Abstract

Internet banking offers a kind of self-service technology that is fast assuming an important full-fledged allotment medium for utilization of banking products and banking services, especially in developed countries. Since the internet was introduced to the bank industry in Saudi Arabia in the 1980’s banks in the kingdom have made up their minds to make the best use of it.

Seventy-three percent of banks in Saudi Arabia have web images, and at least twenty-five percent are fully engaging in the use of the services. The general increase in the usage of the internet recently has equally enhanced customers’ interest in e-Banking as a preferred banking channel; except for the interest of customers in an online bank, services are being hampered by customers’ fear of losing personal bio-data against their security and privacy.

The paper attempts to investigate the contempt of customers for internet-service quality in Saudi Arabia. Equally, attention is paid to studying factors that enhance customers’ acceptability of online bank services. Data was gathered primarily from a random sample of two hundred respondents using well-structured questionnaires which were served to Saudi-Arabian bank’s customers via electronic mails. Analysis by statistics and descriptive statistics were made use of in the explanation of respondents’ demographic profiles.

Factor/Regression analysis was also made use of in the determination of online banking acceptability. Findings identified factors such as security and privacy, innovation, a familiarity that are desired for the project. Findings from the study identified that irrespective of the fact of customers’ security/privacy concerns, bank customers in Saudi Arabia could adopt online banking dependent on whether banks would make available essential guidance.

Introduction

Background

Within the banking circle, developing information technologically presents several effects of flexibility on payment methods and as well makes banking services more user-friendly to bank clients or customers. Online banking has to do with the usage of the internet (or the web) by customers in accessing or carrying out bank transactions such as checking bank-account balances, paying bills, and topping up or carrying out inter-banks fund transfers (Conaway, 1994).

From a simple perception, online banking infers setting up a customer-based web page by a particular bank to make available the necessary information on products/services offered by the bank (Gulfer, 2010).

From an advanced point of view, online banking has to do with banks’ provision of facilities that would enable customers to access accounts, transfer funds, as well as buy financial products/services online (Judd, 2000). This could be achieved through facilities such as the Automated Teller Machine (ATM). Davis noted the introduction of online banking in Saudi Arabia as follow:

Saudi banks created online, real-time, 24X27 systems in the 1980s. Saudi Banks are working together on a shared e-system for B2B payments and authentication. Because they have already cooperated through SAMA (Saudi Arabian Monetary Agency) in developing shared payments systems (SARIE, ATM, POS) and have established processes for future cooperation (Davis, 1989).

The instance whereby banks make available customer-purposeful self-services is regarded as ‘transactional’ online banking (Ganesan and Vivekanandan, 2009). Even though there are enormous derivatives from online banking, banks must take into cognizance the several risks that go along with it. In Saudi Arabia, Huff notes:

“Although a regional leader, Internet banking in Saudi Arabia is yet to be fully utilized as a value-adding tool to improve customer relationships and achieve cost advantages” (Ganesan and Vivekanandan, 2009).

This view by Ganesan and Vivekanandan has also been shared by Lee and Turban (2002). A very vital procedure that banks in Saudi Arabia have to adhere to before carrying out any transformations has to be insured appropriate handling of online-banking risks (Msema, 2011). However, there are several complexities accrued to the determination of the most accepted approaches by both banks and customers on the usage of online banking.

Ostlund (1974) has identified distinct risks which are associated with the efforts of integrating fresh channels with the existent ones. Gerrard and Cunningham (2003) in their studies have identified customers’ security/privacy concerns as being instrumental to enlarging the risks. They noted:

“The Saudi Arabian bank customer is already indicating interest in e-banking; except, they are very concerned about security and privacy of internet banking” (Gerrard and Cunningham, 2003).

The Banking System and Need to enhance customers’ Trust in the System

The banking system can nearly not survive without trust; even though analyzing trust in terms of a phenomenon is near impossibility; especially as may be required by electronic-commerce- this is based on the fact that electronic-commerce is complex and risky. Trust then is considered to be a tool by which the success or the crash of online banking can be measured.

To better understand how to monitor the interest of the customer in online banking in Saudi Arabia, IDB (2002) considered instances from the United States where studies were conducted on ‘trust enhancers’. From the studies, it was found that the two basic items are relevant to the customer- which banks must always protect cautiously: these included privacy and security.

The Banking system and Element of Privacy of the Customer

The privacy of a customer to a bank could be said to be the individual’s fundamental right to provide personal information to a bank and control the level of exposure by which information is disseminated (Jun and Cai, 2001). In the banking world, concern about the privacy of the customer is no longer strange; even though banks may have a collection of information on their customers for a long. In any case, the issue of customer privacy has continued to stand out due to the emergence of fresh information-techs which usually are an improvement over previous ones. Pasmore (1988) noted from his studies that:

… The quality of the Internet connection, the awareness of online banking and its benefits, the social influence, and computer self-efficacy have significant effects on the perceived usefulness (PU) and perceived ease of use (PEOU) of online banking acceptance. Education, trust, and resistance to change also have a significant impact on the attitude towards the likelihood of adopting online banking [in Saudi Arabia] (Pasmore, 1988).

For this paper, a customer may be regarded as one who has an interest in the services of a bank using active patronage of such a bank, and who is bonded to the services of the bank by its terms and conditions; whose rights are respected and protected by the bank where patronage is carried out. The paper will be built around the definition to understand the level of acceptance of online banking in the Saudi-Arabian market where nearly seventy percent of the populace resides in rural areas and the remaining percentage resides in developed areas (Lewin, 1981).

The study assumes that customers are mature enough to be decisive and express their level of contentment regarding online banking services. The paper equally focuses on the realization of online facilitation factors to bank customers in Saudi Arabia despite the security/privacy concerns. Factors that would enhance or bring about an increment in customers’ willingness to adopt online banking in Saudi Arabia are therefore investigated. Deliberations on these issues provide answers to reflective questions which were served to customers in a plain survey randomly.

Aim of the Study

This study aims to evaluate customer contentment through internet-service quality in Saudi Arabia through administer of questionnaires to improve online banking service services which will bring about customer satisfaction in the kingdom.

Literature Review

The notion of Internet Banking and its Use

Internet-based applications have taken over a lot of activities in banking industries nearly worldwide, recently (White and Nteli, 2004). The result of this development is the creation of the provision of customer-self-service banking. In the view of Singh (2004) the newly emergent tech in the banking industry has brought about high competition in the sector. In any case, the new development of the banking system has necessitated the need for banks to improve on how they understand the needs of their customers.

Online banking has been viewed diversely. For example, online banking has been defined as follow:

Online banking is the delivery of banks’ information and services by banks to customers via different delivery platforms that can be used with different terminal devices such as a personal computer and a mobile phone with browser or desktop software, telephone or digital television (Roboff and Charles, 1998).

In the view of Shapra (2001):

“Online banking is a construct that consists of several distribution channels” (Shapra, 2001).

Online banking is a term wthathasn been used interchangeably with electronic banking, internet banking, or e-banking. The rate at which online banking is growing worldwide has become a matter of interest to many. For example, in the year 2006, Pew-Internet and American-Life-Project noted from studies an overwhelming engagement of online banking in the US- that over sixty-three million persons banked online during that year (Sohail and Shanmugham, 2004).

Online banking and traditional banking are very close in a diversity of ways such as in making payments, in making inquiries, in the procession of individuals’ information; it only differs in terms of the channel by which it is delivered. For a country or a sector of its banking system, deciding on adopting online banking is usually geared by several indicators. Saaty (1980) stressed:

“The success in online banking is achieved with tailored financial products and services that fulfill customer’ wants, preferences and quality expectations” (saaty, 1980).

Aladwani (2001) affirms customers’ satisfaction to be instrumental to success in providing online banking; and that banks are required to utilize a variety of mediums in a bid to customize their deliveries for specified needs of customers. Essential drives for successes in online banking have been suggested from studies for creating better online banking perceptions of security in banking-security by customers to include user-friendliness and network speed (Aladwani, 2001).

Opportunities of online-banking Saudi Arabia

In Saudi Arabia, online banking is creating a lot of opportunities that would enable the customer to benefit maximally from the variety of bank services available in the kingdom. According to Alan:

“… Customers can interact with their banking accounts as well as make financial transactions from virtually anywhere without time restrictions” (Alan, 1997).

Indeed, Saudi Arabia is endeavoring to catch up with online banking- to provide facilities that are obtainable in the global banking community as has been identified by Armstrong and Philip:

“Customers are changing their existing pattern of use of traditional banking and switching over advanced self-service technology” (Armstrong and Philip, 2010).

Online banking must be effective to achieve its objective. Bandura (1977) in agreement with Armstrong and Philip further noted that:

“… The willingness to adopt online banking by customers in Saudi Arabia depends on the expectations of accuracy, security, network speed, user-friendliness, user involvement, and convenience” (Bandura, 1977).

Studies conducted in Turkey and the United Kingdom on customers’ contempt level in online banking equally reviewed that customers’ privacy led the chart among the expectations of things customers want to have for them to be more contempt in online banking services (Aljlfri, et.al., 2003). The Argument has been emphasized given online banking and customer satisfaction that security remains a singular issue for encouraging the customer to be more contempt-minded with online banking services in most countries (Albrecht, 1983).

Al-Harran (1993) studied the characteristics of online-banking users and noted a common assumption of demography that influences the acceptability of electronic self-servicing elements; which involves online banking. The studies reviewed youthful people to be more engaged in online banking than adults and the elderly.

The reason for this could depend on the fact that youths are more interactive with computer devices, tools are services; as such they are more confident about deliveries from electronic services than older people. If this argument is anything to go by, it will be reasonable to suggest that the basic requirement for urging bank customers to adapt to the usage of online bank services is reliant on enhancing the confidence of the customer toward the development.

According to Al-Harran:

“Youths actively seek out online banking tools, and they want to conduct all transactions through the same channel” (Al-Harran, 1993).

In any case, Albrecht (1983) carried out a related study and came to a different conclusion. Lee discovered that Customers-Relation-Management (CRM) is a particular factor of influence on the customer’s willingness to access online-banking self-services deliveries more than it could be noted of other factors on the subject. Alan opined therefore that:

“… Customers tend to use such tools based on attitudes, not demographics” (Alan Al-Alawi, A., 2004., 1997).

Related studies investigating exact implementations by CRM in the evaluation of criteria/problems which require tacking for success in the implementation of the CRM program for enhancing the adaptability of customers to online banking were carried out by Al-Alawi (2004).

Saudi Arabia, like the United State, faces gender crises regarding usage of online banking: in the United States, studies were conducted:

An empirical study by Pew Internet & American life project dated 2002 was concerned with the number of people banking online and their gender in addition to their age. The study found that men are somewhat more likely to bank online than women (Abdulwahed, et.al., 2006).

Equally, the study reviewed:

Younger and middle-aged internet users are the most likely group to turn to online banking. The highest category using online banking in the survey was people in the age of 30 to 49, the lowest category is above 65 and the rest of them are in between (Daniel, 1999).

The research was rather specified based on evaluation of adaptability to online banking in terms of age of the customer and also identified that confusing webpage as well as complexities in the steps for carrying out online banking disheartened customers’ adaptability to online banking (See Table 1). Resultantly, there was the recommendation for the development of three-dimensional easy-to-use web pages which had a voice-recognition facility and used video tech.

A Brief Comparison of Online Banking in Saudi Arabia with Other Online Banking Systems

In Malaysia, studies were conducted on preferences to online banking by Sohail and Daniel (1999); the numbers of respondents were limited to three hundred only from the studies, and it was realized:

“… Age and educational qualifications of electronic and conventional banking have no significant impact on online-banking adoption” (Berne, 1966).

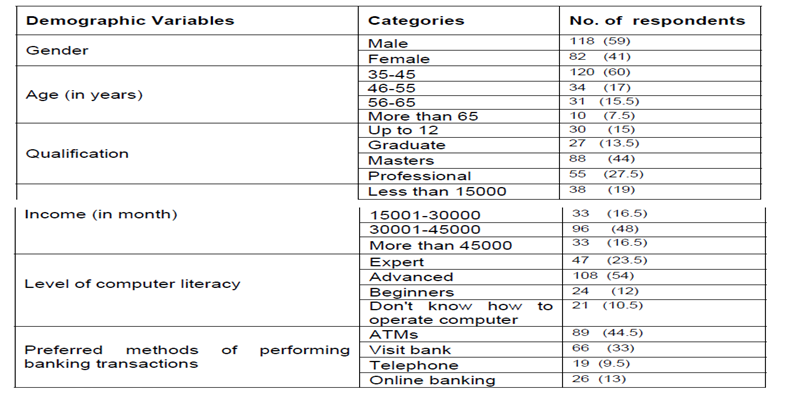

The descriptive statistics of the respondents present the demographic characteristics of the 200 respondents. It first shows that about 59% of the respondents are male and 41% of respondents are female. It shows that all respondents are adult, 60% of respondents were 35-45, 17% were 46-55, 31% were 56-65 and 7.5% were more than 65 in age (Berne, 1966).

Rather, Black et. al. (2001) Found:

“Accessibility to the Internet, awareness of online banking and customers’ resistance to change are the main factors influencing the adoption” (Black et. al., 2001).

Albrecht (1983) carried out a similar study that was based on four varying studies in a bid to identify recent and likely tendencies to the perception of online banking by customers in Saudi Arabia and came to the conclusion:

“… There are common perceptions regarding online banking with disregard to demographic, geographic or psycho- graphic characteristics” (Albrecht, 1983).

The study indicated majorly that non-adaptation to online banking by customers is primarily a function of security concerns as well as an inadequate understanding of online banking by users. Conclusively, online banking is not entirely a new concept to most countries and there is adequate research conducted on the acceptability of online banking services and the level of adaptation by customers. From research carried out on the subject, online banking has received the most attention in the following countries:

“Australia (Sathye, 1999), Malaysia (Mukti, 2000; Chung and Paynter, 2002; Sohail and Shanmugham 2004), Singapore (Gerrard and Cunningham, 2003a, 2006b), Turkey vs. the United Kingdom (Sayar and Wolfe, 2007) and, Saudi Arabia (Sohail and Shaikh, 2007)” (Howcroft, 2010).

In these countries, from the vast array of information on the acceptability of customers’ usage of online banking, it can be said that customers require that their confidence be made more solid in terms of protection of their security, and bank web pages have to be made more user-friendly to promote usage convenience, simplicity, and clarity by customers.

Service Quality

The outburst of new technologies in the banking world in recent years has brought about a variety of channels for carrying out banking services such as the usage of Automatic-Teller-Machines (ATMs), internet banking, and mobile banking. This development makes it possible for customers to carry out banking activities nearly without restriction to time and location. Conaway noted studies that:

“… These technological interfaces are known as self-service technologies [SSTs]” (Conaway, 1994).

The customer has more opportunities for banking with the availability of SST facilities in terms of saving costs, energy, and time. But the level of adaptation to the facility by customers varies or is a function of an individual’s perception or interest.

Bennis has confirmed that:

“… Although the kinds of service one can avail from these SSTs are similar, the patronage among the SSTs differs” (Bennis, 1969).

Equally, there is remarkable variation in the services offered by the various SST facilities and the level of acceptance by customers depending on the requirements for usage, benefits, perceived risk, service’ nature, or purpose.

In the US, the use of technology of banking services has proved to be effective especially as has been noted by Bennis:

The convergence of technologies has made the distribution of services more convenient than ever before. Automatic teller machines, bill payment kiosks, internet-based services and phone-based services (both voice and text), automated hotel check out, automated check-in for flights, automated food ordering systems in restaurants, vending machines, interactive voice response systems are examples of technology-based service delivery channels (Bennis, 1969).

These technologies are designed to be user-friendly or make the customer want to use them. Saudi Arabia, unlike the United States, has been on a journey to make online banking more than just an interact-with-the-bank by customers, but a lifestyle of the customer to satisfy their needs through online banking- such as paying for bills online and the rest. The Saudi Arabian bank system has so far made available online banking from retailing through ATMs and to some extent internet, and mobile phone devices.

Gewj identified some benefits of retailing through SSTs to include time-saving, cost-saving, and energy-saving. In Saudi Arabia, it is not the entirety of provided services through SSTs that are made use of by customers. This has made the level of acceptance of online banking by the customer further a bit slower than in countries where there are several incorporations in SSTs.

The essence of using SSTs is essentially sectional and dependent on customer services, transactions, as well as self-help. In the world of banking, services to customers are emphasized on obtaining information on account balances, obtaining statement-of-accounts, order for cookbooks, application for loan facilities, and so on. According to Blake and Mouton:

… Transaction involves making payments through SSTs like paying electricity bills, telephone bills, booking tickets for travel and entertainment, third-party transactions. Self-help includes knowing about the bank’s activities, location of branches, interest rates, procedures related to availing different services extended by banks, etc (Blake and Mouton, 1978).

Perceived risk (PR) has ordinarily been considered as a feeling of uncertainty that could erupt as a result of negative usage of products or services. Blake and Mouton (1978) identified PR be of two dimensions structurally; these include adversely consequent risks and light consequent.

Internet Banking in Saudi Arabia

Online banking in Saudi Arabia took off in the 1980s and has continued to grow steadily creating new opportunities for banks to serve customers better and at the same time bringing about stiffer competition among banks. Black et. al. (2001) noted recent developments regarding online or internet banking in Saudi Arabia as follows:

Saudi banks are working together on a shared e-system for b2b payments and authentication. Because they have already cooperated through SAMA (Saudi Arabian Monetary Agency) in developing shared payments systems (SARIE, ATM, POS) and have established processes for future cooperation (Black et. al., 2001).

SAMA has been on in Saudi Arabia for approximately twenty active years of intensive regulatory activities; during this period, it has laid the foundation for the contemporary system of payment which is setting new standards in the banking system of Saudi Arabia. During the year 1986, the agency brought into existence a system for automated clearing of cheques that made it easy and allowed an effective interbank-settlement and cheque-clear.

In any case, there are a lot of explanations for the non-flourishing of cheques as a channel for making payments and filling in the space; to overcome several emergent challenges, the banking stem adopted the usage of plastic cards in a rapid move. In recognition of the development, SAMA brought into existence the development of a national-ATM-transactions switch which brought about linkage to the entirety of ATMs in the country thereby enabling the customer to easily get their details of accounts at any available banking unit(s) located within Saudi Arabia. According to Black et. al:

“… This system, known as the Saudi-Payments-Network (SPAN), went live in 1990 and was enhanced to support point of sale transactions in 1993” (Black et. al., 2001).

The expansion of SPAN-system is rapid so that in the year 1998, there was an interconnection of about one thousand six hundred ATMs as well as sixteen thousand points of sale-terminals which brought about the provision of all available access to approximately three-million ATM-card owners who could access their services at any place in Saudi Arabia.

Equally, within the end of the 1980s, the agency brought into existence two fundamental initiatives which were very vital in furthering a fast growth in the procedure for making payments within banking systems from Saudi Arabia. The agency demanded the usage of swift-network regarding any transactions that had to do with international payments, and then in the year 1990, the agency developed the electronic-security-information-system (or the ESIS). According to Al-Alawi, ESIS may be said to be:

…an electronic floorless share trading and settlement system that is operated and supervised by SAMA. This system, which had almost entirely dematerialized share trading, achieves t + 1 settlement as standard and was soon to be moved to delivery vs. Payment (DvP). (Al-Alawi, 2004)

Even though these developments were in place, according to Burke:

“…interbank settlements until early 1997, continued to be affected by cheque clearing or account transfer at SAMA’s head office and branches” (Burke, 1982).

The development was attacked by whatsoever risk and inefficiencies that are known of with paper-based systems. Resultantly, a demand for an electronic-funds-transfer (EFT) system was necessitated to allow for payments/settlements which involved various banks in an automated system- the development assumed a very significant point of support to payments systems within the kingdom.

SAMA identified the necessity for the system to exist as a combination of the unction of both a-high-value and a-high-volume system of payment which had to be the pillar of strategically making payment in the future. Saudi Arabia protects online banking as has been noted by Burke:

In Saudi Arabia, all debit card transactions are routed through Saudi Payments Network (SPAN), the only electronic payment system in the Kingdom, and all banks are required by the Saudi Arabian Monetary Agency (SAMA) to issue cards fully compatible with the network. It connects all point of sale (POS) terminals throughout the country to a central payment switch which in turn re-routes the financial transactions to the card issuer, local bank, VISA, AMEX, or MasterCard. As well as its use for debit cards, the network is also used for ATM and credit card transactions (Burke, 1982).

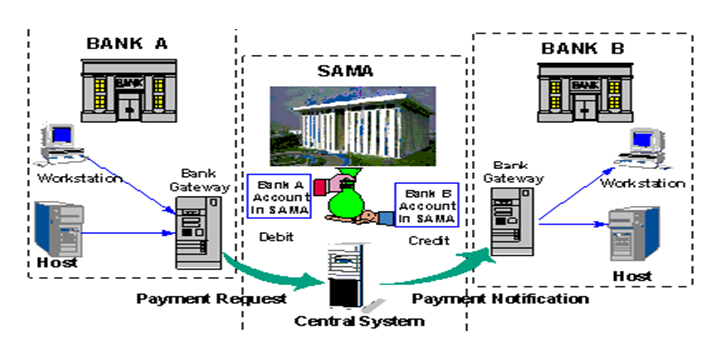

There are many real and possible merits of SARIE, but the most significant benefits to the banking system are found below:

- Banks are now able to carry out electronic financial transactions which include receiving and transferring funds safely and securely through their SAMA account;

- It is possible to pay utility bills from anywhere without the client having to visit his bank. A conclusion could be arrived at in such a way as to bring about automatic-financial-deductions which are derived from customer’s account in the settling of bills using the SARIE-MODEL;

- Funds could be sent across the various banks in Saudi-Arabia without difficulty in an automatic way since the numerous banks are interconnected through the SARIE-device; And

- The SARIE-tool enables banks to give out credit facilities against a client’s accounts and transfers the money to the beneficiary’s account at any bank in Saudi Arabia. A limit is set between the client and the bank which is paid on a timely basis. SARIE services are offered at different prices based on what is required. A SARIE payment flow is presented in figure 2 for further understanding of the discussion.

Oonline Customer Satisfaction

In the mid-1980s, commercial banks acted as share brokers while SAMA oversaw all share trading operations in pursuit of bringing about customer satisfaction in online banking. In the 1990s electronic-share-information-system (ESIS) was introduced and this greatly improved operations within the share market.

This led to the creation of a means for proper market update and information distribution. In 2001, the TADAWUL system was introduced to the share market to aid in market operations. This trading system provided immediate trading information as it occurred showing share trading settlement as well as transactions that took place daily. This enabled investors to invest from any place of their choosing as long as there is an internet connection. This technology also made the market more transparent.

Financial statements were submitted over the internet and made more accessible. In 1997 foreigners were welcomed and permitted to invest in the Saudi-Arabian share market through the Saudi Arabian-Investment-Fund (SAIF) which had been inaugurated in London earlier. Also in the year 1999, non-citizens gained the right to be involved in the Saudi-share market through the utilization of open-ended mutual-funds obtainable from Saudi banks.

In 2000, an investment law was passed enabling foreign organizations to carry out direct investments in parts of Saudi Arabia’s economy with/without the presence of local participation. Over the past twenty years, bank customers and their investment funds have grown exponentially with their subscribers also increasing at a yearly rate of 20 percent.

The government securities market is growing constantly and the materialization of corporate papers is also encouraging. There are no longer government restrictions on the amount of investment carried out online in Saudi Arabian bank customers.

Equally, there is a reflection of customers’ satisfaction in the stock market which has benefited from the computerization to enhance and simplify its operations, increased trading efficiency, and information distribution as well as enhanced supervision of trades. In the year 1989, the settlement system was put in place which resulted in existing growth that revolved around the requirements for business.

In the creation of the Electronic-Securities-Information-System, SAMA made use of a near-perfect stock exchange for numerous benefits it provides. It places all local securities transactions into one singular market. The system that controls this market provides real-time information on orders given, those executed and those are exempted from execution.

Technically speaking the ESIS information server was installed to enable better customer satisfaction in Saudi Arabia in the year 2004. This server provides real-time updates on market transactions for a huge number of clients throughout the kingdom. The ESIS information server is a platform providing multi-functionality in the stock market. SAMA also facilitated the workability of ESIS/WEB to bring about mutual-fund information distribution; it equally incorporates disseminating daily reports from SARIE/SPAN and remote-border-routing. According to Burke:

The server software was designed by Stratus and the ESIS web server is installed on Windows NT4.0 to host database Sybase version 11.0.3 on HP-UNIX C418 and ESIS web server database-Sybase 11.5.1 on Windows NT 4.0 as well as OS/2 Client database DB2 Version 1.2 (Burke, 1982).

This system receives banking transactions at the end of each day and starts the settlement process. This has to do with selling-back for the delivery of sold-shares on a preceding day. When the setting is done, a clearing report is brought Into effect systematically.

According to Burke:

“The system provides a good platform for monitoring the day to day activities of banks and how this grants satisfaction to the customer” (Burke, 1982).

Therefore, the ESIS can be described as a server/client application supporting different databases. To permit isolated branches to carry out new orders and make inquiries about particular emergent orders, and print reports, SAMA initiated the ESIS-Net platform. ESIS-Net is also called Order-Router-performs and is a Server to remote ESIS-Net branches.

This is an SNA-link running APPC LU6.2 applications. Interconnectivity between ESIS-Net and Saudi Arabian bank customers environments vary from bank to bank; some banks use IBM Communication Manager (CM2) with SDLC-card, LAN-card, or IBMX.25-card or Eicon-APPC-interface with Eicon-card. According to Beckett et.al:

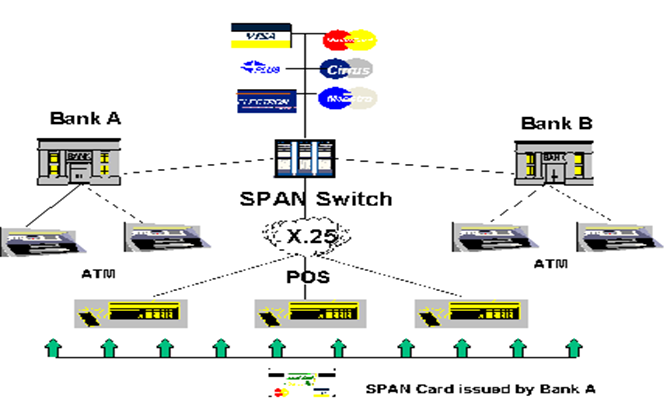

“The Saudi-payment-network (SPAN) is the general ATM and point of connectivity for all banks in Saudi Arabia creating a universal service point for the kingdom” (Beckett, et al. 2000).

The major reasons for creating SPAN have been very significant to the Saudi banking sector. To begin with, SPAN was designed intentionally to encourage Saudi citizens and foreigners residing in the kingdom to fully utilize the banking sector. This included electronic access to their funds in isolated areas thus dropping the banknotes on distribution. Also, the advent of electronic business has reduced the general demand for banknotes and increased the proper utilization of banking facilities.

SPAN has improved the effectiveness of the banking sector by preventing unproductive struggle at the business delivery points. From the period was launched till now, it has become more and more obvious that its primary purpose has been achieved. For example, there has been an annual increase in the total number of transactions, ATMs, SPAN cards, and Points-of-Sale terminals.

The consumer (or bank customers) population, consists of both citizens and residents who have over time had grown confidence in SPAN services. This confidence increases the tasks of the banking system to make available the maximum levels of support to the users of the complete SPAN network.

SPAN proffers additional banking services. These services include sustaining and maintenance of international business dealings, such as Visa/MasterCard, from either within or outside Saudi Arabia. SPAN has an unswerving relationship with these associations and provides that connectivity in a go-through mode to the Saudi-Banks. This international service includes both credit and debit card transactions at both ATM and Point-of-Sale terminals. Figure 3 illustrates the effectiveness of the service.

Again, the satisfaction of customers in Saudi Arabian banks is driven by SAMA which persuades banks to create Internet banking systems. Nonetheless, the dangers of such systems must be properly controlled and monitored. The responsibility of sustaining proper systems of control, together with those in respect of Internet banking, lies wholly with the institution itself. SAMA’s supervisory approach involves:

- Entertaining discussions with individual banks who wish to start internet banking to ascertain how the plan to check the security risks before the start rendering the service;

- Addition of definite Internet banking issues in SAMA’s usual off-site and on-site bank assessment processes; And

- Encouraging timely reviews of Internet banking facilities, processes, and processes

Therefore, banks preparing to offer online banking services should, as a minimum:

- “Ensure data available by outsiders is encrypted using industry-proven encryption techniques. Noting that widely-used may not be the same as highly secure. Minimum 128-bit keys should be used for SSL implementations;

- “Particular care is taken to ensure that the physical and electronic security of root keys and any certification authority systems are used;

- “Ensure adequate security measures are adopted to prevent hackers from accessing the bank’s mainframe;

- “Enact security policies and procedures to deal with the major areas of safety and security violations;

- “Monitor and report all security occurrences to SAMA regularly; and

- “Invite experts regularly to evaluate your security and send their assessment reports to SAMA” (Conaway, 1994).

- With the mentioned points on the ground, the banking sector in Saudi Arabia is good to go since there is an adequate regulatory platform to provide sound and secure services. The expertise and the customer market for internet-banking services will certainly mature further. Legal changes would also be considered to prevent issues of conflict in the future; for instance, signing of contracts on the internet through the use of digital signatures, access to customer information, and privacy. As service improves, transactions over the Internet will become more widespread thereby increasing the customer base of such institutions as well as the complete growth of the institution. Also at this stage, it is adequate to amplify the security services into a more meticulous guideline which all organizations offering Internet-banking services should follow. Banks are now able to carry out electronic financial transactions which include receiving and transferring funds safely and securely through their SAMA account;

- It is possible to pay utility bills from anywhere without the client having to visit his bank. An agreement can also be reached such that automatic financial deductions are made from the customer’s account to settle bills via SARIE;

- Funds can be transferred across any bank in Saudi Arabia easily and automatically since all the banks are interconnected via SARIE; And

- SARIE permits banks to issue credit facilities against a client’s accounts and transfer the money to the beneficiary’s account at any bank in Saudi Arabia. A limit is set between the client and the bank which is paid on a timely basis. SARIE services are offered at different prices based on what is required. A SARIE payment flow is presented in figure 2 for further understanding of the discussion.

Finally, effective internal auditing constitutes a necessary function that can help banks detect possible technological-related challenges. As Online-banking gets bigger, SAMA should endeavor to preserve the financial institutions informed of the best safety procedures which are put into use globally by giving out improved versions of safety documents as well as organizing workshops to assist in sustaining the security of online banking in Saudi Arabia.

Internet Banking Service Quality

Saudi Arabian Banks adopted e-banking services for two major reasons:

- “To face the challenges of financial requirements; and

- “To gain the benefits of online banking” (Conaway, 1994).

With approximately eighteen million Saudi-Arabians and a further seven million emigrants, banks in Saudi are getting wider. Financial institutions are channeling investments to alternative means of delivery. Internet access is also constantly increasing, generating a higher need for electronic banking. Electronic banking is easier, it makes fund transfer possible. Its usage is simple and it is easy to understand. For Saudi Arabian banks to fully satisfy their customers it became necessary for electronic banking to be adopted.

A vast number of Saudi-Arabian banks have turned in for the usage of electronic banking with the integrated approach whereby they maintain their brand name and proffer electronic-banking services as well as ATM and telephone-based options. These services are offered at cheap prices but are very effective. Electronic banking in Saudi Arabia has been effective with clients gradually switching to it daily.

Relationship between Service Quality and Customer Satisfaction

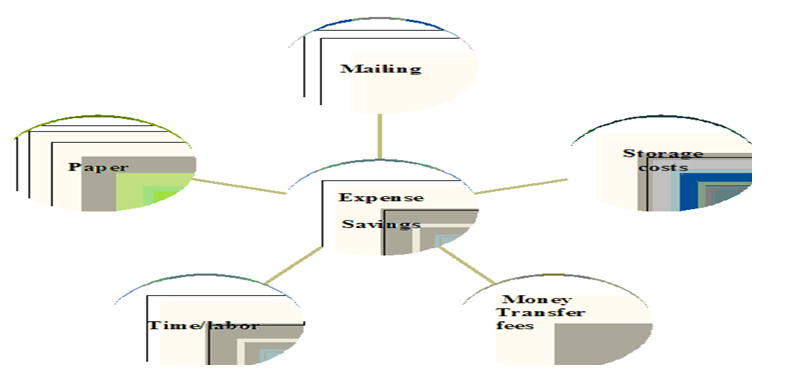

The internet is a global tool that offers banks an adequate distribution channel for already existing banking products and services. It also provides an efficient means of carrying out electronic banking transactions efficiently and at a cheap rate. For the clients, it enables him/her to carry out transactions anytime, at any place, and at any time. An enhanced services quality, therefore, is necessary for customer contempt. Figure 4 illustrates instruments that are capable of generating customer satisfaction from effective service quality.

Various strategies are formulated to retain the customer and the key of it is to increase the service quality level. Typically, customers perceive very little difference in the banking products offered by private banks dealing in services as any new offering is quickly matched by competitors (Chellappa and Pavlou, 2002).

TAM (Technological Acceptance Model) and Related Studies

The Technology-Acceptance-Model (TAM) is found to be very applicable to a diverse dimension in information technology and expresses cumulating traditions that are almost developed in any research. A lot of tam investigations are known to be empirical and make use of surveying approaches that are capable of generating appreciable successes (refer to appendix a). For this study, the technology acceptance model is considerably a matured model which is made valid in several contexts. However, like the model adopted by Shapra:

“It still needs to be empirically investigated for its invariance across different respondent subgroups to make sure that different sample profiles would not hurt the findings” (2001, p.47).

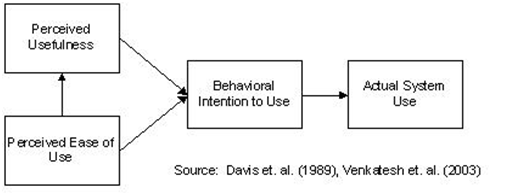

Role of TAM in Internet Banking Acceptance

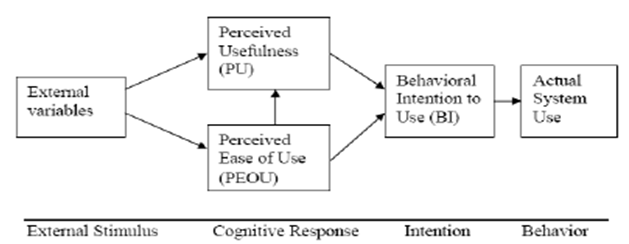

A particular model which has in the most been made use of in the study of information systems has been the tam. The TAM for the studies has been presented in figure 5 and expresses the determination of the exact behavior investigated under perceived-usefulness (PU) and under the perceived-ease-of-use (PEOU) which relates to customers’ attitude against online banking adaptability. According to Gerrard and Cunningham:

- “Perceived ease of use (PEOU), defined as ‘the degree to which a person believes that using a particular system would be free of an effort’

- “Perceived usefulness (PU), defined as ‘the degree to which a person believes that a particular system would enhance their performance” (Gerrard, and Cunningham, 2003).

According to the TAM these two beliefs are of primary significance for computer acceptance. PU refers to the prospective user’s subjective likelihood that the use of a certain application will increase his or her performance. PEOU is defined as the degree to which the prospective user expects the potential system to be free of effort (Davis et al., 1989).

The acceptability of the used system rests on the independence of its usage. For various samples, various tam-models are effective in usage.

Measuring Online Service Quality

Measuring online self-service quality is recently becoming very vital because affirms the delivery of expanded arrays of services about Websites. According to Conaway:

“Substantial research examines online services using salient scales primarily developed for personnel-orchestrated, face-to-face services; several recently developed scales that target online services focus on important information and/or system characteristics but do not consider retailers fundamental roles holistically” (Conaway, 1994).

This study makes use of past research works on the identification of customers’ level of satisfaction in online banking and utilizes several piloting and valedictory frameworks in using the e-SELFQUAL scale for the examination of the level of contempt of the customer as relating online services provided by Saudi banks.

Traditional Service Quality Dimensions

Several types of research have recently been concerned with assessing underlying electronic-service-quality dimensions on the subject matter of online customer satisfaction especially in Saudi Arabian banks rather than having a considerable examination of Internet-service-quality and the link of this to customer satisfaction and how it is capable of bringing about loyalty by the customer and addition of values. Studies have reviewed that:

Five dimensions, namely, efficiency, system availability, fulfillment, privacy, and responsiveness are significant determinants of loyalty to internet-banking users in Saudi Arabia. However, only three dimensions, namely, efficiency, fulfillment, and privacy are significant determinants of value to internet-banking users in Saudi Arabia (Cockburn and Wilson, 1996).

Traditional banking in Saudi Arabia is limited to the use of cheques and other manually used or paper banking devices which over the years have proved to fail in satisfying the customer in the slightest.

Online Service Quality Dimensions

Online banking in Saudi Arabia is limited in the full use of technology. However, the Saudi Arabian bank system has so far made available online banking from retailing through ATMs and to some extent internet, and mobile phone devices. Some benefits of retailing through SSTs include time-saving, cost-saving, and energy-saving.

In Saudi Arabia, it is not the entirety of provided services through SSTs that are made use of by customers. This has made the level of acceptance of online banking by the customer further a bit slower than in countries where there are several incorporations in SSTs.

The essence of using SSTs is essentially sectional and dependent on customer services, transactions, as well as self-help (muter et al., 2000). In the world of banking, services to customers are emphasized on obtaining information on account balances, obtaining statement-of-accounts, order for cookbooks, application for loan facilities, and so on.

Conceptual Framework of Service Quality Dimensions

From a conceptual point of view, the banking customer in Saudi Arabia needs to be educated further on the use of online banking services to bring about a better understanding of the application of the services offered by banks online in the kingdom. The extremely open, linked nature of electronic business calls for an augmented amount of confidence amongst clients, and financial institutions. Trust that a client’s private information will not be disclosed.

Trust that the information given to others in a system is accurate and of the uppermost truth. And the conviction of having a system that could be monitored continually daily, as it is needed in Internet-time. This is necessary for bringing about a means of putting up this trust is by educating the customers.

The Saudi Arabian bank system has so far made available online banking from retailing through ATMs and to some extent internet, and mobile phone devices. Gewj identified some benefits of retailing through SSTs to include time-saving, cost-saving, and energy saving. In Saudi Arabia, it is not the entirety of provided services through SSTs that are made use of by customers. This has made the level of acceptance of online banking by the customer further a bit slower than in countries where there are several incorporations in SSTs.

The essence of using SSTs is essentially sectional and dependent on customer services, transactions, as well as self-help. In the world of banking, services to customers are emphasized on obtaining information on account balances, obtaining statement-of-accounts, order for cookbooks, application for loan facilities, and so on. According to Blake and Mouton:

… Transaction involves making payments through SSTs like paying electricity bills, telephone bills, booking tickets for travel and entertainment, third-party transactions. Self-help includes knowing about the bank’s activities, location of branches, interest rates, procedures related to availing different services extended by banks, etc (Blake and Mouton, 1978).

Perceived risk (PR) has ordinarily been considered as a feeling of uncertainty that could erupt as a result of negative usage of products or services. Blake and Mouton (1978) identified PR be of two dimensions structurally; these include adversely consequent risks and light consequent.

There may also be the need to encapsulate the use of social networking in online banking to make it more interactive; a situation whereby customers will be free to interact with themselves in a forum and be able to suggest best banking practices that will be beneficial to them.

This application has proved effective in addressing possible influences and effects of internet-based social media and its potential or instrumental inductions to business promotions through a consideration of an incident involving a certain youthful musician, Dave Carroll, and airplane baggage handlers in July 1999 while he traveled in with his music-band in United Airlines; an incidence he later tacked up in Youtube which became light-stick for possibilities of a revolutionary tool for defining customer-management relations.

In this context, the Social-media is viewed as a designed media for the dissemination of communal interactions which is structured with the use of enhanced accessible/scalable publish techniques. Otherwise, social media is supporting the human necessity of social interactions, which is especially needed in the banking society through the use of the internet facility and other web-related technologies.

The Dave Carroll incident defines the effectiveness of social media through viral power which exposes possible expansions of internet-based networking. This demonstrates customer/company expanded-dialogue that permits direct company/stakeholder communications as a drift from what has been defined as:

“The traditional one-way output of corporate communications’ (Cleaver, 1999).

Customer-Relations Social media provides first-hand business-review options for accessing products or services. This is because the business administrators are aware of their needs; thus they have the opportunity of reestablishing with complainant customers in case a product does not satisfy the latter (Barry, 1998).

Fundamentally, social media creates connectivity micro-communities for persons with similar interests, whereby such individuals can interact or assist one another. Such communities can promote market growth in the following ways:

For one’s social media strategy to attain success, such as it was with Dave Carroll, it has been noted that the mere expression of words is inadequate (Burke, 1982). The reason for this incapacitation of words to effectively driving a market in a customer/management relationship has been attributed to the fact that clients on the internet are not there in the interest of searching companies’ websites but rather to acquire solutions in the fastest way to their questions (Bandura, 1977).

Perhaps, clients’ interests online are diverse; including seeking videos, articles, checking for mails, or sometimes merely engaging with forums. Thus, to make a piece of information on the internet attractive and beneficial to social media channels, the work must be properly structured to address the needs of the end-users.

In recent times, the entirety of online transactions has drifted and this has equally affected the attitude of clients. For one to effectively affect an internet community there is the need to drift with clients and meet their desires. There is rather the need to educate clients rather than persuade clients (Belanger, et al., 2002).

Problem Discussion

The need to instrument the confidence of customers in banks in Saudi Arabia is necessitated by a corresponding need to bring about faster, better, and more efficient banking services in the kingdom. Online banking is known to make available opportunities for banking with the availability of SST facilities in terms of saving costs, energy, and time.

However, in Saudi Arabia, the level of adaptation to the facility by customers varies as a function of individual customers’ perceptions or interests. Generally, there is distrust by customers in the ability of banks to secure the information or bio-data of customers in the online banking system.

Equally, there is remarkable variation in the services offered by the various SST facilities and the level of acceptance by customers depending on the requirements for usage, benefits, perceived risk, service’ nature, or purpose.

For the online technology to be fully accepted in Saudi Arabia, it must be designed to be user-friendly or make the customer want to use them. Saudi Arabia, however, is on a journey to making online banking more than just an interact-with-the-bank by customers, but a lifestyle of the customer to satisfy their need through online banking- such as paying for bills online and the rest.

The Saudi Arabian bank system has so far made available online banking from retailing through ATMs and to some extent internet, and mobile phone devices. Some benefits of retailing online in the kingdom include time-saving, cost-saving, and energy saving.

Aim and Objectives

The aim of implementing online banking in Saudi Arabia is to bring about an easy, faster, and cheaper means of banking; whereby banks can deliver efficient banking services to their customers in the best know comfort customers. The objectives for this have been stated in section 2.4 under online customer satisfaction

Methodology

Descriptive research

A questionnaire has been structured consisting of twenty research questions which are administered to two hundred respondents online through e-mails seeking to evaluate how much banking customers in Saudi Arabia have been satisfied with online banking practices in the kingdom. The questions follow the need to improve the services provided by banks in the kingdom regarding online services.

In the questionnaire, the research seeks to know the level of satisfaction customers have online and the possible challenges met by the customers. A related study was conducted by Blake and Mouton as noted:

“Respondents were asked if they were aware of online banking and whether they were willing to experience it had their banks provided sufficient support” (Blake and Mouton, 1978).

The surveying instrument which was made use of in the study is in a structure for emphi9rical studies. The study questionnaire is formed to meet up dimensions that measure the acceptability of online banking by customers in Saudi Arabia. Like it was the case with French and Bell (1978):

The variables were measured using multiple items. All of the scale items represented in the survey instrument utilize a five-point categorical rating scale. The anchors used included:

- 1= strongly disagree,

- 2= disagree,

- 3= neither agree nor disagree,

- 4= agree,

- 5= strongly agree (French and Bell, 1978).

Research Approach

The research approach involves administering questionnaires to customers online in a bid to evaluate their level of satisfaction with online banking services in Saudi Arabia. This hopes to the analysis of the current use of information technologies and online banking services in Saudi Arabia. In addition, interviews were conducted online with customers to further ascertain the authenticity of the findings.

Questionnaire Preparation

A questionnaire was prepared and administered to the customers online to access the level of satisfaction that the Saudi Arabian banking customer has in online banking as delivered within the Saudi-Arabian banking system. The questionnaire sort to know how individual customers personally feel about online services as offered within the banking system. Appendix B presents the questionnaire.

Data Collection

Data was gathered through administered questionnaires online. The Saudi Arabian bank system has so far made available online banking from retailing through ATMs and to some extent internet, and mobile phone devices. Bandura (1977) identified some benefits of retailing through SSTs to include time-saving, cost-saving, and energy-saving.

In Saudi Arabia, it is not the entirety of provided services through SSTs that are made use of by customers. This has made the level of acceptance of online banking by the customer further a bit slower than in countries where there are several incorporations in SSTs.

The essence of using SSTs is essentially sectional and dependent on customer services, transactions, as well as self-help. In the world of banking, services to customers are emphasized on obtaining information on account balances, obtaining statement-of-accounts, order for cookbooks, application for loan facilities, and so on. According to Blake and Mouton:

… Transaction involves making payments through SSTs like paying electricity bills, telephone bills, booking tickets for travel and entertainment, third-party transactions. Self-help includes knowing about the bank’s activities, location of branches, interest rates, procedures related to availing different services extended by banks, etc (Blake and Mouton, 1978).

Perceived risk (PR) has ordinarily been considered as a feeling of uncertainty that could erupt as a result of negative usage of products or services. Blake and Mouton (1978) identified PR be of two dimensions structurally; these include adversely consequent risks and light consequent.

Findings and Analysis

Demographic Findings and Analysis

Banks in Saudi Arabia offering electronic banking services may face the following challenges:

- Recognizing and solving problems of customer concerns on online bank transactions;

- Building and maintaining the confidence of clients;

- Clients’ inexperience;

- Convincing customers to accept the impact of secure bank transactions;

- Handling the cost of online transactions.

Saudi Arabian banks can prevail over the above challenges by applying the following two strategies:

- “Disclosing risks to customers; and

- “Educating customers” (Bandura, 1977).

Banks should make accessible clear information to clients on the demerits and merits of using electronic banking; publish consumer privacy and protection policy, disagreement handling, reporting, and problem resolution procedures, etc. They should inform their customers that proper security measures have been set up to guarantee the safety of their funds. They also need to highlight the type of encryption and firewalls used to ensure safety.

Quantitative Data presentation

A very promising aspect of online banking in Saudi Arabia is the promise for applied banking in the local premises. Online banking enables transacting businesses using internet services of the internet tool. Chellappa and Pavlou say that:

“The advent of internet-based electronic finance offers considerable opportunities for banks to expand their client-base and rationalize their business” (Chellappa and Pavlou, 2002).

Black et. al.(2001) in intense study lamented the lagging behind Saudi Arabia in terms of the provision of online banking services to customers effectively (Daniel, 1999). In any case, the studies identified that the Saudi –kingdom is fertile land on which effective online banking and customer satisfaction can be achieved. the introduction of online banking in Saudi Arabian came as a result of decree number one hundred and sixty-three of march, third nineteen ninety eighty.

In the view of Aljlfri, Pons, and Collins (2003), this was necessitated for a substantial telecom infrastructure upgrade which the kingdom underwent around the time when online banking services were launched in the kingdom.

Clear merit that was foreseen of online banking in Saudi Arabia was its tendency to develop customers in terms of enhancing their ability to interact with the computer and computer devices more freely or easier-even though a number 0of Of bank customers in the kingdom own a computer, it has been recorded that a majority are not familiar with the operations. Bandura has identified a further advantage of online banking as provided by the banks in Saudi Arabia stating that:

“Many employees have access to a computer in the workplace and prefer to conduct business with banks during office hours from their offices” (Bandura, 1977)

Gulfer (2010), thus, an effective provided online bank service is certain to bring about high contempt.

Howcroft, Hamilton, and Heder (2002) presumed that the banking sector in Saudi Arabia is certain to take a lead in the provision of online services in Saudi Arabia within a few years. It was evaluated that approximately sixty percent of online banking in the kingdom of Saudi Arabia is focused on financial-sector services. This is similar to what is obtainable in the United Kingdom where there has been an expectation that the banking sector will expand tenfold of British electronic commerce in the next five years. Studies by Beckett et.al reviewed that:

“Around one-fifth of Finis and Swedish bank customers are online, while in the united states of America, online banking is growing at an annual rate of sixty percent” (Beckett, et al. 2000).

The number of customers patronizing online bank services in the United States was expected to amount to fifteen million by the year 2003 (Ganesan and Vivekanandan, 2009). The objectives of the establishment of online banking in Saudi Arabia have been noted by Pavlou, (2001) to offers online banking procedures. In his studies, Singh (2004) noted:

“Financial services with the use of the internet may be offered in an equivalent quantity with lower costs to more potential customers. There may be contacts from each corner of the world at any time of day or night. This means that banks may enlarge their market without opening new branches” (Singh, 2004).

In the United States, banks have been making effective use of internet services to provide a three-fold service to customers, including:

- Marketing of information;

- Delivery of banking products/services; and

- Improvement of customer-relationship (Sohail and Shanmugham, 2004).

These facilities have made payment-cost reduced to the least as regarding carrying out online transactions. In the United States, the cost for online transactions is averagely placed at sixteen cents, using mobile phones and when using personal computers to access bank-owned software, one could spend as much as twenty-six cents. According to Roboff and Charles:

“A telephone bank is 54 cents, a bank branch $1.27, an ATM 27 cents, and on the internet, it costs merely 13 cents”. (Roboff and Charles, 1998)

Studies have reviewed that due to this reduced price in accessing online banking in the United States, there was a massive increase in the rate at which customers began to access banks online in the US since the year 1995. Consequent to the development, Shapra (2001) has noted:

“Millions of commercial websites have emerged. 3,286 banks around the world have already established their websites. Some banks are there because their competitors have been” (Shapra, 2001).

Lee and Turban (2002) lamented the slowness in practicalizing online banking in Saudi Arabia.

Efficiency

Before a successful transaction online, there must be the existence of well-structured and acceptable laws/principles. These are necessary to influence issues that may ordinarily hamper smooth transactions. In developing economies, the need for appropriately structuring rules in favor of international practices has been domesticated by professional institutions whereby they endeavor to localize monitory laws. The idea of international-best-principles can then be seen as a present-day global agreement amongst different legislative bodies.

Reliability

It is rare for an International business to survive in this twenty-first century without the assistance of independent investors- who cut across different countries and firms. In most cases, the support comes through the venture capital market. Venture-capital businesses make available finances to host nations in an area like technological designs, financial projects, and legal matters which bring about ample chances to save the rights of financiers and help government agencies to be strengthened (Jun and Cai, 2001).

Businesses achieve more international recognition and expertise which can easily conquer any setbacks that may be experienced. Venture capital in an international business has to do with investment organizations coming together financially to protect the interest of a company (Judd, 2000).

Responsiveness

The practice is been carried out by financially expert organizations with the sole responsibility of collecting funds from various sources and looking out for different firms worldwide that are in dire need of capital to advance their newly established business. After their financial commitment to all these companies, venture-capitalist in returns get an equitable share from such firms and enjoy more dividends if the firms do better in the business environment.

Every business has its gray-sides, the same happens to venture-capital business which sometimes provides data that may not be satisfactory especially on the fresh establishment (Howcroft, Hamilton and Heder, 2002). Studies have reviewed that Venture-capital is the best place to access funds for establishing firms (Msema, 2011).

Fulfillment

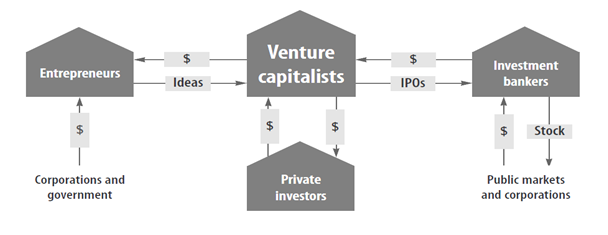

Ostlund (1974) argues that based on the high rise in the internationalization of business, a lot of the freshly established firms which lack the know-how that investors want may enjoy the open hands of venture-capital firms Which’s assistance provides unquantifiable benefit to all investors worldwide. Figure 6 is an Illustration of the interconnectivity between venture-capitalist and interacting bodies.

Banks are sometimes not that readily positioned to assist fresh establishments; not because the funds are not available but for information lop-sidedness and overhead cost. Venture-capitalist is stronger in this type of business by engaging in effective monitoring and personal contracting. This and more have made the VC get more patronage.

The venture capital business has four main players: entrepreneurs who need funding; investors Who want high returns; investment bankers who need companies to sell; and the venture capitalists Who make money for themselves by making a market for the other three (Alan 34).

In the United State, venture capital is appreciated as an economic hub that embraces different industries. Venture finance is not a long period transaction but only cherished investment in an organization with a good balance sheet and well-positioned infrastructural capabilities are the bases for future acquisition to any public institution.

Venture-capitalists acquire parts of any entrepreneur capital and build it within a specific period to grow and later dispose of it with the assistance of an investment banker. Usury laws allow a reduction in what banks charge on interest-based on the money borrowed funds and any danger that may be witnessed comes into play.

Even though personal equity and VC funds are fairly small worldwide, several nations still record high-growth-level in this business. Some years back personal equity funds move up to forty-five percent in India, while the China republic was three hundred and twenty-eight percent.

The facts behind this advancement in VC activities in China can be traced to result-oriented-formation and good host nation policies to defend funds. Any country with political stability will win the heart of venture capital organizations and a couple of others factors mentioned earlier which allow firmness in policy, there is a good location for the investor without any iota of doubt.

It should be known that investment from another country creates ample opportunities for the investors of such funds; these privileges can be in the form of a free-tax-holiday, fast approval of business documents, easy recognition, and patronage by policymakers to all the foreign investors. Again the host nation gains a lot in this kind of international investment environment which drives growth economically by creating jobs, improving on expertise, raising the proper standard of living for the citizenry.

Now it is known that every party involves in international business especially the host nation benefits immensely from such an opportunity. Host nations to this kind of direct investment need to develop articulate policies that can drive more investment which can boost the national economy in a positive direction. For some nations, caution needs to be taken in tax collections. This is a sensitive field that a professional needs to be consulted and possibly propose a total reduction in investment tax which can encourage the influx of foreign investors to the nation.

Privacy

Today’s awareness of the technology-based economy encourages banks to look out for substantial assets in getting loans which only a few have such assets to give as a standing order. Most of these banks and Equity-Company are guided by law to safeguard public investment and again such law allows an organization to get access to the public market. Venture-capital firms are headways in some nations especially in Saudi Arabia by funding different areas of innovation by adding their quotas to the economy to large VC firms in other parts of the world.

Analysis

Socio-technical systems (STSs) constitute tools that are made use of in helping IT-based management to succeed in resolving interdisciplinary IT-based-project confrontations. These confrontations may include situations where the manageability of resources in an IT-based organization may be technically, ethically, socially, politically, and culturally intertwined with the values of the organization.

The need to effectively utilize the fundamentals of STSs makes socio-technical analysis readily available as a facility for the integration of social values and ethics in the management of IT-based projects. In other words, the psychoanalysis of socio-technical systems enables a better comprehension of social impacts and aspects of ethics of IT-based projects; and basically, there is the enablement to diagnose and curtail appropriately anticipated probable challenges.

This study has been based on utilizing STS tools for enhancing the satisfaction of customers to online banking services in Saud Arabia through the following fundamental key points, among others:

- Appropriate knowledge of qualities that determine an effective IT-based project: The fundamental target here is an enhancement of the effectiveness of IT-based projects through the incorporation of its structural variables;

- An Articulate knowledge of the social system as it relates to IT-based projects, products/services, structure, as well as values;

- Interventional changes to the process, structures, behavior, and values of elements of IT-based project management.

Service Quality Dimensions and Their Relationship with Satisfaction

For online banking in Saudi Arabia to meet the goals which it is meant, the bank(s) where the same is conducted must be efficient as well as effective in terms of the managerial structure and services. Organizational effectiveness has been defined as:

“…a measure of the extent to which an organization realizes its goals” (Albrecht, 1983, p.4).

Similarly, Albrecht (1983) has considered organizational efficiency as follow:

“…the number of resources [that] an organization uses to produce a unit of output” (p. 4).

In Online banking, effectiveness and efficiency demand that dependence on an organization’s capability to restructure itself is a bid to meet up with environmental, technological, and (or) resource transformations which may sometimes really be swift. This, according to White and Nteli (2004) is achieved through four (4) fundamental processes, namely:

- Evaluation: this refers to the periodic and methodic procedure by which complete-functional inspection of an organization is realized;

- Adaptation: this may be considered to be the formal/disciplined process that facilitated policies and decision(s) which are realized through an articulated process of planning;

- Graduation: this entails identified organizational and systematic processes or tools by which the development of emergent leadership is achieved; and

- Innovation: this entails policies that facilitate better accomplishments in an organization by individual workers who are saddled with defined responsibilities.

In consideration of the extent and form of differences as well as the integration mechanisms for departmental coordination, studies have noted that an organization’s efficiency is enhanced in a situation whereby environmental complexities are aligned with structural complexities (Saaty, 1980).

Accelerated performances in online banking are through self-organized teams which have been assumed a very significant position as a component of designing in organizations for the maintenance of competitive edges. An impressive design for progressive teams was put together to enable the realization of STS (Pasmore, 1988). Pasmore defines the STS theory as follows:

“The theory of socio-technical systems (STS) is a process-based, team-oriented approach to work that evolved as a way to extend democratic and humane values into the workplace” (Pasmore, 1988).

Given the definition, The IT-based organization could be considered as been an open system that is positioned for the integration of two(2) independently connected systems; these include the technical subsystem and the social subsystem. The earlier goes in line with physics/chemistry/engineering rules and encompasses equipment and transformational processes that are technological and are driven by the economy; the choice for the most acceptable technique is reliant on which is least expensive and more result-oriented. Studies have reviewed that:

“The social subsystem, following the rules of psychology, sociology, and politics, incorporates interpersonal relationships that develop among people and build a mutual trust” (Pasmore, 1988).

Further studies have stressed:

“The system recognizes that commitment to work is conditional on the work experience and assumes technology can be adapted to fit people. The best match of solutions is explored through joint optimization and discovery” (Warren and Brandeis 1990).

Similarly, Msema (2011) has noted that STS also expresses the approach of the workers as the desire of a number of them which is based on gaining skills, control, or authority in the managerial train of a project. Designers of social techniques have made efforts in widening the knowledge of individuals to managerial issues as well as enable the latter to project the social/economical consequences accrued with management and then persuade the various workers to acquire more skills for better results.

The workgroup then assumes a center for change. Additionally, Msema (2011) had identified the need for STS-used organizations to structure tasks, authorities, as well as reporting-relationships in delegated groupings for ease implementation of decisions and assigning, training, inspecting, rewarding, or punishing of the groups as the need may be.

The need for this would be for enhancing the optimization of the technical/social subsystems in the general interest of a superior system. Management has the responsibility of ensuring the coordination of groups by requirements of work as well as those required by a task environment. The fundamental functions including monitoring of environmental factors then affect interior functions and coordination of the two(2) sub-systems.

There are several merits to this team-based design. Even though each organization is looked upon as being socio-technically a system, in the view of Lewin:

“…not every organization is designed according to its principles, methods, processes, and philosophies. The economic performances of companies based on an STS design have been significantly better than comparable organizations using conventional designs” (Lewin, 1981).

A fundamental design goal of STS is that of producing systems that would be able to adapt to changes and as well make the most out of a person’s ability to be creative. Returning to Socio-technical-values, principles, and objectives could be very helpful in simplifying an entire complexity with system productions as well as making available solutions to confronting issues that may occur presently; these may include challenges like corporate-values reinforcement. This has been appropriately clarified by Pasmore as follow:

The problem of value arises only when men try to fit together with their need to be social animals with their need to be free men. There is no problem, and there are no values until men want to do both. The concepts of value are profound and difficult exactly because they do two things at once: they join into societies, and yet they preserve for their freedom that makes them single men. It is thus assumed that the parallelism between societal and individual goals leads to a parallelism between institutional and individual values (Pasmore, 1988).

Most of the time, in IT-based projects, valued demand is for significance and worthiness whereas acquiring skills and experiences are automatically the most desiring force in shaping the projects (See Appendix A). Values in the setting of an organization have to do with persons working in ties for actualizing the achievement of unified goals as well as enabling the creation of standards for conduct that keep business decisions on the go.

Organizations have to set up shared values-sets as well as beliefs that are aligned with social/technical project-management aspects to actualize the achievement of business organizational targets. The values make provisions for links that connect members of an organization, its structures, process, and system as made use in adopting managerial project methods (French & Bell, 1978).

Efficiency

The need to effectively utilize the fundamentals of STSs has been noted in this study as necessitating socio-technical analysis and has made readily available a facility for the integration of social values and ethics in online banking in Saudi Arabia.

Reliability

In generalized terms, the internet (the vehicle for carrying out online transactions in a bank) could be considered the most effective machinery for reaching out to customers and delivering banking services to them in a way that would bring about maximization of their satisfaction. Online services are delivered through websites that are digitalized-brochure-forms of bringing about the provision of promotional data, institutional information, financial reports, vacancies/recruitment forms, search-engine, and offering of measures by which customers can reach out to banks.

White and Nteli (2004) noted that:

As of the middle of 2000, there were 11 banks with 1201 branches operating across Saudi Arabia. Of these, eight banks (73%) had established their presence in the web sites and only two of them were offering internet banking services” (White and Nteli, 2004).

Discussions

Identified Dimensions of Internet Banking Service Quality and Their Influence on the Saudi Customer Satisfaction

Effective online banking in Saudi Arabia followed the launching of SARIE in May 1997 to effectively address real-time settlements (RTDS) with a revolutionary electronic banking and commercial sophistication. It involves the application of an automated clearing-house (each) which is a cheque-clearing electronic system that goes hand in hand with span and connects ATMs with POS terminals; it equally embeds electronic-securities-information-systems (ESIS) as well as trading/settlement systems. SAMA’s responsibility stretches across managing SARIE whereby it assumes complete responsibility for monitoring expectations. According to Roboff and Charles: