Abstract

Over the past three decades, cases of fraud and white-collar crimes have been increasing exponentially in the 21st century. Fraud and white-collar crime is a complex issue in society because its occurrence is dependent on many factors such as organizational structure, organization culture, and personality traits. One of the prevailing notions surrounding white-collar crime is that it is the direct result of the general environment that people find themselves in.

However, it is the assumption of this study that the environmental culture that a person is in merely acts as a “trigger” so to speak resulting in a relatively minor contribution towards an individual’s propensity towards criminal activity. Since not everyone can commit white-collar crimes, there is ample evidence to prove that a white-collar crime is connected to an individual with distinct set of personality traits that sets them apart from the rest of the population.

It is based on this that further studies are needed in order to examine what personality factors influence people to commit white-collar crimes and how they can be identified. As such, this study will utilize statistical analysis in order to investigate several members of various corporations around the world in order to determine what factors influence the manifestation of white-collar crime in the research subjects.

Introduction

Social scientists engaging in the study of human behaviour have failed to establish a stronger correlation between psychological features and individual behaviours that are likely to be employed effectively in analysing the fraudulent tendency of perpetrators in cases of white-collar crimes. Many people in the corporate world are known to be law-abiding, but researchers, both in the field of psychology and finance, ask themselves several questions regarding what went on in the early 1990s to 2000s. This is because fraud was the order of the day among senior managers and those charged with the role of policy formulation in big organizations (Hartog and Belschak 2012: 35).

This irrational enthusiasm was mainly attributed to greed and dishonesty; however, current studies suggest that the personality of an individual has an intrinsic connection to his or her corporate behaviour. In fact, people in the corporate world rarely resort to fraud and misappropriation of public funds to attain their selfish interests. Criminologists offer three explanations regarding the manifestation of fraudulent behaviour, one of them being a supply of motivated offenders.

One of the current theories behind why white-collar crimes take place is because suitable targets are available while others perspective focus on its manifestation once capable guardians are missing. The explanation is in line with the idea that white-collar crime is often committed by choice, in that available opportunities and motivation determines the type of crime that an individual is likely to commit.

The inherent problem though with this perspective is that people in various businesses are exposed to a variety of opportunities where they can commit white-collar crime; however, its manifestation is seen in only a small segment of the professional worker population. What this means is that opportunity is not necessarily the primary cause behind criminal behaviour; rather, there must be other factors that influence a person towards white-collar crime.

One of the primary assumptions behind what influences this form of criminal activity is that white-collar criminals feel that they have access to the means that would allow them to steal without being noticed. The rate of professional crime varies directly with the supply of illegal opportunities, as well as the supply of people and organizations vulnerable or motivated to utilize them, whereas the rate and occurrence of offense varies inversely with the strength and strictness of rule of enforcement.

In other words, white-collar crime is inherently limited based on the opportunities inherent in a particular organization and the type of people that most likely to commit it. Examples of this can be seen in a variety of financial institutions that are located on Wall Street wherein the combination of opportunity and the willingness of some individuals to commit white-collar crime in order to gain a substantial profit or for their own personal gain combine to create a situation that has a high potential for white-collar criminal activity (i.e. insider trading, Ponzi schemes, etc.). Based on this, it can be seen that the environment in which people find themselves is a contributing factor, however, it is still dependent on the willingness of the individual to commit the crime in the first place.

This particular assertion is support by various studies on white-collar offenses that show that actions by business professionals that are often in conflict with the social, moral, and officially permitted norms of behaviour, are often due to the general environment that they find themselves in. For instance, when going back to the example of Wall Street, studies such as those by Norton (2010) state that there is a general culture of “cockiness” and “risk taking” that is often an aspect of various financial institutions.

These pervasive behaviours within the sector result in the development of adverse behaviours when it comes to business dealings wherein the line between ethical and unethical actions is often blurred due to the desire to make more profit (Norton 2010: 19). Aside from this, there is also the inclination towards unethical activity due to irrational exuberance, which is defined as an individual’s propensity to model their actions on the behaviour of other individuals.

In the case of white-collar crime, unethical actions due to irrational exuberance are thus committed due to the thought that “everyone else is doing it” resulting in the popularization of unethical activities due to a prevailing thought that ethically questionable actions are the norm in the environment that an individual operates in (Messick 2009: 71). This assertion can be traced to the work of Gibbs, Cassidy & Rivers (2013) which delved into the various instances of financial fraud and unethical business dealings within various financial institutions in the U.S. wherein Gibbs et al. states that while it is the environment that helps to trigger the manifestation of unethical actions in the form of white-collar crime, there still needs to be an inherent tendency within the individual in question to actually perform it in the first place (Gibbs, Cassidy & Rivers 2013: 353).

What this means is that merely attributing the behaviour of white-collar criminals to the pervasiveness of unethical behaviour within a business environment is insufficient to create a proper correlation. This is especially true when taking into consideration the larger dynamics of the population of various financial sectors wherein unethical behaviour is the exception rather than the norm. It is based on this that it can be stated that there must be some underlying psychological behaviour that is manifested within such environments that causes people to turn towards white-collar criminal activity.

In support of the earlier assertion that it is the culture evident in an environment that helps to manifest criminal tendencies, various studies that apply theories of organizational culture hold that culture has a significant influence on human behaviour because it causes employees to commit white-collar crimes. The presence of “criminogenic” culture in an organization leads to the development of unethical behaviours among employees, which consequently leads to the emergence of white-collar crimes. This was noted earlier regarding the culture of “risk taking” that is seen in the case of Wall Street and, as such, helps to show that there is a definite link between the influences of organizational culture and the manifestation of criminal intent and its application in white-collar crime (Laffey 2004: 11).

However, it should be noted that the application of theories in describing the occurrence of white-collar crimes fails to explain how subordinates acquire cultural values from their superiors. In this view, social learning theory fills the gaps in elucidating how “criminogenic” culture makes employees commit white-collar crimes because it applies the principles of operant conditioning and association-reinforcement.

Subordinates acquire “criminogenic” values from their superiors because the “criminogenic” behaviours flow through the management system (Martin, Rao and Sloan 2009: 40). In other words, employees learn through observed behaviour resulting in the manifestation of adverse traits. It should be noted though that despite such actions, the prevalence of such behaviours is not as wide spread as initially believed. For example, the study of Wasieleski & Hayibor (2009) which delved into the current corporate culture of Wall Street explains that it is only a small percentage of the employee and managerial population that espouse such “criminogenic” tendencies with the vast majority simply doing their jobs.

Though the culture of risking taking and being profit oriented is prevalent, there is still the presence of sufficiently ethical behaviour to show that culture alone is not enough to actually cause a person to commit white-collar crime (Wasieleski & Hayibor 2009: 587). This shows that there is an inherent “limit” so to speak in the capacity for “criminogenic” culture to actually influence an individual towards committing white-collar crime. This particular limitation is not entirely explained by social learning theory and is indicative of other factors that are involved that influence someone to commit white-collar crime (Birtch & Chiang 2014: 286).

The differential social association theory is one of the theories that view white-collar crime as an organized form of crime due to social organization. Three concepts of the differential association theory, namely, differential group association, normative conflict, and differential association in contextualizing white-collar crimes in the society are often applied. The concept of differential social organization conceives that the occurrence of white-collar crimes is dependent on cultural values and vices, which oppose and support white-collar crimes respectively.

The trade-off between values and vices ultimately determines the prevalence of white-collar crimes in most organizations. Since society has the capacity to influence human culture and behaviour, the concept of normative conflict views society as a significant factor that contributes to the occurrence of white-collar crimes. Differential association is a third concept that focuses on the knowledge and skills that are necessary for one to conduct fraudulent activities. In applying the theory of differential association, gaps in the understanding of organizational culture exist, as theories do not account for the organizational variation in the occurrence of white-collar crimes (Perri 2011: 217).

In layman’s terms, when taking the various theories that have just been mentioned into consideration, the manifestation of white-collar crime is the result of the interaction between societal influences and the inherent values that influences a person’s behaviour and actions. This helps to explain why despite the inherent adverse societal influences found in the case of various Wall Street institutions; the manifestation of white-collar criminal activity is actually isolated to a small segment of the population. Simply put, if a person does not have the necessary personality traits to manifest criminal behaviour, external cultural influences have little in the way of sufficient impact on that individuals actions (Duffield & Grabosky 2001: 6).

Though, it should be noted that this particular perspective does not take into consideration the possible changes that long term exposure might have on an individual that is immersed in such a culture (Murphy & Dacin 2011: 613). With this in mind, it is important to understand these predilections and what they are in order to properly determine how likely a particular employee would commit an act of white-collar crime.

Based on this, it is critical for psychologists to revisit the ideas of economists, anthropologists, and sociologists to understand the issue of white-collar crime. Sociologists, as well as criminologists are of the view that fraudulent behaviour is a result of trust violation because individuals who are likely to commit white-collar crime are rarely suspected of being offenders (Henle 2005: 247). What this means is that individuals who are often perpetrators of white-collar crime often do not appear to be overtly capable of such actions based on their external behaviours. It is only when a combination of the culture of their environment, their inherent internal personality traits, the need arises and the opportunity presents itself that such aspects manifest into an act of white-collar crime (Basson 2000: 40).

In trying to understand fraud, a fraud triangle concept is often employed, something the detectives term as the means, motives, and opportunities that pave way for crime. The triangle has three major elements including the perceived incentives or motivation, the available opportunities, and the tendency to rationalize the fraudulent behaviour upon its occurrence. The fraud psychology of the perpetrator influences the three elements. Individual motivation and the pressure to be successful control human behaviour.

The individual would rarely sit back and see things unfold, but instead he or she will try the best to justify the behaviour. The personal behavioural calculus influences the assessment of opportunity. Therefore, fraud cannot be understood without seeking psychological explanations meaning the logical answers are not enough. Criminals engaging in white-collar theft need excuses just as other criminals. The triangle suggests that a need should first exist on the side of the offender. The criminal would then explore the existing opportunity to commit the act. However, fraud does not happen when opportunities are non-existent.

Finally, the white-collar criminal attempts to justify or rationalize the act. The individual tends to believe that people are getting rich and he or she is lagging back hence the only way of catching up very fast is through fraud (Johnson, Kuhn, Apostolou and Hassell 2013: 206). For some, they reason that their action is temporary because it amounts to borrowing and the money will be retuned at some point. Others are of the view that they deserve the benefits because of their contributions and once the opportunity presents, the company should afford it. Fraud is perceived as a victimless crime because it does not hurt anyone. Finally, this type of crime is never viewed as being serious because it only involves money and not the lives of other people.

These aspects can be explained through the psychological concept of self-attribution, which can be summed up as a means of attributing or explaining one’s own behaviour and its potential outcome through perception and evaluation. Such a method of examination proposes that the attribution an individual makes about a particular event or outcome is based on internal or external factors. In the case of internal factors, this is defined as the intrinsic personal factors that influence an individual’s behaviour such as their feelings, behavioural traits, cognitive abilities, etc. Thus, when an individual is attempting to determine what are the antecedents and resulting consequences of their behaviour, they conduct an examination of such traits either through external observations made by other people or through memory.

This is due to the fact that people in general do not have “access” so to speak to their internal states and, as such, need to infer such traits through observations or an examination of the context of the situations in which such behavioural traits arise. Ramamoorti (2008) explains that internal attribution focuses on the internal factors that influence external behaviour resulting in a particular outcome. For example, individuals with anger management issues usually have an outcome where they lash out and attempt to vent their anger through some physical or verbal means (i.e. punching something or shouting at a particular individual) (Ramamoorti 2008: 522).

While on the other end of the spectrum, people who have emotional traumas, autism and a variety of other traits that cause reserved behaviour usually have an outcome where they are socially reserved, quiet and rarely, if ever, act out. In the case of external attribution, instead of intrinsic factors being the case behind an individual’s behaviour, the origin is instead placed on extrinsic situational factors. For example, a particular person can be normally calm and collected at home, however, due to his/her stressful workplace environment he/she is normally angry, annoyed and regularly irritated at work with the outcome of external physical or psychological outbursts (Quinsey 2002: 1).

This is not to say that such an individual is like this intrinsically, rather, their workplace environment is what influences them to act in this particular fashion. Thus, when making an assessment regarding the behaviour and actions of either yourself or another individual, self-attribution focuses on the intrinsic and extrinsic factors that influence behaviours. It is through this means of evaluation that it can be seen that it is the interaction between intrinsic and extrinsic factors along with internal self-evaluation that results in white-collar crime.

Basically, people examine the merits of the crime based on their learned behaviour and traits and this manifests in the act of committing a crime. People simply do not commit white-collar crime at the spur of the moment; instead, it is a process that involves a considerable level of self-introspection, which showcases its connection to the necessary behavioural attributes that would need to be present in order for a person to commit an act of white-collar crime in the first place.

Some of the possible behavioural traits associated with white-collar crime are immorality, arrogance, deception, cleverness, creativity, and poor management. These are some of the behavioural elements that contribute to organizational culture that is tolerant of aberrant behaviours that promote white-collar crimes (Marshall, Baden and Guidi 2013: 559). As such, they will be observed from a more in-depth perspective in the analysis section of the study.

Study Approach

A cross-sectional research was conducted to study the personality attributes that influence people to commit white-collar crimes using social desirability scale, hedonism scale, narcissism scale, conscientiousness scale, and behavioural self-control scale. Since prior studies have used one scale in determining personality correlates of white-collar crimes, this study sought to fill the reliability and validity gap by using numerous scales in one questionnaire. In the cross-sectional study, it was discovered that high conscientiousness; high narcissism, low behavioural self-control, high hedonism, and low integrity are personality attributes that predispose people to commit white-collar crimes in most organizations (Stevens, Deuling, and Armenaki 2012: 105).

A white-collar crime is partly a personality issue in most organizations. Hence, personality traits are important in studying white-collar crimes. It is assumed that individuals with traits such as narcissism, egoism, anger, self-centeredness, hostility, disagreeableness, and considerable competitiveness are more likely to commit acts of white-collar crime than others. These individuals are this classified as “Psychopathic” in that they are likely to deceive, con, manipulate, and charm people in order to achieve their goals regardless of the adverse outcome this may have on the individuals they are interacting with. It is based on this that it can be assumed that psychopathic personality traits make a person more likely to commit white-collar crimes.

Objectives

The objective of this study is to explore the correlation between an individual’s psychological traits and their attitude towards committing fraudulent activities in a workplace. The research aims to determine if the presence of the dark triads (Machiavellianism, Narcissism and Psychopathy), high Risk Taking and low Self-Control, Diligence and Integrity are more evident in the higher age group and those with longer working experience.

Methodology

Introduction

This section deals primarily with the chosen research methods for the study as well as the method of data gathering that was implemented by the researcher.

Study Design

In this analysis, seven personality traits scales (Machiavellianism, Narcissism, Psychopathy, Diligence, Integrity, Risk Taking, Self-Control), Attitude to Fraudulent Activities and demographic questions (Gender, Age, Country, Work experience, Type of organisation and Occupation) will be incorporated into a single questionnaire form and distributed through the use of a web-service. To comply with proper research ethics, participants will remain anonymous resulting in no personal data like name, address, date of birth being requested.

Questionnaire Design

The questionnaire is based on the following research studies:

- Paulhus, D. L. (2013), Dark Triad of Personality (D3-Short). Measurement Instrument Database for the Social Science. Retrieved from www.midss.ie-.

- Lee, K. and Ashton, M. C. (2004) ‘Psychometric properties of the HEXACO Personality Inventory’ Multivariate Behavioral Research 39:329-358.

- Peterson, C., & Seligman, M. E. P. (2004) Character strengths and virtues: A handbook and classification. New York: Oxford University Press/Washington, DC: American Psychological Association.

- Jackson, D. N. (1994) Jackson Personality Inventory-Revised manual. Port Huron, MI: Sigma Assessment Systems. Self-Control-

- Gough, H. G. (1996) CPI Manual:Third Edition. Palo Alto, CA: Consulting Psychologists Press.

Population Set

About 200 – 250 participants, who are over 18 years of age with working experience, will be recruited from business organizations and professional organizations to answer the online questionnaire (Appendix 1). There is no direct contact with the participants.

Data Gathering

Participants will be informed about the research study thorough the Participant Information Sheet and will be requested to consent by agreeing to consent form before commencing with the survey and also to provide a unique number in case they would like to withdraw from the survey.

Data Analysis

Quantitative analysis of the data will be performed using the SPSS tool to produce the statistical calculations such as regression analysis and statistical tables. The data will be collected anonymously thorough a web-service and only the numerical responses will be provided as a file for analysis.

Results

Introduction

This section focuses primarily on the results of the study and presents the results in a table format. Explanations are given regarding statistics utilized and how they relate to the study as a whole.

Descriptive Statistics

Initially, a series of descriptive statistics were conducted on these data in order to better describe this sample of respondents and the dataset analysed. Sample sizes and percentages were reported for each category of response for the categorical variables included within this study, while measures of central tendency and variability were calculated and reported for the continuous measures of interest.

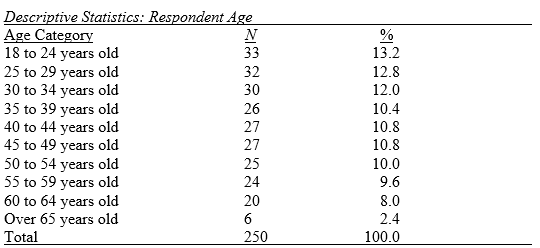

All 250 respondents agreed to the survey (100.0%), with this sample containing 123 male respondents (49.2%) and 127 females (50.8%). Table 1 summarizes respondents on the basis of age group. A fairly broad distribution was found on the basis of age, with a greater percentage of respondents being young adults, and the percentages decreasing fairly steadily as age category increased.

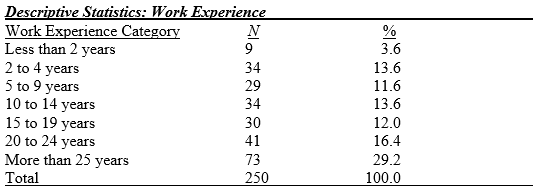

Table 2 summarizes responses obtained with respect to work experience. Over 29% of respondents had more than 25 years of work experience, with more than 16% having between 20 and 24 years of work experience. 13.6% of respondents each had between two and four years of experience and between 10 and 14 years of experience. 12% of the sample were found to have between 15 and 19 years of experience, with close to 12% having between five and nine years of experience. Finally, close to 4% of respondents had less than two years of experience

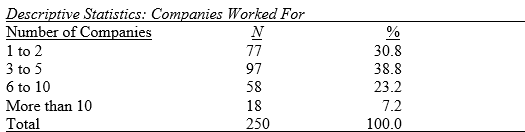

Respondents were then summarized in Table 3 on the basis of the number of companies they had worked for. Here, it was found that close to 39% of respondents had worked for between three and five companies, with close to 31% having worked for one or two companies in total. Additionally, slightly over 23% of respondents were found to have worked for between six and 10 companies in total, with slightly over 7% of respondents having worked for more than 10 companies.

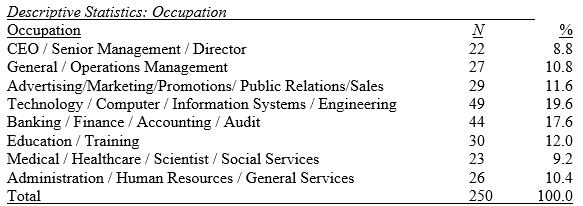

Broad ranges in occupations were found, as shown in the table 4. Most commonly, close to 20% of respondents worked in technology, computers, information systems, or engineering, with close to 18% of respondents working within banking, finance, accounting, or auditing. Least frequently, close to 9% of respondents found to be employed as a CEO, in senior management, or as a director.

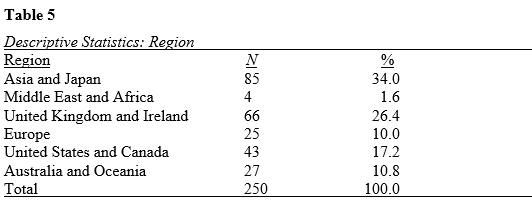

For region in Table 5, 34% of respondents were found to be based in Asia, including Japan, with slightly over 26% being based in the UK or Ireland. Following this, slightly over 17% of respondents were in either the US or Canada, with close to 11% being based in Australia or Oceania. Following this, 10% of respondents were found be based in Europe, with close to 2% being based in the Middle East or Africa.

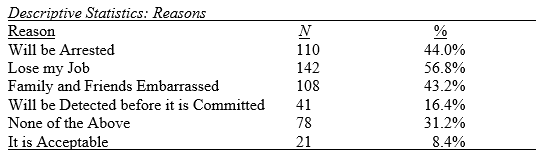

Table 6 summarizes the results obtained with respect to reasons for not committing crime. Most commonly, close to 57% of respondents stated that they could lose their job, while 44% were concerned over getting arrested. Slightly over 43% indicated that they do not commit crime as their family and friends will be embarrassed, with slightly over 16% being concerned that the crime would be detected before it was committed. Finally, slightly over 31% of respondents replied with “none of the above”, while slightly over 8% stated that they felt it was acceptable.

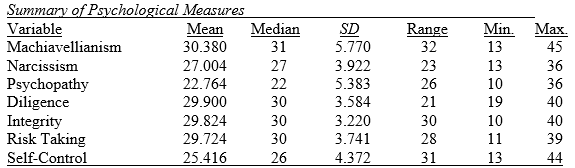

Table 7 summarizes the psychological measures included within this study. As shown, means as well as medians on the scales generally approximated 30, with standard deviations ranging from slightly above three to close to six. Overall, scores were found to range widely.

Research Question 1

The first research question explored within this study consisted of the following:

The fraud/white-collar criminal is most likely to be between the ages of 35-55, and have >10 years work experience; these experienced employees will have sufficient knowledge to circumvent the controls and would even break the law to attain higher achievements. Therefore, those aged <35 will show lower levels of Machiavellianism, Narcissism and Psychopathy compared to those aged 35-55, an indication that these traits are nurtured.

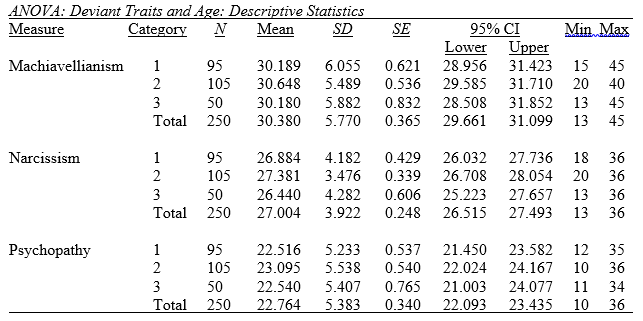

Initially, a one-way analysis of variance was conducted in order to determine whether there were any significant differences in Machiavellianism, Narcissism, and Psychopathy on the basis of these three age groups (less than 35, 35-55, and above 55). Table 8 summarizes a series of descriptive statistics conducted on these psychological outcomes based upon these three age groups. As shown, mean differences on the basis of age category were found to be small, with standard deviations found to be moderate in relation to these mean scores.

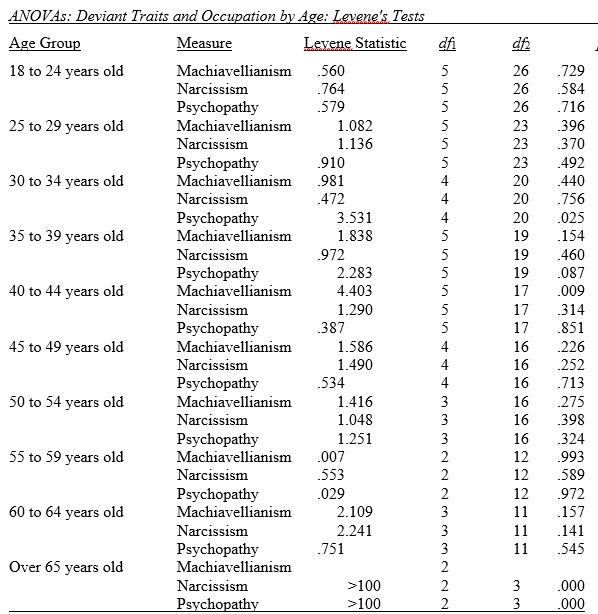

Levene tests were conducted on these data in order to determine whether the assumption of the homogeneity of variances was violated in these three analyses. Statistical significance was not found with regard to Machiavellianism, W(2, 247) =.255, p =.775, Narcissism, W(2, 247) = 1.962, p =.143, or Psychopathy, W(2, 247) =.043, p =.958, indicating that this assumption was not violated in any case.

With regard to the ANOVAs themselves, statistical significance was not indicated with respect to Machiavellianism, F(2, 247) =.194, p =.824, Narcissism, F(2, 247) = 1.046, p =.353, or Psychopathy, F(2, 247) =.341, p =.711, indicating that significant differences in these three psychological outcomes were not present on the basis of age category based on these analyses.

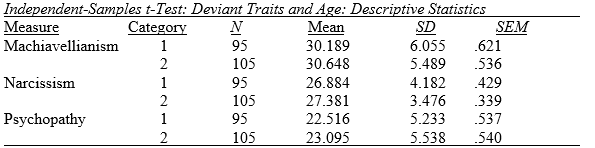

A series of three independent-samples t-tests were conducted focusing specifically on the comparison between individuals aged 35-55 and those younger than 35. Table 9 summarizes the descriptive statistics conducted associated with these t-tests. However, substantial mean differences in these psychological outcomes on the basis of age category were not found.

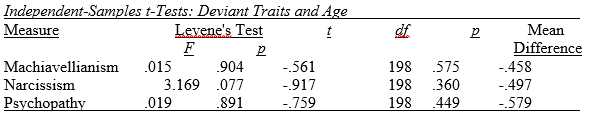

Table 10 summarizes the results of the independent-samples t-tests themselves. Levene’s test was not found to achieve statistical significance in any case, indicating that the assumption of the homogeneity of variances was not violated in any of these three tests. With regard to the t-tests, statistical significance was not found in any case, indicating that significant differences in these three psychological outcomes were not present on the basis of age category.

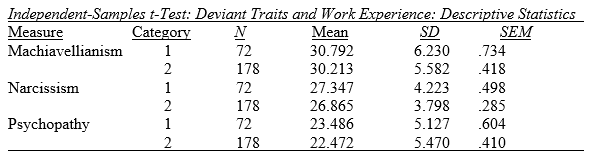

Further analyses were then conducted focusing upon work experience. Specifically, the focus of these analyses was on comparing individuals with more than 10 years of work experience with all other respondents. Table 11 summarizes the descriptive statistics conducted on these data. As shown, substantial mean differences in these outcomes on the basis of work experience was not found.

Table 12 summarizes the results of the independent-samples t-tests conducted on these data. Levene’s test was not found to achieve statistical significance in any case, indicating that the assumption of the homogeneity of variances was not violated any of these three tests. Additionally, the independent-samples t-tests themselves also failed to achieve statistical significance in any case, indicating that there were no significant differences in these three psychological outcomes on the basis of work experience.

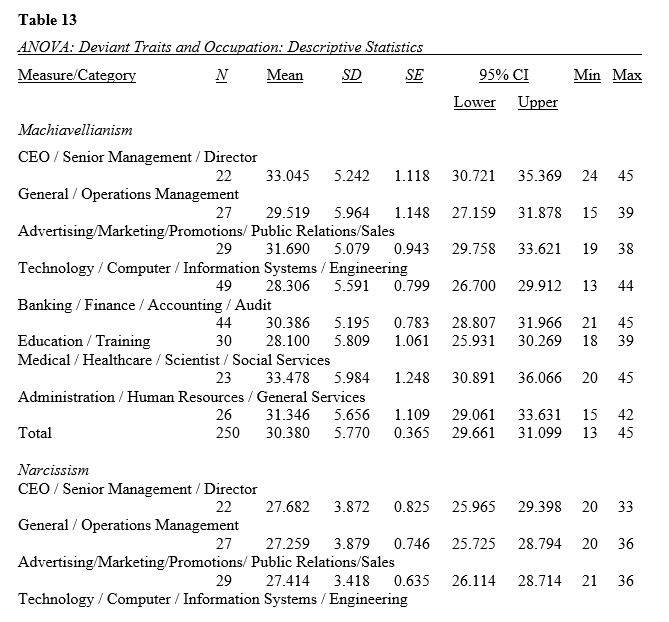

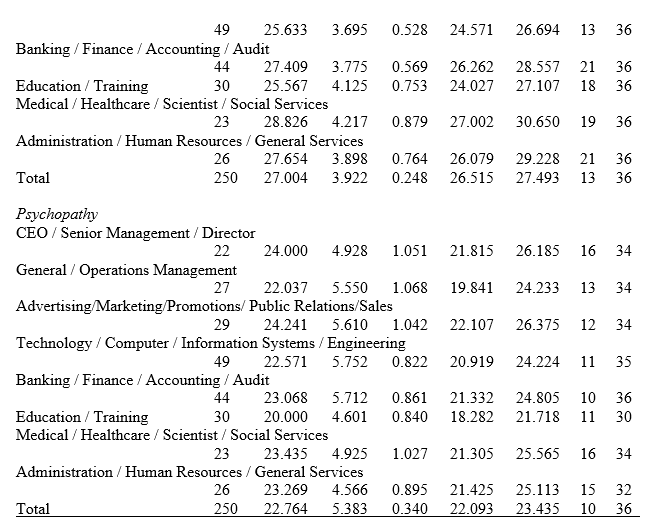

Additional analysis was conducted in order to determine which occupations display high levels of these traits, with a separate analysis also being conducted on the basis of the respondent’s age. A series of one-way ANOVAs were conducted in order to determine whether significant differences exist in the mean levels of these three psychological outcomes on the basis of respondent occupation. Table 13 summarizes descriptive statistics conducted in relation to these items on the basis of occupation. As shown, mean differences were generally found to be small, though more substantial than the mean differences indicated earlier on the basis of respondent age. Standard deviations were found to be moderate in comparison with these mean scores, with large ranges in scores generally being found.

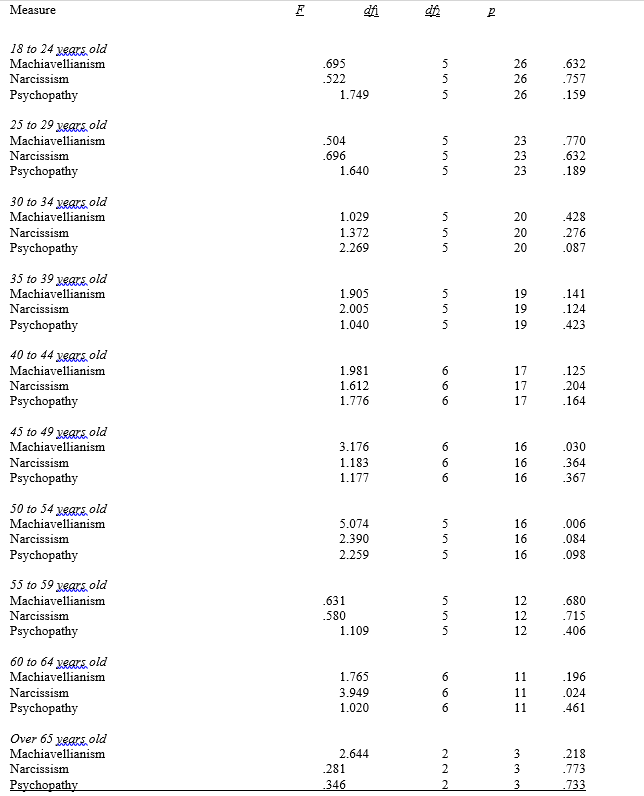

For the Levene’s tests conducted, statistical significance was not indicated with respect to the analysis conducted with Machiavellianism, W(7, 242) =.289, p =.958, Narcissism, W(7, 242) =.164, p =.992, or Psychopathy, W(7, 242) =.607, p =.750. The results indicate that the assumption of the homogeneity of variances was not violated in any of these three tests. With respect to the one-way ANOVAs, statistical significance was not found with regard to Psychopathy, F(7, 242) = 1.833, p =.082, while significance was indicated with respect to Machiavellianism, F(7, 242) = 3.887, p <.001, as well as Narcissism, F(7, 242) = 2.574, p =.014. These results indicate that significant mean differences exist with respect to both Machiavellianism and Narcissism on the basis of occupation. Post-hoc analyses found a substantial number of significant pairwise comparisons.

Table 154 summarizes the results of the Levene’s tests conducted on these data. With regard to these analyses and the ANOVAs, the one CEO / Senior Management / Director case was removed so that post-hoc analyses could be conducted. As shown, statistical significance was indicated in the analysis conducted with Psychopathy on the 30-34-year-old age group, the analysis conducted with Machiavellianism on the 40-44-year-old age group, as well as the analysis conducted with Narcissism and Psychopathy conducted on individuals above 65 years of age. In these specific cases, the Games-Howell post-hoc test was used instead of Tukey’s HSD as the Games-Howell test does not incorporate the assumption of the equality of variances.

Table 15 summarizes the results of the one-way ANOVAs conducted. Among these analyses, statistical significance was indicated in the following cases: Machiavellianism, 45-49 years old and 50-54 years old; and Narcissism, 60-64 years old. No significant post-hoc comparisons were found.

Research Question 2

The second research question included within this study consisted of the following:

Frauds are not committed at the spur of the moment; the fraudulent activity is usually not detected for about 18 months, those aged 35-55 will also display high levels of positive personality traits of Diligence, Integrity, and Self-Control compared to those aged <35.

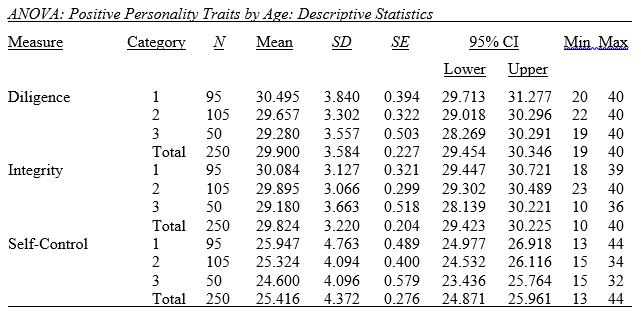

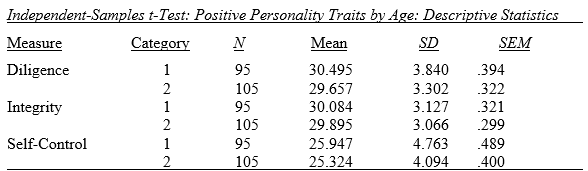

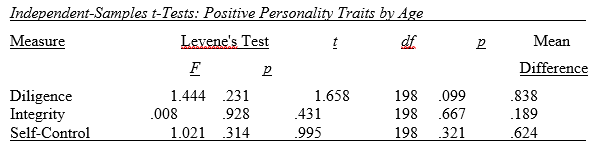

To explore this research question, a series of one-way ANOVAs were conducted focusing upon age-related differences in the mean levels of diligence, integrity, and self-control. Table 16 summarizes the descriptive statistics conducted in relation to these analyses. Only very slight mean differences were indicated in these measures on the basis of respondent age category. Standard deviations were found to be relatively low in relation to these mean scores, with the ranges presented generally found to be more restricted as compared with the descriptive statistics presented earlier. As in the previous one-way ANOVAs, in these analyses, individuals between the age of 35 and 55 were compared with those younger than 35 and those older than 55.

With regard to these analyses, Levene’s test for the quality of variances was not found to achieve statistical significance with respect to Diligence, W(2, 247) =.815, p =.444, Integrity, W(2, 247) =.009, p =.991, or Self-Control, W(2, 247) = 1.008, p =.367. These results indicate that the assumption of the equality of variances was not violated in any of these three analyses. For the one-way ANOVAs conducted, statistical significance was not indicated with respect to Diligence, F(2, 247) = 2.322, p =.100, Integrity, F(2, 247) = 1.339, p =.264, or Self-Control, F(2, 247) = 1.604, p =.203. The results of these analyses indicate that significant mean differences in these three outcomes do not exist on the basis of respondent age category.

A series of independent-samples t-tests were conducted focusing upon differences in these measures on the basis of age category, comparing those aged 35-55 with younger respondents. Table 17 summarizes the descriptive statistics conducted associated with these analyses. As shown, mean differences in these measures on the basis of age category were found to be very slight, with standard deviations found to be relatively small in relation to these mean values.

Table 18 summarizes the results of the independent-samples t-tests themselves. As shown, statistical significance was not found in any case, indicating that significant mean differences in these measures were not present on the basis of age category.

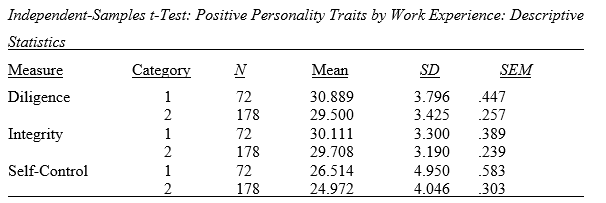

Additional independent-samples t-tests were conducted focusing upon differences in diligence, integrity, and self-control on the basis of work experience. Table 19 summarizes the descriptive statistics conducted associated with these analyses. However, mean differences were found to be minor, with standard deviations found to be relatively low in relation to these mean values.

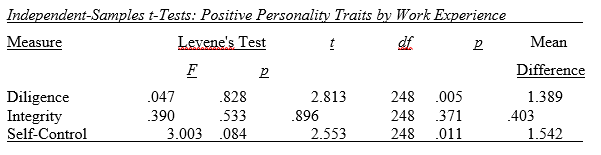

Table 20 summarizes the results of these independent-samples t-tests. As shown, statistical significance was not found in relation to integrity, while this was indicated with respect to diligence and self-control. Specifically, the results of these analysis indicated that individuals with less than 10 years of work experience had significantly higher scores on diligence as well as self-control.

Research Question 3

The third research question included in this study consisted of the following:

Those aged <35 however are more likely to have lower levels of Integrity but higher levels of Risk Taking compared to those aged 35-55, thus making them more susceptible to developing the deviant traits.

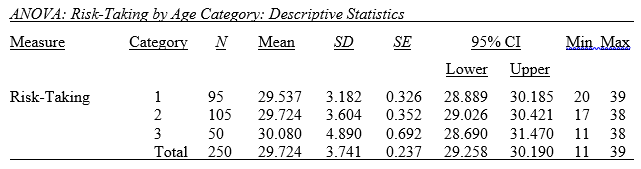

A one-way analysis of variance was conducted in order to determine whether significant mean differences in Risk-Taking exist on the basis of age category. Table 21 illustrates the descriptive statistics conducted in relation to this analysis. As shown, mean differences on the basis of age category were found to be very slight, with standard deviations found to be relatively low in relation to these mean values.

Levene’s test for the equality of variances was not found to achieve significance, indicating that the assumption of the homogeneity of variances was not violated in this analysis, W (2, 247) = 2.062, p =.129. Additionally, the one-way analysis of variance itself also failed to achieve statistical significance, F(2, 247) =.344, p =.710. This result indicates that there was no significant mean difference in Risk-Taking on the basis of age category based on this analysis.

Independent-samples t-test was conducted in order to further explore whether there was any association between age category and Risk-Taking. Table 22 summarizes the descriptive statistics associated with this analysis. Only a very slight difference in risk taking mean values was present on the basis of age category. Additionally, standard deviations were found to be low in relation to these mean values.

Table 23 summarizes the results of the independent-samples t-test conducted. Levene’s test failed to achieve statistical significance, indicating that the assumption of the equality of variances was not violated in this analysis. The independent-samples t-test conducted did not achieve statistical significance, indicating no significant mean difference in Risk-Taking on the basis of age category.

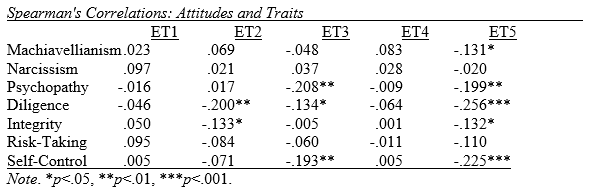

A series of Spearman’s correlations were conducted between all nine attitudes and all traits included within this study. The nine attitude questions are:

- Claim personal items as business expenses

- Keep a copy of confidential work documents in case you need them in your next job

- Claim for higher amounts of expenses than that spent

- A vendor offers to pay for a holiday if you inform them what their competitors are bidding in a tender

- Include additional hours in timesheets to make up for the cutbacks in bonus and incentives

- Give customers the impression that what they are buying is the genuine product

- Invoice your customer at one amount, submit a receipt for a lesser amount and keep the difference

- Deposit cash into your personal account instead of the company account to avoid being over-drawn until payday

- Buy a dress, wear it to a party, and then return it the next day for refund.

Spearman’s correlations were selected for these analysis as the measures of attitudes were ordinal, consisting of the responses of yes, neutral, and no, which would have violated the assumption of normality present within Pearson’s correlation coefficient.

Table 24 summarizes the results of the correlations conducted with the first five attitudes. Among these analyses, no significant correlations were indicated with the first or fourth attitude. However, with regard to the second attitude, having higher scores on Diligence and Integrity were associated with a significantly higher likelihood of indicating “yes” with regard to this attitude. Next, having higher scores on Psychopathy, Diligence, or Self-control were all associated with a significantly higher likelihood of responding with “yes” with regard to the third attitude. Following this, in the analyses conducted on the fifth attitude, it was found that having higher scores on Machiavellianism, Psychopathy, Diligence, Integrity, or Self-control were all associated with a significantly higher likelihood of responding with “yes”.

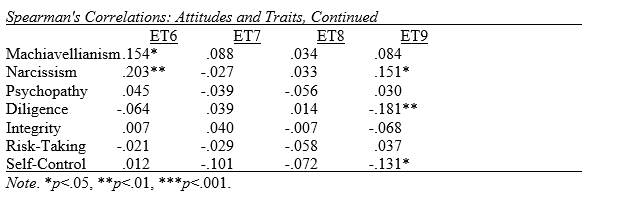

Table 25 summarizes the results of the correlations conducted on the sixth through ninth attitudes. No significant results were found with respect to attitudes seven or eight, while higher scores on Machiavellianism and Narcissism were both associated with a significantly higher likelihood of responding with “no” with regard to the sixth attitude. With regard to the ninth attitude, a higher score Narcissism was associated with a significantly higher likelihood of responding with “no”, while higher scores on Diligence and Self-control were both associated with a significantly higher likelihood of responding with “yes” for this attitude.

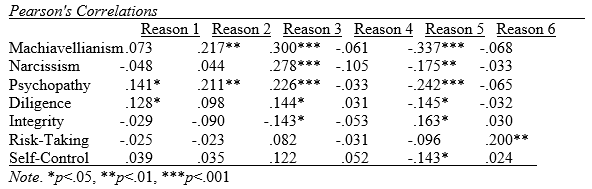

A series of Pearson’s correlations were conducted in order to determine the extent of the association between attitudes toward committing fraud and the reasons for not committing this crime. The results of these analyses are summarized in Table 26. The reasons presented to respondents consisted of the following:

- Concern over being arrested

- Concern over losing their job

- Their family and friends being embarrassed

- The crime being detected before it is committed

- None of the above

- It is acceptable.

Weak, positive, and statistically significant correlations were found between concern over being arrested and Psychopathy as well as Diligence, while additional weak, positive, significant correlations were indicated between concern over losing their job and Machiavellianism as well as Psychopathy. With regard to having their family and friends be embarrassed, weak, positive, and significant correlations were found with Machiavellianism, Narcissism, Psychopathy, and Diligence, with a weak, negative, significant correlation found with Integrity.

No significant correlations were found with concern over the crime being detected before it is committed, while significant, negative, and weak correlations were found between a response of none of the above and Narcissism, Psychopathy, Diligence, and Self-Control. Additionally, a significant, negative, and moderate correlation was found between this reason and Machiavellianism, with a weak, positive, and statistically significant correlation found with Integrity. Finally, a significant, positive, and weak correlation was indicated between feeling that this was acceptable and Risk-Taking.

Discussion

The findings of this study suggest that the main reason why employees engage in fraud is due to intrinsic motivating behavioural factors that influence their actions that manifest in the form of white-collar crime. Further analysis revealed that it was not primarily the existence of opportunities that resulted in such actions; rather, it was due to the inherent behavioural traits of that individual that took advantage of the opportunity as it presented itself. This means that the problem could be explained purely on psychological terms and was not necessarily a direct result of environment in question that caused an individual to become predisposed towards committing acts of white-collar crime.

This implies that the environment plays a minimal role in influencing people towards corporate criminal activity. However, it should be noted that corporate fraud does not happen in isolation because it entails a combination of motive and opportunity, which means the first step towards prevention of white-collar crime, is establishment of internal controls whereby sufficient checks and balances should be set up (Van-Aswegen and Engelbrecht 2009: 221).

This often manifests in the form of internal CSR (Corporate Social Responsibility) tactics as well as the establishment of a more ethical business culture within a company. However, despite what has been stated so far, there are also other factors that need to be taken into consideration when it comes to the propensity for individuals to commit acts of white-collar crime.

Social control theory states that all individuals actually have the potential to become criminals however it is the “bond” they share with society whether in the form of friendships, recognition of societal rules and norms of conduct, parental influences etc. that prevent them from actually committing a crime (Lowenstein 2003: 63). The theory goes on further to explain that it is actually quite normal for an individual to desire to commit a crime or even think about it such as desiring to steal and object, injure a person or other forms of criminal activity; however, they are prevented from doing so because of a distinct fear of the impact of this type of activity on their position (Eastman 2013: 529).

The concept of fear in this particular case comes in the form of the loss of societal bonds, careers, social relationships and other connections that individuals have come to rely on due to a person’s inherent nature to rely on social connections to retain a stable psychological state (Wilson 2006: 76). In other words, people are normally so dependent on social bonds and maintaining them that the thought of losing them after committing a particular action is sufficient enough to deter them from committing a crime. Social control theory helps to address the underlying issue behind the development of the adverse behavioural traits that were mentioned in the analysis section of the study (Enserink 2012: 21).

Simply put, an individual’s behaviour does not simply appear out of nowhere. Rather, it is the manifestation of learned behaviour over time, which influences their resulting actions. While a person may have the behavioural inclination to act in a criminal way and the opportunity presents itself, the fact remains that under social control theory they would still be unable or even hesitant to commit such crimes due to the potential loss of bonds that they would incur (Fleet & Griffin 2006: 700).

It is based on this perspective that social control theory states that white-collar crimes occur due to individuals either losing or weakening the various bonds which bind them to their society/organization and, as such, results in them not caring of the social ramifications of certain criminal actions. This helps to explain why individuals aged 35 to 55 were initially theorized to be more likely to commit white-collar crime as compared to their younger counterparts since, due to their respective ages; there is less of a dependence on the bonds formed within the organization and a greater level of focus being placed on personal interests.

Segal, Haberfeld & Gideon (2013) helps to explain this by stating that people that have been at their respective positions or jobs for a considerable level of time have already attained the necessary skill and expertise as well as have acclimatized to the organization that they work for to such an extent that they are no longer as dependent on support from other individuals as they used to be (Segal, Haberfeld & Gideon 2013: 94). Furthermore, individuals that are aged above 35 actually have a considerable level of other interests outside of work such as their family, hobbies and their respective lifestyles.

As such, it is more likely for them to have stronger bonds with those outside of work than with people within the company (McIntosh 2007: 1). Lastly, older employees within the company are more likely to be in influential positions within the company where white-collar crime is possible as compared to younger employees who have little, if any influence, within the company. It is from this perspective that the apparent “loss of bonds” explained by social control theory originates from and helps to show why there is a greater predilection for this age group to engage in white-collar crime as compared to their younger counterparts (Kolodinsky, Madden, Zisk & Henkel 2010: 173).

It is suggested by studies such as those by Tang & Sutarso (2013) that it is socialization and not the social structure itself that produces either positive or negative tendencies. Tang & Sutarso (2103) explain that “the more social problems encountered during the socialization process, the greater the likelihood that youths will encounter difficulties and obstacles as they mature, such as being unemployed or becoming a teenage mother” (Tang & Sutarso 2013: 530).

As social learning theorists suggest crime is a direct result of individuals learning norms, values, and behaviours associated with criminal activity. In fact the differential association theory created by Sutherland states that “crime does not originate from individual traits or a person’s socio-economic position rather it is a type of behaviour that is created through a learning process”. Thus, an individual would not have any apparent criminal tendencies while they were young but would develop such behavioural characteristics as a direct result of direct personal influences that result in the development of criminal behaviour. It was also noted by social learning theorists that people who develop criminal behaviour as a direct result of differential association justify their actions based on learned behaviour wherein ideas normally meant to prohibit crime do not manifest themselves resulting in a distinct lack of remorse for crimes committed.

It must also be noted that social control theory is not limited to criminal behaviour alone but also extends to other forms of what can be described as deviant behaviour. This can come in the form of bad behaviour, rebellious violent temperaments or what can otherwise be described as behavioural tendencies, which are looked upon as having negative connotations. For Murphy & Dacin (2011), these behavioural aspects are limited by punishments given for wrongful behaviour with compliance to proper behaviour often rewarded by parents or an authority figure. This helps to explain the reason why white-collar crime is prevalent among members of Wall Street since behaviours that are related to “risk taking” and a focus on profit are often rewarded by the corporations they work for (Murphy & Dacin 2011: 613).

What must be understood is that the characteristics that make a person more likely to commit white-collared crime are also the same characteristics that enable them to become successful in a variety of economic activities such as investment management. This is one of the reasons why this study is so important since it showcases what personality traits are likely to result in white-collar crime and what various financial institutions can do early on in order to address the issue.

Research Questions

Referring to research question 1, while age has always been a factor to consider in identifying the criminal behaviour of an individual, this study never established any significant relationship between age and the psychological disorders of Machiavellianism, psychopath, and narcissism.

Additionally, a comparison of the behaviour of individuals aged thirty-five and below and those aged above thirty-five do not suggest any interlink between age and fraud implying that this type of crime is special and is likely to be committed by individuals with defective personalities, irrespective of their age. In other words, other psychological, as well as social factors influence an individual’s behaviour towards engaging in fraud and white-collar crime. Even though a number of studies establish a statistical significance between an individual’s experience in the organization and the possibility of committing crime, this study failed to replicate such studies.

On the other hand, the occupation of an employee plays a greater role in influencing him or her to commit a white-collar crime because the findings of the study found out that the standard deviations were moderate meaning a relationship exists. Statistical significance was not found with regard to Psychopathy, F (7, 242) = 1.833, p =.082, while significance was indicated with respect to Machiavellianism, F (7, 242) = 3.887, p<.001, as well as Narcissism, F(7, 242) = 2.574, p =.014. These results indicate that significant mean differences exist with respect to both Machiavellianism and Narcissism based on occupation. based on age group (& occupation).

As shown, moderate mean differences were generally indicated. Statistical significance was indicated in the analysis conducted with Psychopathy on the 30-34-year-old age group, the analysis conducted with Machiavellianism on the 40-44-year-old age group, as well as the analysis conducted with Narcissism and Psychopathy conducted on individuals above 65 years of age. Finally, statistical significance was indicated in cases of Machiavellianism (45-49 and 50-54) and Narcissism (60-64).

The rank of the employee in the organization has a role to play as far as fraud is concerned because the higher the position the higher the chances of the employee committing a crime. In particular, those with access to company’s sensitive information are in a position to override controls hence are perpetrators of white-collar crimes. Again, the results of the study suggest that the department influences the behaviour as far as commission of crime is concerned. Those working in the finance department are vulnerable because they have access to the corporate assets apart from being in charge of financial reporting and credit lines.

The department is more tempting as compared to others, which do not have direct access to finances. The position of the chief executive officer (CEO) is the second most tempting followed by the sales and operations departments. Individuals working in the legal department are less vulnerable to white-collar crime because they understand the legal provisions and they are mostly guided by an ethical code of conduct. Individuals who join the company are not usually focused on committing the crime, but certain changes influence them to engage in immoral behaviours (Wakefield 2008: 114)

The findings from the investigation of the research questions also suggest that regional culture plays a role in influencing an individual’s intrinsic behaviour to such an extent that it impacts their predilection towards committing acts of white-collar crime. For instance, workers in Central and Eastern Europe rarely engage in fraud because of the strong corporate culture that condemns all forms of white-collar crime, including fraud. In fact, a number of global organizations originating from the region rarely find themselves in financial scandals as compared to those from Western Europe, Asia, and America.

In this regard, the multinational companies hire European citizens to take up key positions, such as those of chief executive and financial bosses with an aim of reducing fraud cases. Managers from Central and Eastern Europe are known to be whistle-blowers and initiators of investigations. Unfortunately, managers in the region collude with third-party clients to defraud companies, but the cases are usually reported in the sales and procurement departments meaning the company does not lose many resources. Just as Central and Eastern Europe, fraudsters collude with outsiders to channel resources to ghost projects, which amount to serious crime (Watt 2012: 113).

For research question 2, the study established that age-related differences in the mean levels of diligence, integrity, and self-control do exist but only in very slight mean differences that were indicated in these measures based on respondent age category. Standard deviations were found to be relatively low in relation to these mean scores, with the ranges presented generally found to be more restricted as compared to the descriptive statistics presented earlier. In the previous one-way ANOVAs, individuals between the age of 35 and 55 were compared with those younger than 35 and those older than 55.

Unfortunately, statistical significance was not indicated with respect to Diligence, F (2, 247) = 2.322, p =.100, Integrity, F (2, 247) = 1.339, p =.264, or Self-Control, F (2, 247) = 1.604, p =.203. The results of these analyses indicate that significant mean differences in these three outcomes do not exist because of respondent age category.

Differences in these measures based on age category, comparing those aged 35-55 with younger respondents established that mean differences in these measures on the basis of age category were found to be very slight, with standard deviations found to be relatively small in relation to these mean values. Statistical significance was not found in any case indicating that significant mean differences in these measures were not present based on age category. Again, mean differences were found to be minor, with standard deviations found to be relatively low in relation to these mean values. Statistical significance was not found in relation to integrity, while this was indicated with respect to diligence and self-control. Specifically, the results of these analyses indicated that individuals with less than 10 years of work experience had significantly higher scores on diligence as well as self-control

The study also established that narcissistic behaviours vary from one culture to another. Institutional theory is used in this study to assess financial misreporting among CEOs. Financial misreporting depends on the nature of the leadership and the CEOs ethical behaviour. Corporate psychopaths often work their way up to senior managerial positions within organisations (Chen 2010: 33). The Chen (2010) article shows empirical evidence in favour of psychopaths’ preference for senior corporate positions, as well as how their conscience-free attitude predisposes them to financial impropriety. Machiavellians are often deceitful and manipulative and thus rank among the top tax evaders.

The study is based on a survey of tax collectors in Hong Kong. The findings indicate that Machiavellianism influences the attitudes of tax collectors towards tax minimisation. Machiavellians also place less value on CSR because they believe that the central goal of any business is to maximise its profits. This helps to support the initial assumptions of the study that certain forms of behavioural predispositions are necessary in order for a person to commit a white-collar crime.

As for research question3, a one-way analysis of variance was conducted in order to determine whether significant mean differences in Risk-Taking exist based on age category. The findings of the study suggest that mean differences based on age category were found to be very slight, with standard deviations found to be relatively low in relation to these mean values. The one-way analysis of variance itself also failed to achieve statistical significance, F(2, 247) =.344, p =.710.

This result indicates that there was no significant mean difference in Risk-Taking on the basis of age category based on this analysis. Additionally, standard deviations were found to be low in relation to these mean values. The independent-samples t-test conducted did not achieve statistical significance, indicating no significant mean difference in Risk-Taking based on age category. This means that younger employees are statistically not as likely to engage in fraudulent activities as compared to their older counterparts nor are they more likely to engage in risk taking. Instead, based on the results, it can be seen that age is not necessarily a factor when it comes to the development of criminal behaviour in this population set. Instead, inherent psychological traits are more likely the reason why particular segments of this popular are likely to commit acts of fraud.

However, it should be noted that this study does not take into consideration the potential for learned behaviour over time impacting an employee’s predilection to commit a criminal act. Rather, it focuses on already present behaviour given the sheer amount of time (i.e. years) it would take to determine how learned behaviour over time would impact an employee’s predilection towards criminal behaviour.

The findings of the study reveal that mature employees with an experience of over ten years have a greater likelihood of engaging in white-collar crime, but their behaviour is not related to narcissism in any way because they believe that stealing from the company is a way of compensation rather than an ordinary theft (Elliott 2010: 270). This is in part due to the lack of societal bonds that were mentioned earlier which helped to promote the behaviour in the first place.

What the study does show is that young managers are ready to take risks because of their innovative nature and the desire to be successful by trying new things. However, the elderly managers prefer maintenance of status quo meaning they are reluctant to accept change. Therefore, deviant personality traits and lack of self-control leads an individual to commit white-collar crime, as well as fraud.

The dark triads, narcissism being one of them, are not prevalent in the higher age because the old managers engage in fraud as a form of compensation to their contribution in the organization (Ganon and Donegan 2006: 19). Employees with adequate experience have specific skills that allow them to manipulate the systems once they engage in fraud, but this does not mean they are narcissists. However, the elderly tend to apply Machiavellianism because they believe the ends will justify the means.

Conclusion

Based on an analysis of the data, it was revealed that there was little in the way of sufficient statistical significance that would help to indicate a sufficient predisposition towards white-collar crime based on age. The results concluded that weak, positive, and statistically significant correlations were found between concern over being arrested and Psychopath as well as Diligence while additional weak, positive, significant correlations indicated between concern over losing job and Machiavellianism and Psychopath.

With regard to having their family and friends being embarrassed, weak, positive, and significant correlations were found with Machiavellianism, Narcissism, Psychopath, and Diligence, with a weak, negative, significant correlation found with Integrity. No significant correlations were found with concern over the crime being detected before it is committed while significant, negative, and weak correlations were found between a response of none of the above and Narcissism, Psychopath, Diligence, and Self-Control. Additionally, a significant, negative, and moderate correlation was found between this reason and Machiavellianism, with a weak, positive, and statistically significant correlation found with Integrity.

Finally, a significant, positive, and weak correlation was indicated between feeling that this was acceptable and Risk-Taking. Overall, the study was able to show that factors related to Narcissism, Psychopath, Diligence, and Self-Control can be utilized as an effective means of evaluating the likelihood of employees engaging in white-collar crime, however, further testing is needed when it comes to devising the necessary questions that would effectively examine this point.

Recommendation

After completing the study, it was determined that the questions could have used a considerable level of “fine tuning” so to speak when it comes to their capacity to gather data. What must be understood is that one of the weaknesses when it comes to a survey based method is that there is a propensity for the research subjects to falsify the data in favour of making themselves look good. Given the format of the research questions, the origin of the lack of sufficient statistical significance in the research paper becomes immediately obvious.

Future research into the topic may want to consult more academic articles on proper research question format or utilize an interview based approach and quantify the results. It is expected that should this suggestion be followed, a study with a greater level of statistical significance can be developed which would result in a more accurate result.

Reference List

Basson, D 2000, ‘The psychology of fraud’, Finance Week, p. 40.

Birtch, T, & Chiang, F 2014, ‘The Influence of Business School’s Ethical Climate on Students’ Unethical Behavior’, Journal Of Business Ethics, 123(2) 283-294.

Chen, S. (2010) ‘The Role of Ethical Leadership Versus Institutional Constraints: A Simulation Study of Financial Misreporting by CEOs’. Journal of Business Ethics 93(1), 33-52.

Ding, C., Chang, K. and Liu, N. (2009) ‘The roles of personality and general ethical judgments in intention to not repay credit card expenses’. Services Industries Journal 29(6), 813-834.

Duffield, G, & Grabosky, P 2001, ‘The Psychology of Fraud. (cover story)’, Trends & Issues In Crime & Criminal Justice 199(1), 1-6.

Eastman, W 2013, ‘Ideology as Rationalization and as Self-Righteousness: Psychology and Law as Paths to Critical Business Ethics’, Business Ethics Quarterly 23(4), 527-560.

Elliott, R. (2010) ‘Examining the Relationship between Personality Characteristics and Unethical Behaviours Resulting in Economic Crime’. Ethical Human Psychology & Psychiatry 12(3), 269-276.

Enserink, M 2012, ‘Fraud-Detection Tool Could Shake Up Psychology’, Science 337(6090) 21-22.

Fleet, D, & Griffin, R 2006, ‘Dysfunctional organization culture: The role of leadership in motivating dysfunctional work behaviors’, Journal Of Managerial Psychology 21(8), 698-708.

Ganon, M. and Donegan, J. (2006) ‘Self-Control and Insurance Fraud’. Journal of Economic Crime Management 4(1), 1-20.

Gibbs, C, Cassidy, M, & Rivers, L 2013, ‘A Routine Activities Analysis of White-Collar Crime in Carbon Markets’, Law & Policy 35(4), 341-374.

Hartog, D. and Belschak, F. (2012) ‘Work Engagement and Machiavellianism in the Ethical Leadership Process’. Journal of Business Ethics 107(1), 35-47.

Henle, C. (2005) ‘Predicting Workplace Deviance from the Interaction between Organizational Justice and Personality’. Journal of Managerial Issues 17(2), 247-63.

Johnson, E., Kuhn, R., Apostolou, B., and Hassell, J. (2013) ‘Auditor Perceptions of Client Narcissism as a Fraud Attitude Risk Factor’. Auditing: A journal of Practice & Theory 32(1), 203-219.

Kolodinsky, R, Madden, T, Zisk, D, & Henkel, E 2010, ‘Attitudes About Corporate Social Responsibility: Business Student Predictors’, Journal Of Business Ethics 91(2), 167-181.

Laffey, TA 2004, ‘Insurance fraud: cause and effect’, Journal Of Commerce (15307557) 5(4), 11.

Lowenstein, LF 2003, ‘The Genetic Aspects of Criminality’, Journal Of Human Behavior In The Social Environment 8(1), 63-78.

Marshall, A, Baden, D & Guidi, M 2013, ‘Can an Ethical Revival of Prudence Within Prudential Regulation Tackle Corporate Psychopath?. Journal of Business Ethics 117(3), 559-568.

Martin, D., Rao, A., and Sloan, L. (2009) ‘Plagiarism, Integrity, and Workplace Deviance: A Criterion Study’. Ethics & Behaviour 19(1), 36-50.

Messick, D 2009, ‘What can Psychology Tell us About Business Ethics?’, Journal Of Business Ethics 89, 73-80.

McIntosh, K 2007, ‘Revisiting the Past: The Value of Psychology and Group Dynamics in Explaining Criminal Behavior’, Conference Papers — American Society Of Criminology 8 (4), 1.

Murphy, P, & Dacin, M 2011, ‘Psychological Pathways to Fraud: Understanding and Preventing Fraud in Organizations’, Journal Of Business Ethics 101(4), 601-618.

Norton, C 2010, ‘The Psychology of Fraud: Ways to protect your bank from white collar criminals’, New Jersey Banker 4(3), 18-33.

Perri, F. (2011) ‘White‐Collar Criminals: The ‘Kinder, Gentler’ Offender?’. Journal of Investigative Psychology and Offender Profiling 8(1), 217-241.

Quinsey, VL 2002, ‘Evolutionary theory and criminal behaviour’, Legal & Criminological Psychology 7(1), 1.

Ramamoorti, S 2008, ‘The Psychology and Sociology of Fraud: Integrating the Behavioral Sciences Component Into Fraud and Forensic Accounting Curricula’, Issues In Accounting Education 23(4), 521-533.

Segal, L, Haberfeld, M, & Gideon, L 2013, ‘The Effects of the Recession on Attitudes toward Business Ethics: An Inter-temporal Study of Business Students in 2001, 2009, and 2010’, Business & Society Review (00453609) 118(1), 71-104.

Shafer, W. and Simmons, R. (2008) ‘Social responsibility, Machiavellianism and tax avoidance: A study of Hong Kong tax professionals’. Accounting, Auditing & Accountability Journal 21(5), 695-720.

Stevens, G., Deuling, J., and Armenaki, A. (2012) ‘Successful Psychopaths: Are They Unethical Decision-Makers and Why?’. Journal of Business Ethics 105(1), 139-149.

Tang, T, & Sutarso, T 2013, ‘Falling or Not Falling into Temptation? Multiple Faces of Temptation, Monetary Intelligence, and Unethical Intentions Across Gender’, Journal Of Business Ethics 116(3), 529-552.

Van-Aswegen, A. and Engelbrecht, A. (2009) ‘The Relationship between transformational leadership, integrity, and an ethical climate in organisations’. South African Journal of Human Resource management 7(1), 221-229.

Wakefield, R.L. (2008) ‘Accounting and Machiavellianism’. Behavioural Research in Accounting 20(1), 115–129.

Wasieleski, D, & Hayibor, S 2009, ‘Evolutionary Psychology and Business Ethics Research’, Business Ethics Quarterly 19(4), 587-616.

Watt, R. (2012) ‘University students’ propensity towards white-collar versus street crime’. Journal of Business Ethics 5(2), 113-125.

Wilson, S 2006, ‘‘Collaring’ the Crime the Criminal?: ‘Jury Psychology’ and Some Criminological Perspectives on Fraud and the Criminal Law’, Journal Of Criminal Law 70(1), 75-74.

Appendix 1: Participant Questionnaire

Demographics

- Are you?

- Male

- Female

- Which age group do you fall into?

- Under 18

- 18-24

- 25-29

- 30-34

- 35-39

- 40-44

- 45-49

- 50-54

- 55-59

- 60-64

- 65 or older

- Number of years you have worked:

- Less than 2 years

- 2-4 years

- 5 – 9 years

- 10 – 14 years

- 15 – 19 years

- 20 – 24 years

- More than 25 years

- Number of companies/organisations you have worked for:

- 1 – 2

- 3 – 5

- 6 – 10

- More than 10

- Which of the following categories best describes your occupation or most recent occupation?

- CEO / Senior Management / Director

- General / Operations Management

- Advertising/Marketing/Promotions/ Public Relations/Sales

- Technology / Computer / Information Systems / Engineering

- Banking / Finance / Accounting /Audit

- Education / Training

- Medical / Healthcare / Scientist / Social Services

- Administration / Human Resources / General Services

- Other

- Which region do you currently live in?

- Asia / Japan

- Middle East / Africa

- United Kingdom / Ireland

- Europe

- Canada / United States

- Australia / Oceania

- Other

Participant Questionnaire Instructions

Each item of this questionnaire is a statement that a person may either agree with or disagree with. For each statement, indicate how much you agree or disagree with what the item says. Please respond to all the items; do not leave any blank. Choose only one response to each statement. Please be as accurate and honest as you can be. Respond to each item as if it were the only item. That is, don’t worry about being “consistent” in your responses.

There are no right or wrong answers to any of these statements; we are interested in your honest reactions and opinions. Please read each statement carefully, and respond by using the following scale from 1 to 5:

1 = I strongly disagree with the statement

2 = I disagree with the statement

3 = I neither agree nor disagree with the statement

4 = I agree with the statement

5 = I strongly agree with the statement

Your answers will be analysed totally anonymously; no answers will be connected with any personal information of the respondents. The survey will take up to 20 minutes.

Please rate your agreement or disagreement with each item below:

Last question (Reason)

You will not commit a fraud because: [Tick all that apply]

- May be caught and will be arrested

- Could lose my job

- My family and friends will be embarrassed

- Will be detected before it is committed

- None of the above

- Not Applicable – it is acceptable

- Other [_______________________]

Thank you for your participation.