Introduction

In the contemporary changing business environment, lenders face numerous ethical issues when dealing with different clients. The 2008 financial crisis started with unethical and poorly regulated subprime mortgages. Subprime loan is a “type of loan that is offered at a rate above prime to individuals who do not qualify for prime rate loans” (Gramlich, 2007, p.28). In other words, these loans are given to risky individuals with the term ‘risky’ here taken to mean persons whose capacity to repay the loan is not attested, and thus the interest rates a higher than the normal rates. This loan does not require the borrower to pay any down payment and even if such a requirement is in effect, the amounts needed are negligible. In addition, borrowers can secure another loan to pay the down payments needed. In such a scenario, the borrower does not need to have money or the capacity to repay the loan.

Conventionally, the concept of subprime loans was born out of the financial institutions’ ambitious plan to tap into the large pool of middle class citizens seeking to own homes and as Watkins (2011) notes, “the market presents opportunities for untold wealth” (p.365). Therefore, given the open opportunity to secure a mortgage, individuals thronged financial institutions, acquired loans and with the increasing demand for homes, a housing boom culminated, but how ethical are subprime loans? This paper answers this question by summarizing the concept of subprime loans and the risks associated with the loans to the lenders and borrowers, analyzing the role of leadership decision making in the subprime loan financial crisis, and evaluating subprime loans with the notion of social responsibility. The paper also compares and contrasts the resulting consequences for these actions and closes by highlighting the measures that have been taken since that time to ensure that it does not reoccur. The paper narrows on the events leading to the 2008 financial crisis as it is a perfect example of how subprime lending operates.

The concept of subprime loans and the risks they pose to the borrower and lender

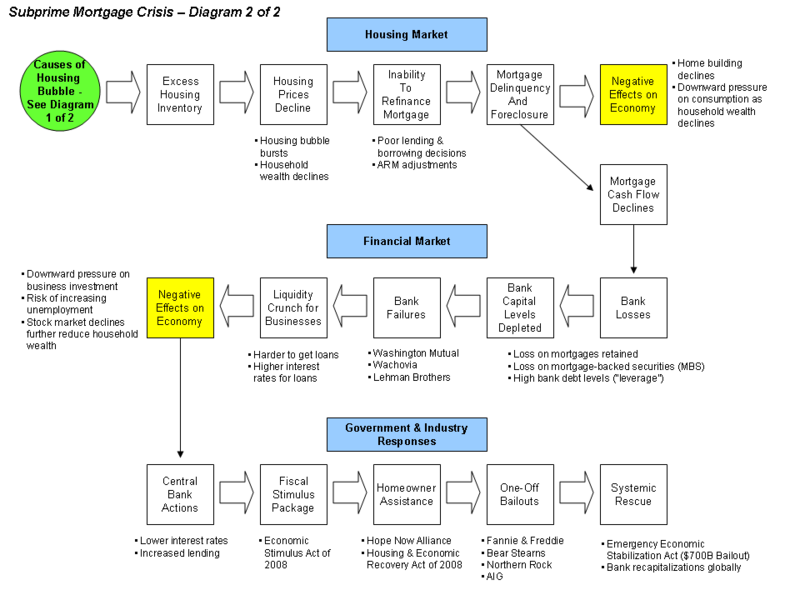

Conventionally, mortgage lending is categorized into subprime and prime based on the borrowers’ capacity to repay the loans. As aforementioned, subprime borrowers are risky as their capacity to repay is not guaranteed. Investment institutions borrow money from banks and they purchase numerous mortgages from lenders. In the 2008 financial crisis, investment institutions borrowed hugely from banks and they then mortgaged subprime borrowers. Later on, these risky borrowers defaulted and thus the investment companies could not repay the loans to the banks. Actually, the majority of these investment companies closed down and thus the banks could not recoup their monies. This move depleted the banks’ reserves as part of the circulating monies was held up in bad loans. In essence, banks could not function normally due to financial constraints. They could not even afford to offer new loans, which are needed to sustain consumer and investment expenditures. The following chart summarizes how a subprime mortgage crises arises:

The most outstanding risk of subprime lending to the lenders is the risk of defaulting. Given that subprime borrowers have very low capacity to repay the loans, the lenders face a real risk of loan default. This first risk heralds the second one which is loss making. Banks make huge profits from interests surcharged on subprime loans, but in the case of defaulting, the losses are equally huge. The ultimate risk from the combination of the two aforementioned risks is closure of business. Being faced with huge losses, the lenders in some cases are forced to close down as the losses become unmanageable. The other risk involves gaining a bad reputation and losing the trust of the clients. Clients would not want to associate with an organization at the brink of collapse especially if it is a company dealing with deposit taking. Customers want assurance of the safety of their savings, and thus bad reputation can kill any bank regardless of the efforts to save it from sinking.

On the borrowers’ side, the most outstanding risk is foreclosure. Failure to repay mortgages automatically leads to foreclosure. One can argue that if the loan is higher than the value of the property, an easy way out is to walk out of the property and let the lender foreclose. However, the borrower’s credit rating slumps and s/he may not access credit facilities elsewhere, which is a huge risk given the uncertainty of the future.

The role of leadership decision-making in the subprime loan financial crisis

Leadership decision making is a key element in the running of financial institutions. The 2008 financial crisis narrows down to intentional leadership decision-making gaps (Gilbert, 2011). The decisions made at one level have a domino effect at other levels in different organizations. For instance, the decision by bankers to violate the conventional rules of lending and include risky borrowers in their lending schemes was a clear indication of poor leadership decision making. Conventionally, borrowers should illustrate their ability to repay loans, but bankers somehow assumed that subprime borrowers would behave differently. Perhaps the decision makers were fooled by the ambiguous mortgage backed securities, which sought to protect lenders from defaulting subprime borrowers. However, this aspect is just an excuse, as decision makers in leadership should investigate such schemes carefully before embarking on any program. Thiel, Bagdasarov, Harkrider, Johnson, and Mumford (2012) note, “By all accounts, promoting ethical decision making at the leader level requires more than ethical guidelines and leaders of strong moral character” (p.52). Unfortunately, such leaders lacked as they engineered the 2008 financial crisis. For instance, the leadership at Fannie Mae acted irresponsibly and Stich (2010) laments, “The image of Fannie Mae as one of the lowest-risk and best in class institutions was a facade” (p.112). The leadership conspired to present wrongful auditing information for personal gains. It duped the public into believing that the company was doing outstandingly in the marketplace with inflated figures, and thus those who fell for the lies ended up losing their investments.

Sub prime loans in the eyes of social responsibility (comparing and contrasting the resulting consequences)

Every government has an obligation to better the lives of its citizens and thus achieve its social responsibility duties. The American government appreciated and embraced this role in 1938 when it created the Fannie Mae. This organization’s elementary duty was to assist low-income earners in owning homes. In addition, in the quest to protect the citizens, Fannie Mae was privatized in 1968 in order to allow independent budget accounting as required of every private organization. Afterwards in 1970, in another move to protect the citizens from the monopoly of Fannie Mae in the secondary mortgage market, the government created the Freddie Mae, thus checking the clients’ exploitation via the vagaries of monopoly. Therefore, by pushing for subprime lending mechanisms, the government executed its mandate towards the social wellbeing of the citizens. However, while on one side the government acted responsibly towards assisting the minority and low-income earners, the financial crisis left the same group in poor financial state with bad credit records after the foreclosures.

Measures taken since that time to assure this will not happen again

One of the key measures taken after the 2008 financial crisis is the passing of The Wall Street Reform and Consumer Protection Act in 2010. This legislation gives different stipulations, which keep lenders from engaging in practices that might lead to another financial crisis. Of the many stipulations in the act, the creation of “a financial stability oversight council to be on the lookout for risks to the financial system” (Poser & Fanto,2013, p.28) will help in noticing any signs of a crisis before it erupts hence ensuring that another 2007-2008 occurrence does not happen again.

Conclusion

The notion of subprime lending underscores the practice of lending to individuals with low capacity to repay their loans. Banks lend money to investment companies who then give mortgages to risky clients. Leadership decision making plays a key role in financial institutions, but key investment companies like Fannie Mae acted fraudulently and lied to the public for personal gains. Borrowers in subprime lending risk foreclosures while lenders risk making huge losses. Even though the government acted in the interest of the citizens by encouraging subprime lending, it ended up hurting the very individuals it sought to assist. However, the government has passed legislations to check the reoccurrence of a financial crisis in the future.

References

Gilbert, J. (2011). Moral duties in business and their societal impacts: the case of the subprime lending mess. Business & Society Review, 116(1), 87-107.

Gramlich, E. (2007). Subprime Mortgages: America’s latest boom and bust. Washington, D.C.: The urban Institute Press.

Posner, N., & Fanto, J. (2013). Broker-Dealer Law and Regulation (4th ed.). New York, NY: Wolters Kluwer Law & Business.

Stich, R. (2010). America’s Housing and Financial Frauds. Alamo, CA: Silverpeak Enterprises.

Thiel, C., Bagdasarov, Z., Harkrider, L., Johnson, J., & Mumford, M. (2012). Leader Ethical Decision-Making in Organizations: Strategies for Sensemaking. Journal Of Business Ethics, 107(1), 49-64.

Watkins, J. (2011). Banking Ethics and the Goldman Rule. Journal of Economic Issues, 45(2), 363-372.