the Section 77 (3) (a), (b) & (c) have defined about the liabilities where each single action has required approval of the practitioners on behalf of the affected company. Amendment of the Business Rescue provision additionally benefited the practitioners that they could be resolution to court to claims any of their rights in the light of Section 162, Sub-section (5). After notification by court of business rescue proceedings, practitioners have secured to investigate company affairs like business operations, property, as well as financial situation according to the Section 130 & 131 (Government Gazette 2009).

Bypass the bankruptcy code

Inconsistent with the Business Rescue provision, South African corporate bodies have opportunities to bypass the bankruptcy code with the aid of two forms- voluntary winding up of the company members or creditors and scope of deregistration of the corporate entity. A brief account of these two forms is described below. (Zuylen & Gilfillan 2009)

Voluntary winding up of the creditors

Comprise with the circumstance of insolvent entity, corporate members or the shareholders of an organisation have scope to apply to court for the dissolution or winding up their corporate entity in order to protect bankruptcy. Alternatively, corporate members have also an opportunity to close company through the procedure of voluntary dissolution of the creditors based on 75 % majority. While performing the method, two prime conditions should consider by the entity. Firstly, there have no scope of distinction and second, members of the entity should follow unanimous agreement for dissolution of the company.

Scope of deregistration

Deregistration in another form to close or dissolution of a company that protects from bankruptcy code. Key attribute of company deregistration involved in cancellation of an organisation’s AA & MA8 in accordance with the Companies Act K 73. Additionally, deregistration procedure involved with the Close Corporations Act (Section 26) during cancellation of close corporation’s founding statements. In accordance with the Section 26, registrar of the close company should affirm that currently, the company has not involved in trading due to reasonable cause and in addition, in favour of the company has no assets and liabilities. Registrar of an organisation should keep in mind that deregistration and liquidation are diverse from each other in case of special dissolution or in term of compulsory application for dissolution to court. For the insolvent entities, deregistration has simply made scope of unenforceable debt where as insolvent company’s debt could be expunged by liquidation, but the existing debts would be further enforceable if the deregistered entity would conduct re-registration and the liquidated entities have no scope to re-registered.

Risk Measures for Recessional Influence & Business Rescue

Financial System Stability of South Africa

The South African Reserve Bank has strong control over the SA financial system stability including its monitory policy, budgetary control while SARB9 expressed its deep concern with the global financial crisis and its recessional impact. SARB also kept its strapping role to reform the banking and financial institutional regulations to respond to the business rescue provision, which would be necessary to financing the financially distressed companies urged to rescue (SARB 2009).

Mnyande (2010) strongly argued in the annual financial planning convention that being a comparatively less open economy, South Africa has not suffered the bursting economic disaster of the global financial crisis of 2008, which the European and US economy evidenced. It is not just fortune, but the success of South African policy respond to its economy for which the banking sector of SA including its wide financial market has successfully escaped from the impact of global financial crisis comparatively untouched while the European and US baking, property mortgage market distressed people to be homeless.

Guma (2010) mentioned that the central bank of South Africa SARB has introduced FSD10 in 2001 with the aim to identifying probable threats of financial instability along with advocating the vigorous route to mitigating those risks in favour of the central bank. In context of global financial crisis of 2008, the development agencies are suggesting the central bank of different countries to take the responsibility of financial stabilisation among the domestic markets while FSD for about a decade proved its effectual role of micro-prudential supervision to financial stabilisation. The FSD has time to time reformed the monitory policy, identified the systemic risks, reformation of banking sectors including insurance sector and restructured rating agencies, efficient hedge funds, and competent accounting standards to maintain sustainable development of South Africa.

Financial Institutions & Associated Risk

Mnyande (2010) mentioned that the World Bank, IMF,11 and G-20 agenda has identified the associated risk with South African Financial institutes are the regulatory concern of monitoring and recommending the market developments, guiding and supporting the best policy best practice by maintaining regulatory standards. The development agencies also indicated risk with severe capital requirements, securities, off-balance-sheet items, effectual crisis management, and lack of cooperation with international agencies while the country is under recovery of the impact of the global financial crisis.

Guma (2010) pointed out that the macro prudential approach of South Africa has many diverse attempts to define the associated risk of financial institution and banking sector with the concept of International Settlements. The assessment of risks under SA macro prudential approach concerned with the time dimension that argues with process how risk go forward over time and next it looks for cross-sectional aspects that deals with the method of how risks are allocated with basic exposures and linkage between the policy and practice. South Africa is thus continuously reforming its fiscal policy with moderate monitory regulation to ensure an integrated behaviour of financial institutions with the aim to mitigating risk while the policy respond evidenced positive signs of recovery in SA economic.

Policy Respond to the Risk

The global financial crisis 2008 and its consequential recessional economy in 2009 has generated to extensive debates in South Africa on the necessity of improving international cooperation regarding the regulatory framework to reinforcing the global financial system improvement for flexibility to respond at any further financial crisis.

The policy makers of SA think that the risk to global financial sustainability has eased while the systemic risks are continuing to collapse due to the global economic recovery has already gained momentum progress and the recovery has involved in reasonable level of uncertainty. It has argued that the developed western economy have had strong financial stability, but why they collapsed and totally failed to respond to the global financial crisis, policy that fragile the economies and damaged financial systems, why South Africa would go to accept them. South African economy has overcome the hardest hit of the global crisis without any major collapse in banking and property sector, but just evidenced decreasing price and export exchanges. Meanwhile South Africa by introducing regulatory reforms, and preserving comparatively conservative monetary and traditional fiscal policies with necessary structural reforms earlier than the global financial crisis have facilitated SA to endure the impact of recession 2009 far better than prior crises. The major risks left behind South Africa is the downward stress on the commodity price that may discourage the governmental revenues generation along with elevating public debt towards unsustainable altitude (Guma, 2010).

South African policy respond is thus in four dimensional pressure such as international pressure to liberate conservative strategy, sustaining stable economic growth, sustaining policy success that faced global financial crisis and implementing business rescue provision.

Action for Legislative Change

The Financial Stability Department under the central bank of South Africa has taken the liability to reform the banking sector to respond the necessary amendment for business rescue provision under the new regulation along with recovery of global financial crisis. FBD has successful record of accomplishment to generating legal framework to regulate as well as supervises banking and financial sector of South Africa integrating with local and international standards. To reform the banking regulation it will be needed to amend the Banks Act- 1990 including the Mutual Banks Act- 1993, to do so FBD already started to review the old legislation to identifying the areas of required change. After making a comparative study, they will issue a report with particular identification of section required to adjust and submit to the Minister of Finance and the ministry will then recommend to the legislating body to take necessary action.

Global Recessional Influence on the South African & ARM

Global Financial Crisis 2008 & Concerned Recession of 2009

The occurrence of the contemptible recession of 2009 was not a sudden incidence, but rather, a result of a long period of mismanagement and numerous consequential events. The fall in sub-prime mortgage market of the US has generated serious liquidity trap in the US banking sector, the resultant effect of which influenced the international financial markets and spread out the liquidity trap and analogous financial dilemmas to Europe and later on to Asia and Africa.

This has caused some severe impacts on the US investments and the country moved its investments from the stock market to oil investments; subsequently, the fuel costs rose at the highest peak of the history. Following all these, the most alarming issue that has increasingly accelerated amongst the major players of financial institutions was the trend of bankruptcy. Consequently, the financial crisis transmitted all over the American commercial bodies, Europe, and rest of the globe the result of which was the recession of 2009. The French bank BNP Paribas has indicated high interest rate as the central ground of the financial crisis. The governments have extended their hands to overcome the situation with bailout bill and other rescue package (for example, the$ 700 billion bailout program by US government and the £400 billion bailout program by the UK government), but the problem entrenched for long run. The bankruptcy of Lehman Brothers was the prevailing collapse of an investment bank in the course of fraud and regulatory failure that has reflected the paucity of American economic order.

Recessional Impact on South Africa

Southern African Development Community (2009) suggests that South Africa formally came into recession in May 2009 as the global economic crisis hit the key drivers of growth – trade, investment, mining and manufacturing sectors – in addition, the economy faced a fall of 2% in 2009 for the first time in last seventeen years history. Baxter (2010) argues that in the first three quarters of this financial year alone, the financial system of South Africa confronted a job cut of 959 000 employees; like in many other nations across the world, the global economic crisis has impelled its government to play a more vital role in the national economy. Efforts to counter recession made the South African government to execute bailouts and uphold extensive stimulus packages, such as the public infrastructure investment programmes; in addition, government established a training layoff scheme as part of its national “framework response” to the global economic crisis; more recently, the government announced the release of the most talked about Industrial Policy Action Plan. This plan will target certain economic sectors for relief, while providing incentives in product innovation in the clothing, vehicle manufacturing, and green industries to stimulate job creation, nonetheless, execution of these activities specified in the “national framework response” has been sluggish and it has already become perceptible that the most susceptible class in the economic-storm is the poor people.

Additionally, economic turmoil interconnects another global crisis that is, the ecological concerns of international trading activities; but deplorably, RSA’s incentive-packages to promote growth in green industries remain few, as it is heavily reliant on carbon-heavy, low-priced coal energy and is facing critical electricity supply-shortages; therefore, solving power supply challenges should be at the heart of RSA’s growth and development policy. During the fiscal turmoil, dawdling economic growth in main export markets, together with lesser commodity prices and a deceleration in capital-flows of the third world nations had put a great influence over the RSA economy; whilst components of domestic-economy were in recession, including automotive, mining, and retail sectors, it was hard differentiate domestic/international factors proportionately with slowdown of sectors. On the other hand, it is arguable that the South African economy even in non-recessionary periods, exemplifies high rates of unemployment as a feature of its economic system, therefore, it is obvious that the downturn’s affect will be to shoot up poverty and inequality in context of the key insinuations for the combination of the nation’s democratic system. For an undersized and business responsive financial system like South Africa that is very much reliant upon international trade and drawing foreign savings to bolster domestic investment, it is quite natural that the financial stress induced economic-slowdown would bring a great impact over the export-based nation and subsequently in its GDP.

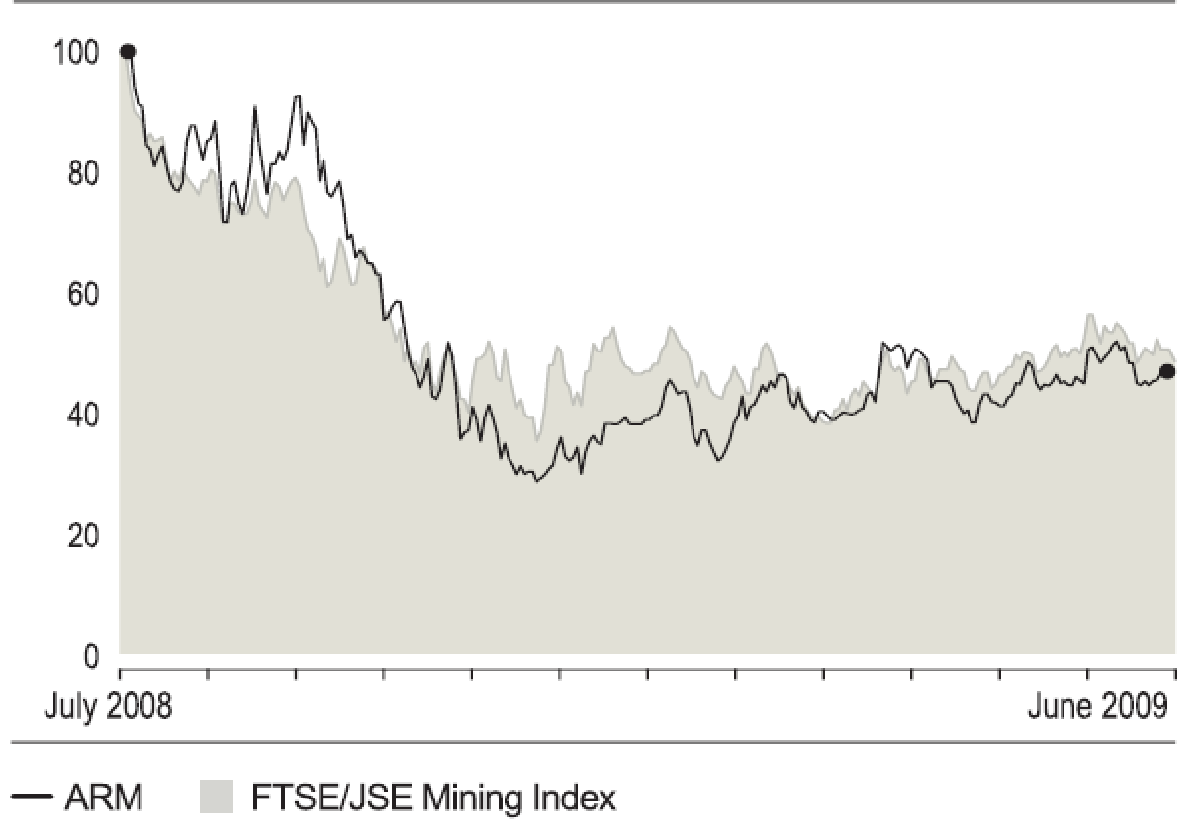

African Rainbow Minerals Limited under Recessional Economy

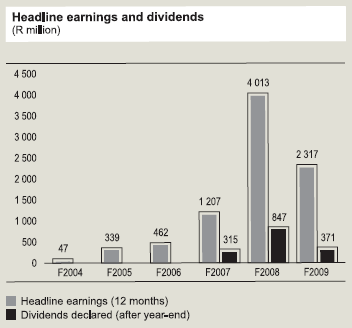

The South African mining industry has suffered from severe losses during the economic turmoil. Even in early 2010, when the international mineral producing industry was observing some levels of recovery, the mining-sector in RSA faced unrelenting slow down and the nation has not been able to take any benefit from the international economic-boom (Stiftung, 2010). Whilst the entire industry was subjected to the crisis, being one of the major players of the South African industry, the adverse affects over the African Rainbow Minerals Limited was not just limited to diminishing profit margins, but also to the operational hindrances as a whole. Embellished by all the flinching economic determinants, such as falling demands, rising operating costs, fluctuating exchange rates and volatile inflation has caused the ARM to experience a decrease in earnings by 42% from R4.0 billion to R2.3 billion, and a decrease in profit from operations before exceptional items by 44% from R6.7 billion to R3.7 billion. Schumacher (2009) states that owing to escalating costs of commodities, raw material and machinery required to carry out the operation of the company, African Rainbow Minerals expected that the capital expenditure (capex) of R3.3 billion in 2009 may amplify by R8 billion over the next three financial years.

On the other hand, the company’s platinum division continued its weak performance in spite of record sales and the platinum group metals (PGM) selling price reduced by 32 percent as compared to the previous financial year; consequently, ARM Platinum recorded a loss of R3 million – a considerable drop from the fiscal year 2008 R1.3 billions of profit margin. ARM (2009) suggests that the Coal Division of the company has added R135 million as its net income, which was down from R175 million in FY2008 because of the financial depression, and ARM observed a plunge in demand for inland and Eskom featured coal, together with a decrease in demand to export coal over the first half of FY2009.

Research Methodology

Introduction

The key purpose of the research methodology is to illustrate how the preferred research approach will go with the ultimate goal of the dissertation investigation, and how this approach practically implemented in the present study. Malhotra (2009, p.9) pointed out six major steps to design the research paper and Yin (2003) addressed the case study approach. However, the author of this study will consider the major steps of Malhotra in order to organise the dissertation, as this research approach is easy to follow for a long research. In contrast, Yin (2002) stated that case study approach is not appropriate while the research questions start with “how” and “what” as this approach deals with a single problem.

Research Approach

Marshall and Rossman (1999) and Sekaran (2006) suggested that qualitative and quantitative approaches are the two main types of research approaches. The researcher would focus on preparing an assessment of both qualitative and quantitative research throughout this paper, as it is arguable that the secondary data has been organised scrupulously whereas the quantitative part provides the chance to take a precise idea about the perceptions of the respondents surveyed. In addition, the paper would also concentrate on inculcating numerous methods to assemble the information collected from the field survey.

Primary research

Zikmund (2006) and Saunders, Thornhill & Lewis (2006) argued that the primary data originated for the particular reason, or identified the research dilemma by using selected research approach. On the other hand, Miles & Huberman (1994) and Yin (2003) pointed out the difference between primary and secondary research approach. They further addressed that primary research is important to gather proper outcome though the entire process is time-consuming matter. In addition, the author will interview at least 50 business leaders, policymakers, Scholars, and employees of renowned companies. In addition, “African Rainbow Minerals Limited” is large company, which was affected by the global financial crisis, so target groups have practical experience about the recessionary impact, which will help the researcher to gather primary data.

Interviews

According to the view of Saunders, Thornhill & Lewis (2006) and Malhotra (2009), face-to-face interview is the best procedure to collect primary data from selected respondents. As a result, the researcher decided to collect data by using this process, though many respondents denied giving their valuable time for this purpose. In this context, the researcher used other instantaneous approach (like phone and email) and sent the questionnaire to the respondents as the respondents would fill up the questionnaire at their convenient time.

Data Analysis process

To analyze the data, this dissertation would consider a number of techniques; for instance, the researcher would review all the completed form of questionnaire to check the presence incompatible and fabricated information, remove unintentional errors about the business rescue concept under the CA No.71 of 2008. In addition, the author would recheck primary data in terms of connected secondary data, comparing with other the relevant information of African Rainbow Minerals Limited, and after following this procedure, the author would use Microsoft excel in order to represent collected data graphically.

The data analysis for this research within the same geographic region, all potential data collection from the interview has pre-approved by the University appointed Superior of the researcher, without any authentic data or information analysis and whenever the approval has taken place, all of the redundant information gathered from the interview questionnaires would be rechecked to protecting unfairness. However, the qualitative data generation technique is most reliable and valid for all type analysis while the present interviews and research of this paper has conducted by utilising the qualitative research module.

Importance of Secondary data

According to the view of Malhotra (2009, p.107), secondary data has already published and processed data for serving the present purpose while these sources acknowledged by the publishers, universities, academia, and renowned scholars. Cohen, Manion & Morrison (2007) pointed out that descriptive research should based on the qualitative research because these are reliable sources and derived from significant research. Most importantly, the author has organised the entire literature review and discussion chapter considering the qualitative data though the researcher faced some problem to find out relevant sources to formulate these chapters. In addition, the researcher has used numerous management books, law journal and books, annual report of African Rainbow Minerals Limited, relevant financial report on the selected company, SAGE journal articles, and other online resources.

Questionnaire Design

Formulating a questionnaire is one of the most important tasks for this study because as it will guide the author to identify key problems and reach a conclusion (Saunders, Thornhill, and Lewis, 2006). In addition, the response from the respondents will help the researcher to recommend possible solutions to the relevant policy makers, legislative bodies, and other beneficiary groups. The researcher will apply few steps, for instance, identifying the required information, and interviewing method for this dissertation, determine the content of questions, formulate the question structure and in accordance with the research objectives. However, Cohen, Manion, and Morrison (2007) expressed that the author can design a questionnaire by adopting his own skills, as it is not a pure science, but an art. At the same time, they stated that questionnaire will point out the research problem, thus, the respondents get the opportunity to specifically response. Therefore, the outcome from the research will not be general, but it will be rational with the topic. Simultaneously, this dissertation focused on this area because four chapters (especially Findings and results, recommendation and conclusion) of this stuffy have direct connection with the response of the respondents such as policy makers, scholars, and so on. However, it is essential to argue that the author has formulated the questionnaire with easy questions because the respondents will be interested to complete the whole form. However, the next table demonstrates the elements of two sections to provide clear idea about the questionnaire –

Table 1: – The questionnaire design process

Source: – Self generated.

Limitation of Data Collection Process

Companies Act No.71 of 2008 has introduced few new options, which will be implemented from this year. In this context, it is difficult to find out proper secondary articles on the application, implementation, and adverse impact on the business. In addition, there are many relevant research papers on the economic impact of global financial crisis in the company, but no research on this Act or implementation.

On the other hand, primary data collection was a challenging job for the researcher, as most of the selected respondents have no clear knowledge about the impact of new provision of Companies Act No.71 of 2008 on the business organizations because implementation process is still going on. As a result, the question related with the impact of bankruptcy and business rescue concept was difficult for the employees to answer. However, the respondents were too busy; therefore, the researcher had to spend a long time for their response.

Review of Data Collection Method

The author will dispatch 300 questionnaires among 75 respondents of different sectors and it is expected that most of the respondents will complete at least a single questionnaire. Here, it is important to express that questionnaires will be self-generated with different parts. The researcher will use both face-to-face and instantaneous method to gather data this paper.

Measurement and scaling process

The purpose of this part is to discuss the measuring scale –

- Nominal scales: This kind of measurement process indicates non-numerical questions, such as, name of the target employees or ethnic group or age of them;

- Ordinal scales: This sort of measurement method concentrate on exact questions in order to assess relative attitudes of the employees of the selected company;

- Multiple Choice – Single Response: At this point, employees would get at least three options, but respondents have to select only one option;

Table 2: Measurement stage with Scale Types in Questionnaire

Source: Self generated

Sampling

As it is difficult for the researcher to contact to the entire management and staff of ARM and a costly affair and almost impossible, it would be better cautiously choose a sample from different units of different sectors, which will derive credible result through the designed questionnaire to interview. Moreover, it is expected that this result will reflect the position option of entire population in context to their view on business rescue and it is not straight proportionate to the whole population and the data possibly will consist a marginal of error.

However, the respondents consist of Freshman University Graduates who are the most competent person or top-level executives working at the different business units of South African companies.

Feasibility

It has already mentioned that the researcher will communicate with the South African Companies, Scholars, and policymakers to obtain data regarding business rescue under new law to use in this dissertation. All the necessary information about the ARM is available in the company’s website and the financial report and annual report 2009 of this company is available as “African Rainbow Minerals Limited” is a listed company. In addition, the researcher of this dissertation has access to the major law firm that pioneered the presentation seminars about business rescue in this country, as the company is the law firm’s major client.

Ethical Issue

This dissertation would keep its enthusiastic attention on two ethical issues, which are diverse nevertheless interrelated with each other and based on the central point of conducting such any qualitative research together with research in strategic evaluation and these ethical issues are the representation of truth as well as confidentiality. The ethical issue of representation of truth affects the exceptionally on the procedure of carrying out qualitative research including data gathering and data analysis and ultimately gaining the outcomes without any bias. The other ethical issue is the confidentiality concerned with respondents and the services triggered by the above-mentioned company who has remarkable contribution to the economy. Both the ethical issues engross an influential relationship between the researcher and respondents, and it comes together with the consequence of other ethical issues, such as, susceptibility and corporate social responsibility while the respondents feel hesitant to come in front of public.

Reliability & Validity of Interviews

It is crucial to assess what are the facts and motivation that have enacted behind to prefer an interview with the management of ARM and few operational managers rather than supplementary resources of the data collections. The most remarkable motivation of such an interview is that, according to this author’s believe, their involvement with the target respondent groups would make appropriate sense to the response. Moreover, a discussion, which intends to take place with one of the members of management team of ARM, such as materials would be further rewarding than any other potential sources. In view of the fact that the target respondent groups would be at the top awareness of comparative to the research concerns, such as what are the clear vision and difficulties of the business rescue concept, or what kinds of amendments require, and how the business rescue plan may misused for bad game and how it would bring successful outcomes.

Contingency Plan

The emergency plan would explain that the company analysis of ARM and strategic decision-making to interviewing through questionnaires and the collected data or information would not enough sufficient for the overall analysis of Business rescue provision if there is no option to terminate or integrating any potential rationale to overcome limitations. In this case, the research techniques have to transform comparing with the previous guidelines or principles, for instance, here the qualitative scheme would be better as well as easier to collect data for the analysis of the viewpoints of ARM as a strong representative of the business communities of South Africa.

As the qualitative research tactic would be applied for this study, several off-line observation tools like the questionnaires, different publications, survey reports would be considered useful tools. However, practice of this guideline may not be helpful without the reduction of time limit as well as proportionately increasing the accuracy of the outcomes for the research. Moreover, observation of both provisions, sections mentioned in the Act and the existing gap has enriched the researcher’s perceptive. To avoid biased or favouritism, the researcher will accumulate numerous questionnaires by utilising magazines, journals, books, articles, which have written by renowned researchers and enthusiastic authors

Findings and Results

Section A: About Respondents

Question 1 to 5: Introductory questions

Section A was designed with some formal questions such as name, age, job position, gender, contact details of the respondents. This section would help the respondents to carry on with relax mode; however, personal information of the respondents is the subject of data protection act.

Section B: Survey Questions

Question 6

Are you familiar with the content of business rescue provision under chapter 6 of the Companies Act No.71 of 2008?

The aim of this question is to recognize about respondent’s knowledge on business rescue provision under new act and this is an important question because only those respondent’s would proceed who have knowledge on this research area. However, all respondents argued that they are familiar with this issue and have sufficient practical experience to answer the relevant questions regarding the consequence of new act.

Question 7

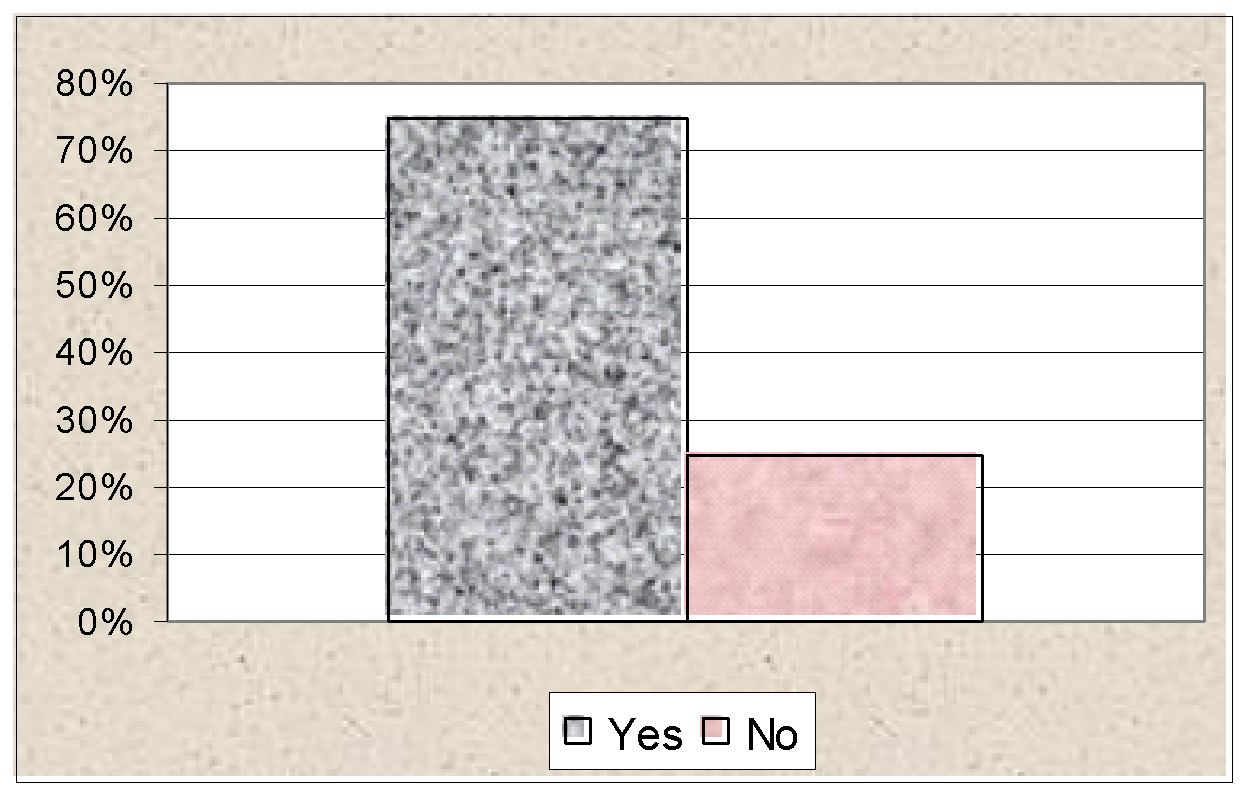

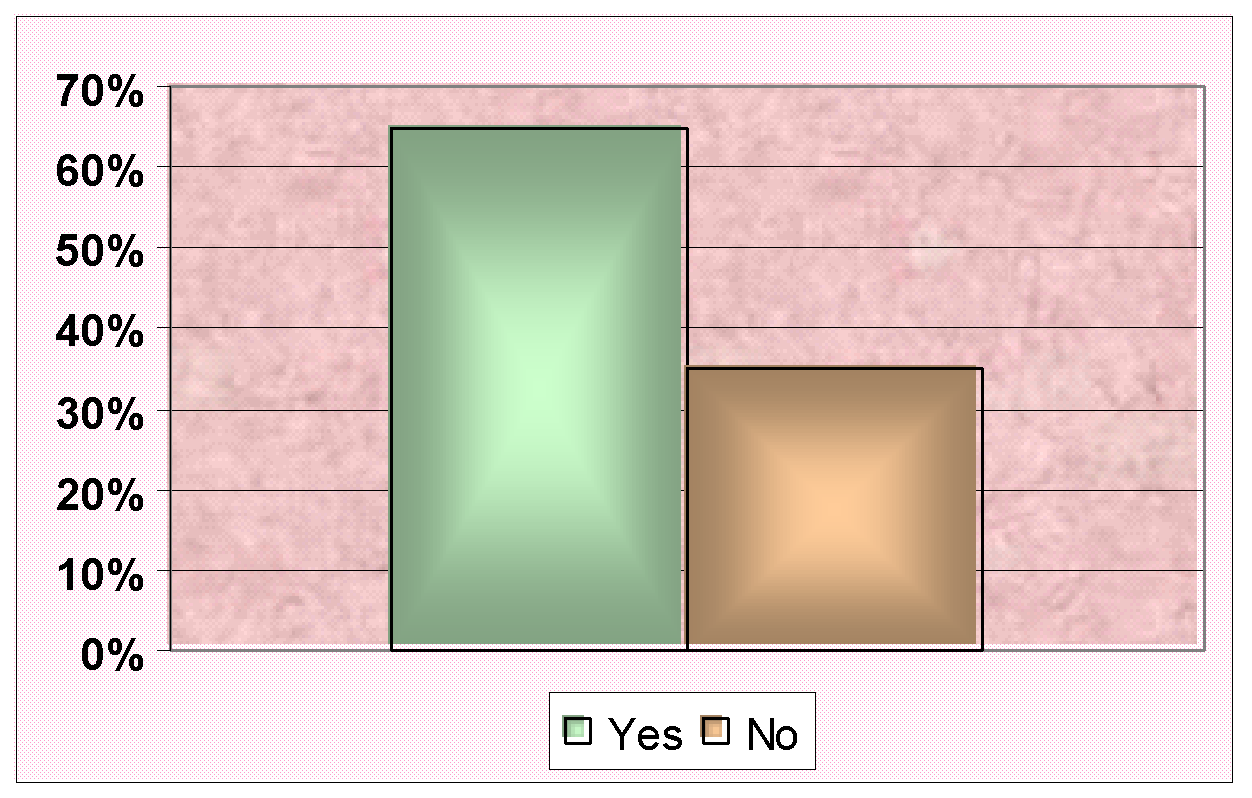

Do you think that the Business rescue concept would be able to provide long run economic benefit?

According to the survey report, around 75% of the respondents selected yes option and only 25% respondents give negative response, which demonstrates the expectation of the scholars to the business rescue provision.

Question 8

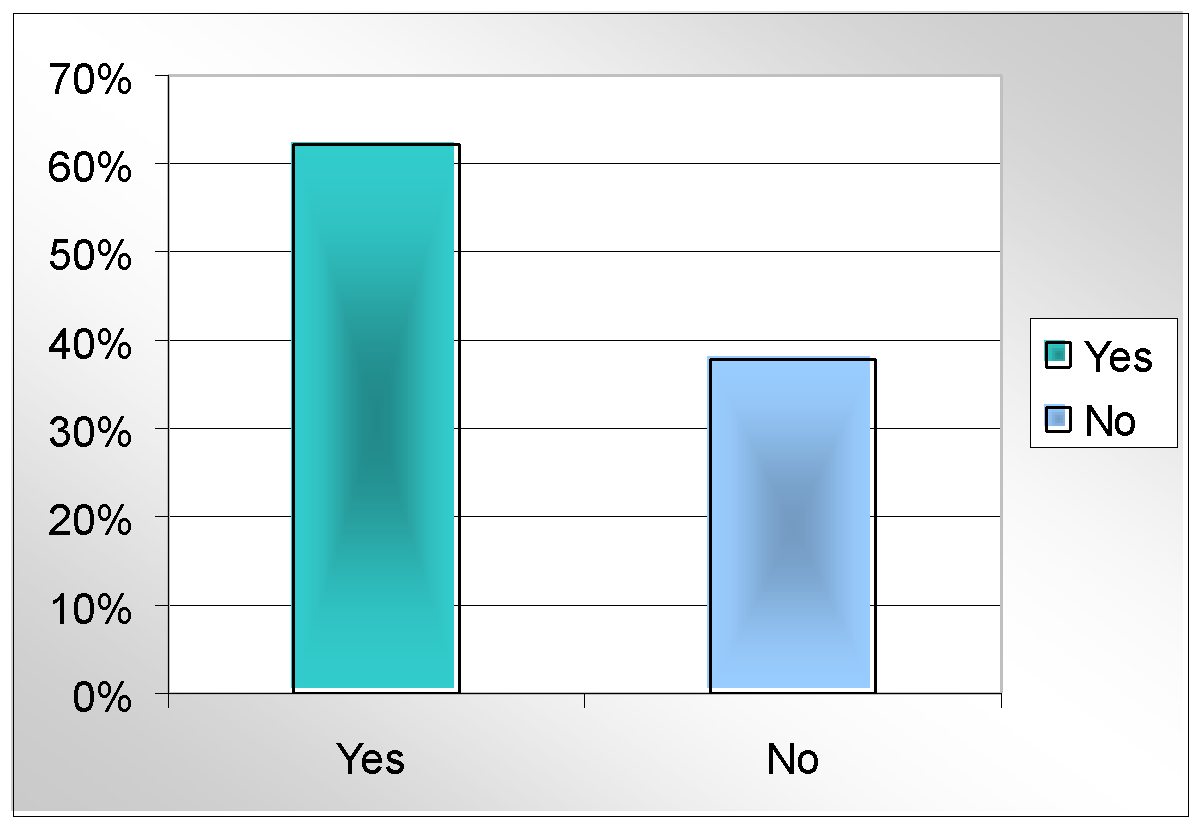

Does the insolvent companies would be capable to improve their position through the highest encouragement debtors under chapter 6 of the Companies Act No.71 of 2008?

The researcher has designed this question in order to identify the impact of new law on the insolvent companies, as these companies will get the opportunity of fresh start with rescue package. However, out of the 50 respondents of different sectors, 31 respondents (or 62% interviewees) stated that this law is able to improve the position of the insolvent companies.

Question 9

Do you think that, the unclean provision for creditors would threaten the financing institutes under business rescue?

From the answer of the interviewees, the researcher identified that 60% of the total respondents said financial institutes would be under risk in case of bankruptcy while 40% provided different view.

Question 10

Do you think to rethink about creditors and ask for amending the provision?

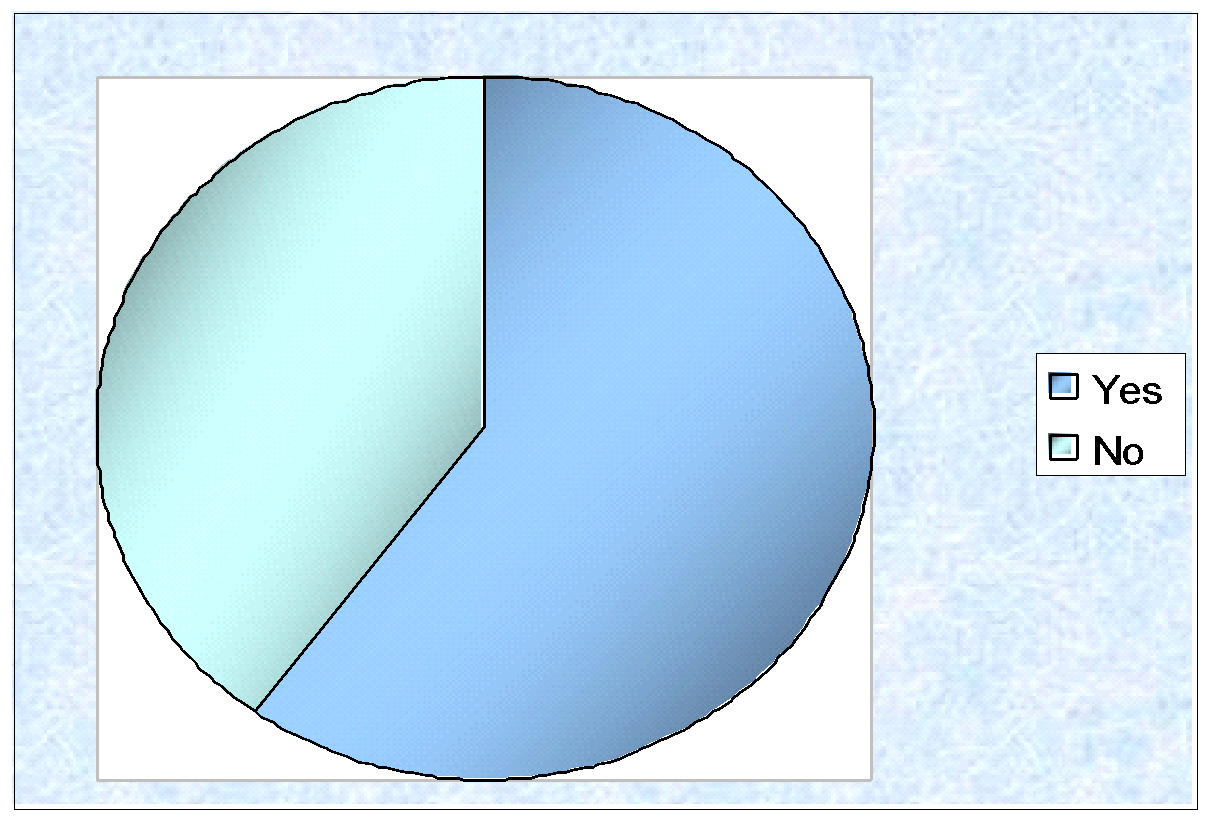

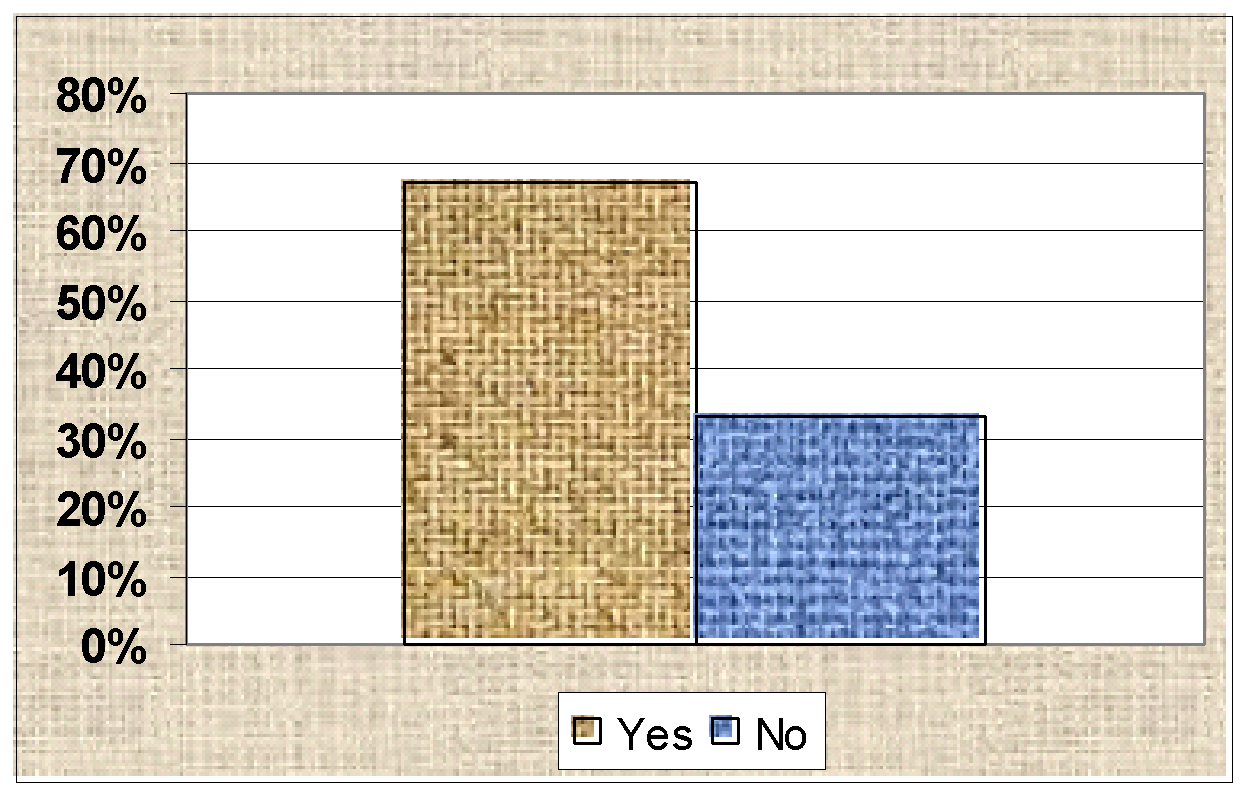

More than 67% respondents stated that few provision of Chapter 6 of Companies Act 2008 should require amendment. On the other hand, 33% respondents disagreed with the statement because they have enough confidence on the new law in terms of security of the creditors.

Question 11

Do you think that the privileges for debtors under business rescue would be fair?

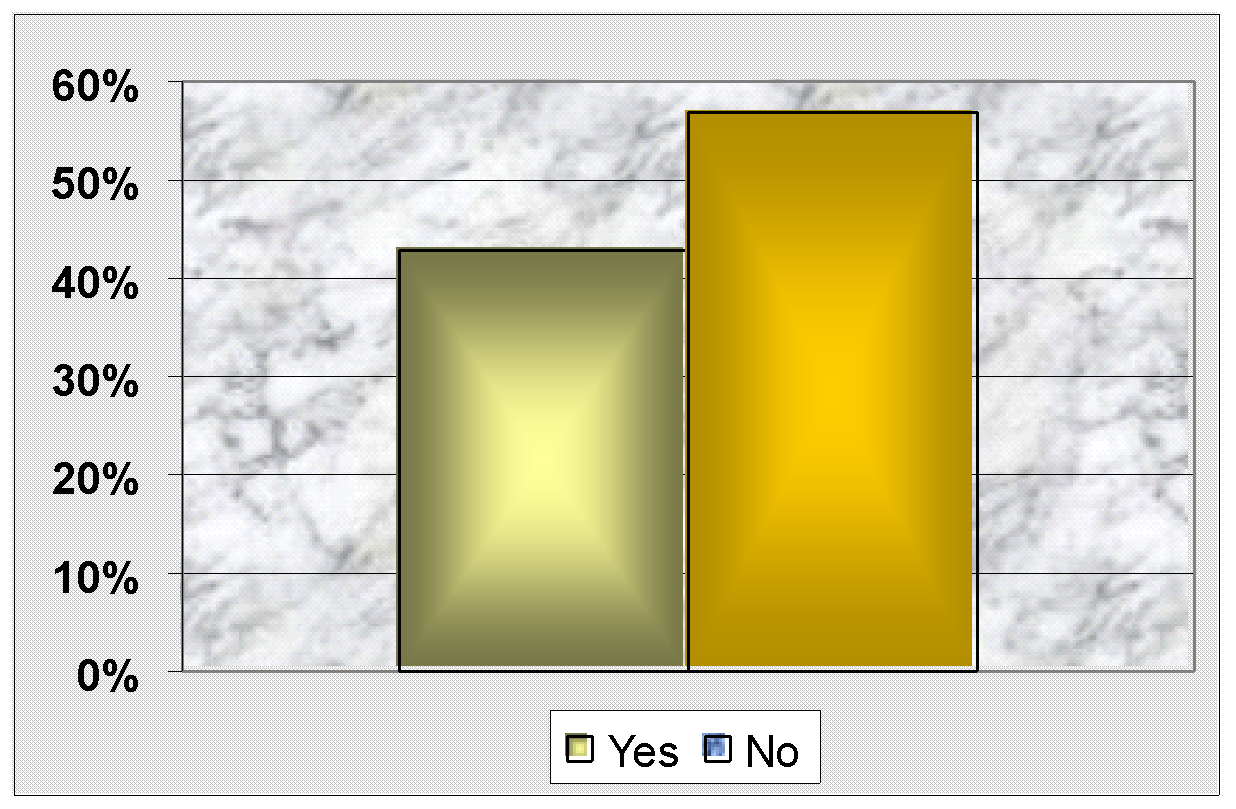

Most of the respondents clearly understood the statement and gave their opinion; however, only 43% respondents have agreed and 57% respondents were disagreed with this statement. Some scholars also mentioned that if the regulation concentrates more on the debtors, then the creditors undergo with financial risk though the business profit depends on the performance of the debtors.

Question 12

Do you think that the requirement to take the opportunity business rescue is hazardous and needed to amend?

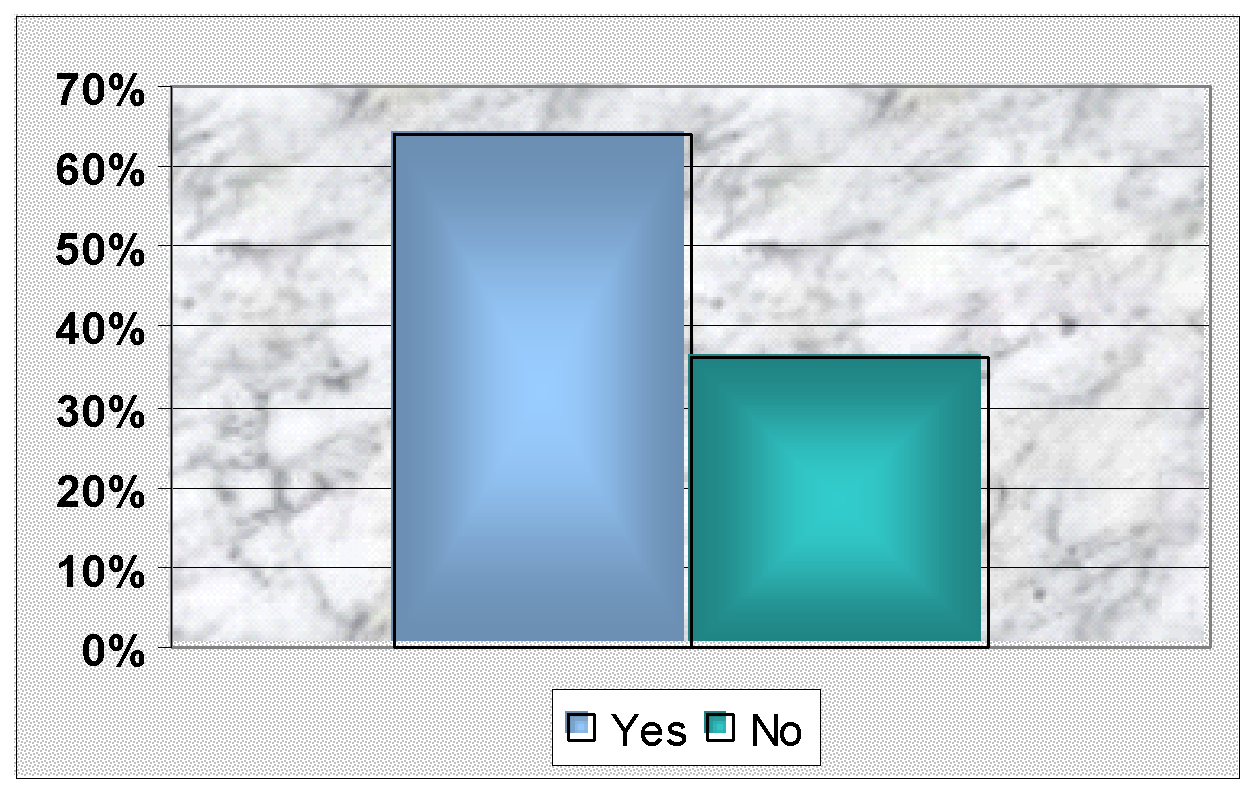

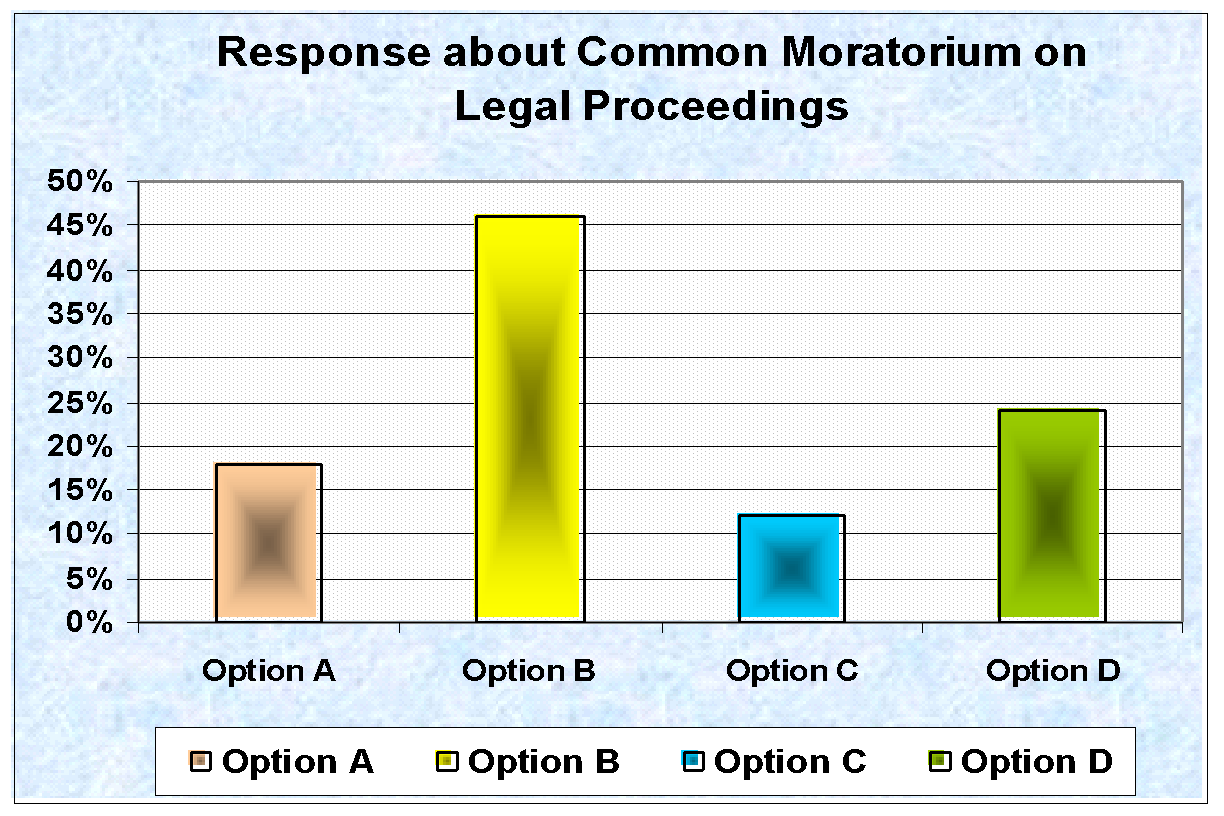

About 64% of the respondents had selected yes option and 36% respondents had strongly disagreed with the statement and selected no option. Most of the Scholars argued that new system must reduce liquidity rate, and help distressed companies from unusual position in this global financial crisis.

Question 13

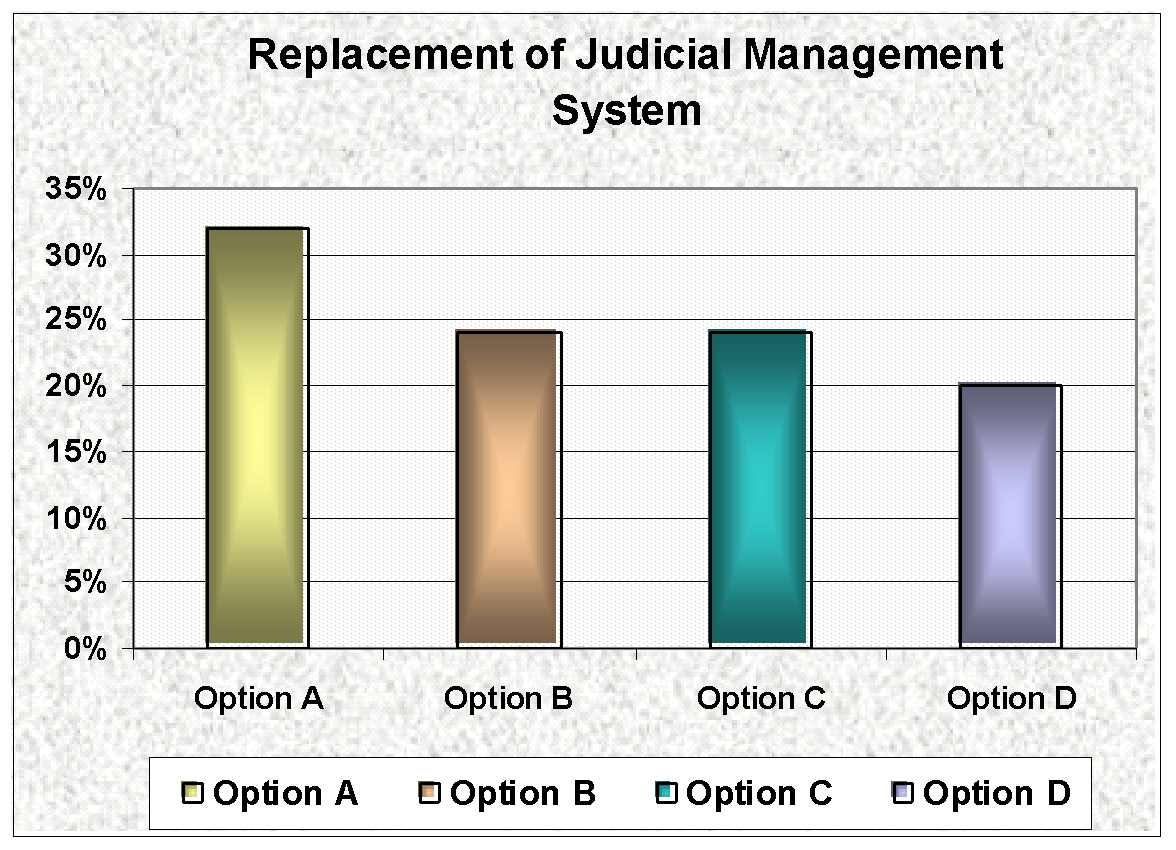

Would decreasing the involvement of judicial management under Business rescue will reduce complicacy of the process?

More than 65% of total interviewees had agreed with the statement because Companies Act No.71 of 2008 replaces the judicial management; as a result, it must help reducing complicacy of the process. On the other hand, 35% of the total interviewees disagreed with the statement because the process is still complicated to them.

Question 14

Do you think that the procedure mentioned to apply business rescue under Companies Act No.71 of 2008 is okay to address all stakeholder?

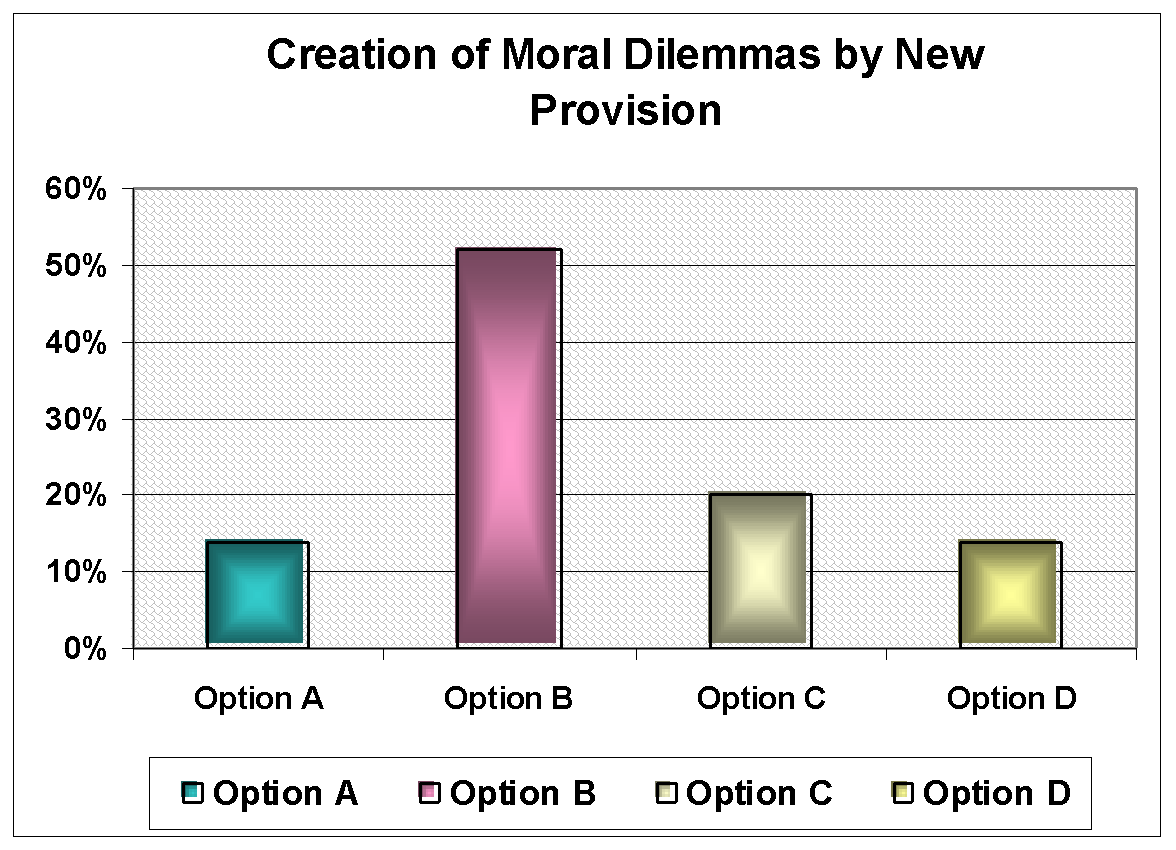

It is an important question to know about the provision of Chapter 6 for the stakeholders; however, 48% respondents were agreed, and 52% respondents were selected no option because new law was not addressing all stakeholders.

Question 15

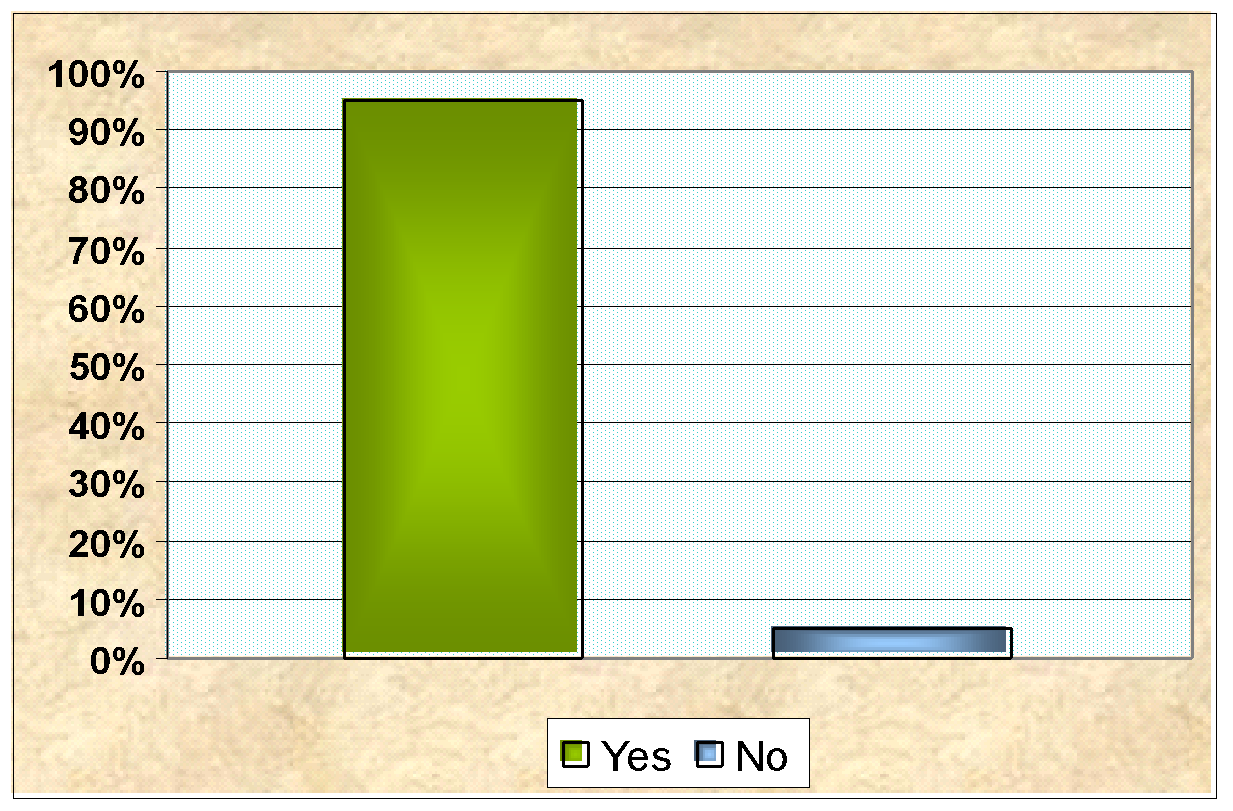

Does business rescue affect employees and contracts?

A substantial number of the respondents (95%) selected yes option because employees would become a “super-priority” creditor while it is labour-focused piece of legislation.

Section C

Question 16

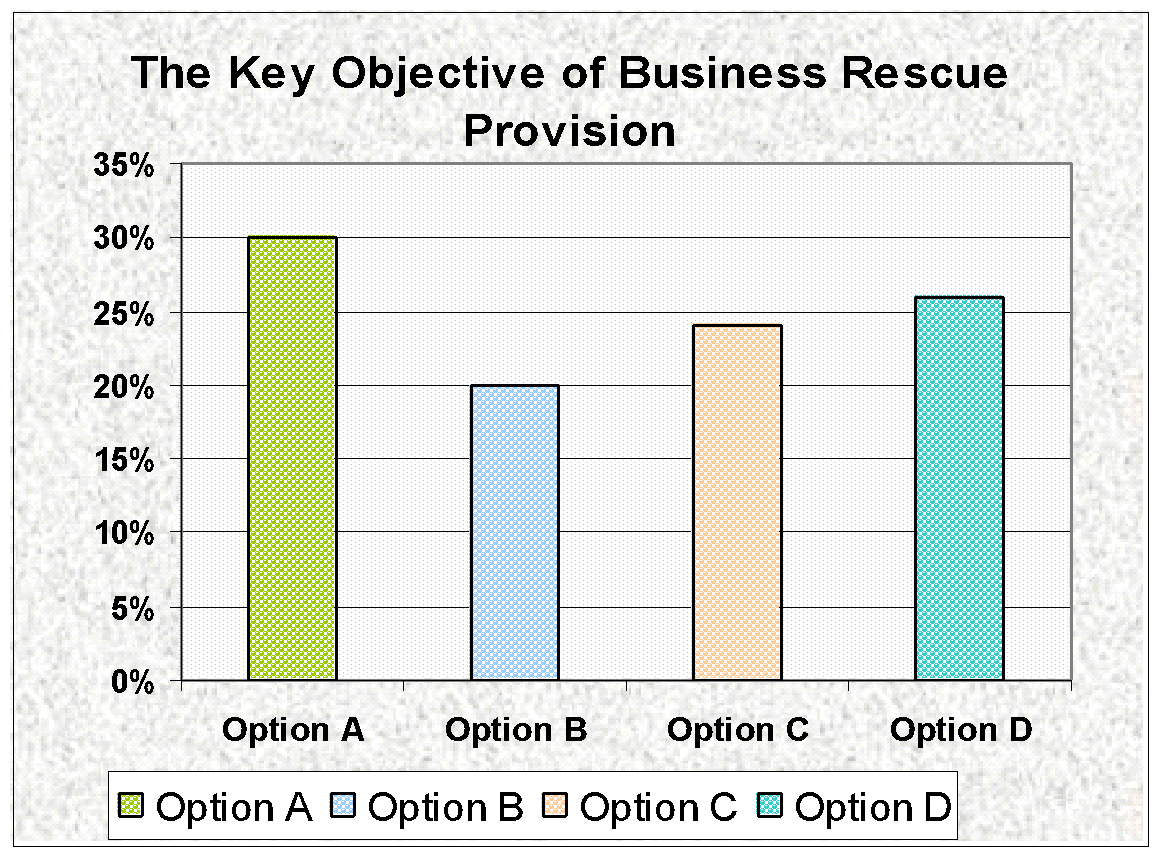

What is the key objective of Business rescue in South Africa?

According to the feedback from the respondents, the key objective of Business rescue in South Africa is to prevent a business entry from liquidation, as about 15 respondents were selected first option. However, 10 respondents argued that to facilitate a business entry for another fresh imitative, 12 respondents stated that to prevent creditors and move burden on them and 13 respondents pointed out that to spoil the creditor-friendly insolvency with western idea are the key issue of Business rescue.

Question 17

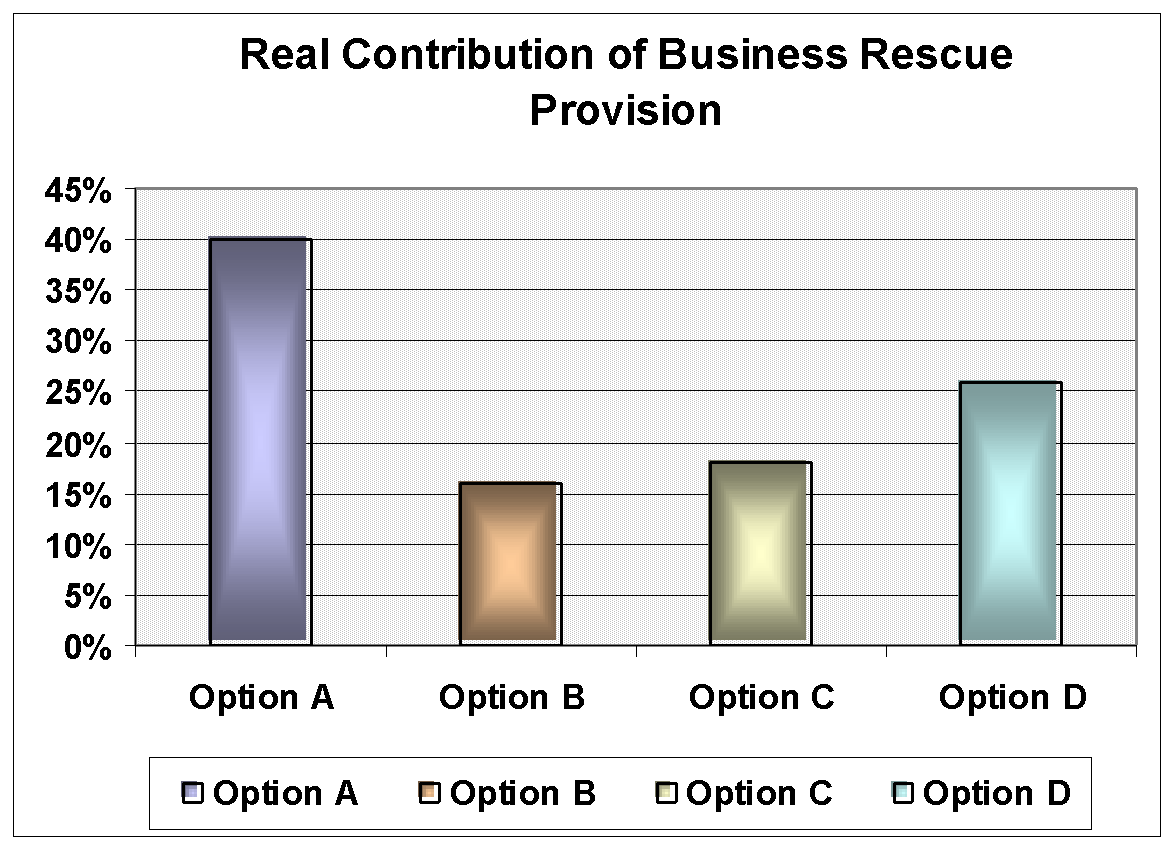

How does business rescue provision would contribute to real rescue?